Your car is in a tow yard or at a body shop. The other driver may have admitted fault, or maybe the story is already getting messy. You've taken a few photos, opened a claim, and now someone from the insurance company says an auto damage adjuster will inspect the vehicle.

That's usually the point where frustration starts. You don't just want a number on paper. You want the car repaired correctly, the hidden damage found, the right parts approved, and the claim handled without getting pushed into shortcuts.

In Oregon and Washington, that stress often overlaps with larger property losses. A windstorm damages your roof and drops a limb onto the family vehicle. A garage fire affects both the structure and the car inside. A vandalism claim turns into questions about dwelling damage, contents, and vehicle damage all at once. National guides rarely address that overlap, but it matters. The people handling the building claim and the people handling the auto claim may use different standards, different estimating tools, and different assumptions.

The adjuster's role sits at the center of that process. If you understand what that person does, how the estimate is built, and where low numbers usually come from, you'll make better decisions from the start.

The Aftermath of an Accident and the Adjuster's Role

The first few days after a crash are rarely orderly. You're arranging a rental, answering calls, trying to remember what happened, and hearing terms like supplement, total loss, teardown, salvage, and liability before you've even seen the full damage.

That's where the adjuster enters the picture. In a practical sense, the auto damage adjuster is the person who translates visible vehicle damage into dollars the insurer is willing to pay. For many policyholders, that makes the adjuster the gatekeeper between a damaged car and a usable settlement.

A lot of policyholders assume the inspection is just a quick look around the bumper and fender. It isn't. Even on a straightforward collision, the estimate becomes the working document that drives repair approval, parts choices, labor operations, and the next round of negotiations if the shop finds more damage after disassembly.

A claim often turns on the first scope written down, even when everyone knows the first scope usually isn't the full story.

That matters even more when the auto claim is tied to a broader property event. In the Pacific Northwest, storms, falling trees, floods, and fires can damage more than one type of insured property at the same time. The homeowner may focus on the roof or structure first because that loss feels bigger, while the vehicle claim gets treated like a side issue. Insurers often separate those files. You shouldn't separate your documentation.

When a vehicle is damaged during the same event as a house, garage, or business property, keep the timeline, photos, receipts, and witness information consistent across both claims. If the storm caused all of it, your records should show one clear chain of events. That avoids a common problem where one department accepts the cause of loss and another starts questioning it.

What an Auto Damage Adjuster Really Does

Think of an auto damage adjuster as a financial auditor for vehicle damage. The adjuster doesn't repair the car. The adjuster evaluates what the insurer believes should be paid, based on inspection findings, parts and labor databases, and the policy terms that apply.

According to O*NET's summary for insurance appraisers of auto damage, auto damage adjusters play a critical role in evaluating vehicle damage to determine repair costs, and the median annual wage is $76,650. That same source notes that key duties include using standard automotive labor and parts cost manuals to estimate repairs and deciding whether a vehicle should be treated as a total loss.

If you've ever wondered whether this is a specialized job or an entry-level paper-pushing role, that wage data answers part of it. The work demands judgment. Structural damage, mechanical damage, electrical damage, interior damage, and repair practicality all affect the estimate.

For readers curious about the profession itself, including how people enter the field, this overview of auto damage adjuster jobs gives useful background.

What happens during the inspection

A solid inspection usually includes more than a few exterior photos. The adjuster should identify damaged panels and components, note point of impact, review obvious related damage, and decide whether the estimate can be written immediately or needs teardown by a repair shop.

In day-to-day claims work, the process usually looks like this:

- Vehicle identification: VIN, mileage, trim level, options, and condition all matter.

- Damage mapping: The adjuster marks the impact area and related parts that appear affected.

- Repair versus replace decisions: Many disputes begin at this stage of the process.

- Pricing the estimate: Labor operations and parts are pulled from estimating systems and manuals.

- Total loss review: If repair cost and vehicle value are too close, the file may shift away from repair.

What the adjuster is trying to answer

The adjuster's estimate is built around a few practical questions:

| Question | Why it matters |

|---|---|

| What was damaged? | The insurer only pays for covered damage tied to the loss. |

| Can the part be repaired? | Repair is often cheaper than replacement. |

| If replacement is needed, what part type applies? | OEM, aftermarket, recycled, or reconditioned parts can change the number. |

| Is more disassembly required? | Hidden damage often appears after teardown. |

| Is the car repairable at all? | If not, the claim moves toward total loss handling. |

Practical rule: An estimate is not a repair blueprint. It's the insurer's starting position.

That distinction matters. A body shop writes to restore the vehicle. An insurer's adjuster writes to evaluate what it believes is owed at that stage of the claim. Sometimes those line up. Sometimes they don't.

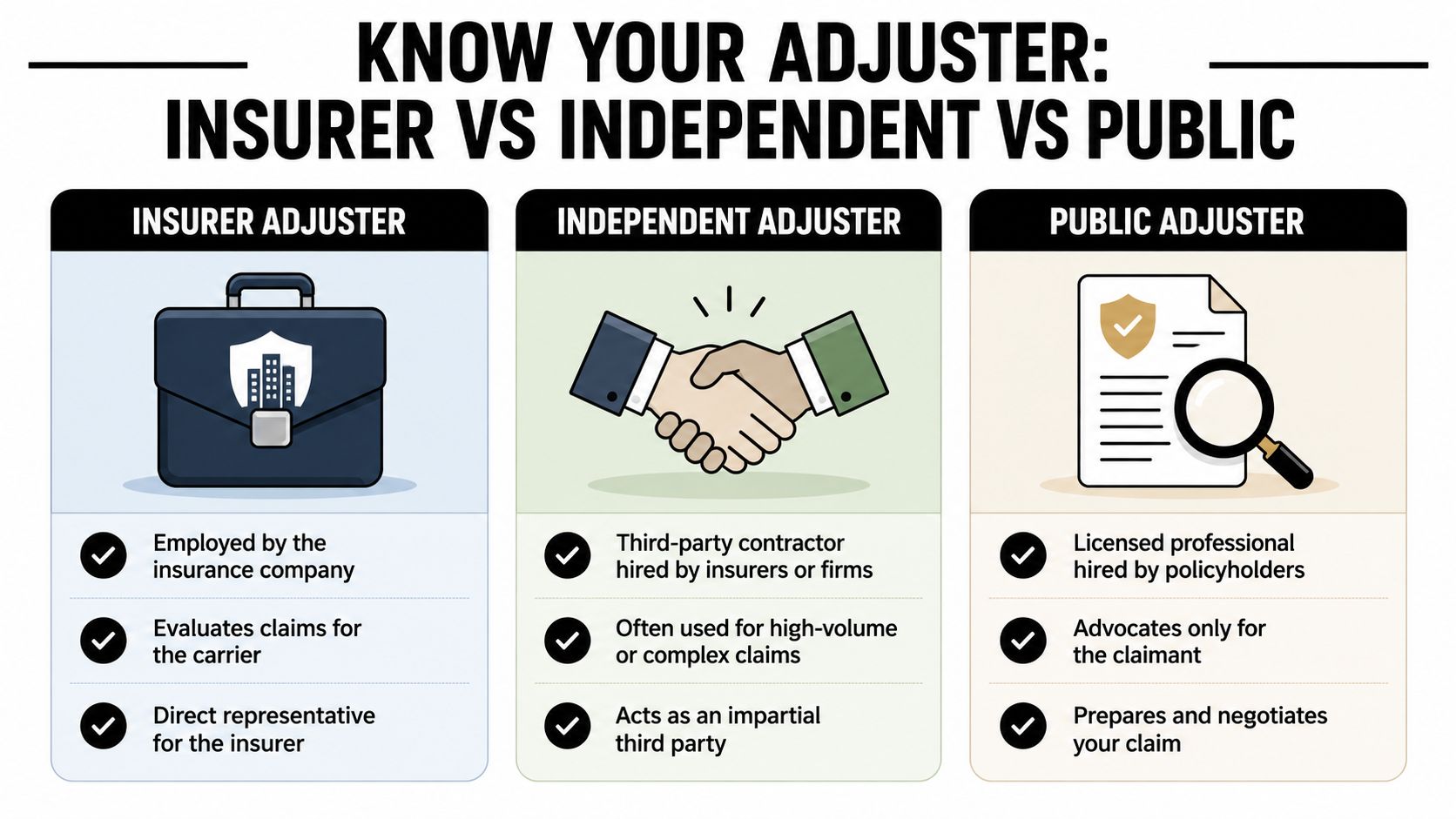

Know Who You're Talking To Insurer vs Independent vs Public Adjusters

A lot of confusion comes from one word: adjuster. People hear it and assume every adjuster plays the same role. They don't. The title sounds similar, but allegiance changes everything.

The three roles in plain language

An insurer adjuster works directly for the insurance company. That person may be a staff employee handling claims under the carrier's internal procedures and settlement authority.

An independent adjuster is not the policyholder's independent representative. This is the point many people miss. Independent adjusters are outside contractors hired by insurers to inspect and estimate claims on the insurer's behalf.

A public adjuster works for the policyholder, not the carrier. That changes the objective, the scope review, and the negotiation posture from the outset.

For a deeper side-by-side breakdown, this guide on public adjuster vs insurance adjuster is useful.

Three Types of Adjusters Who Do They Work For?

| Adjuster Type | Works For | Primary Goal |

|---|---|---|

| Insurer Adjuster | The insurance company | Evaluate and settle the claim for the carrier |

| Independent Adjuster | The insurance company that hires them | Inspect and estimate on the carrier's behalf |

| Public Adjuster | The policyholder | Prepare, document, and negotiate the claim for the insured |

Why this distinction changes your claim

If a carrier sends a field appraiser to inspect your car, that doesn't mean the inspection will be unfair. Many adjusters do careful work. But it does mean the adjuster is operating within the insurer's system, estimate platform, review standards, and payment authority.

That affects real decisions such as:

- Parts selection: The carrier may favor lower-cost allowable parts where policy language or state rules permit.

- Labor operations: Some necessary procedures may be omitted initially and added later only if the shop pushes for a supplement.

- Damage causation: The insurer's representative may question whether a condition was pre-existing or caused by the reported loss.

- Total loss treatment: The file may be steered toward repair or total loss depending on valuation and salvage considerations.

Public adjusters matter most when the dispute isn't just over a line item but over the scope, cause, valuation, or strategy of the entire claim. That's especially true when the vehicle loss is tied to a larger home, commercial, or nonprofit property loss. In those situations, one representative who can keep the narrative and documentation organized across the broader damage picture can make a major difference.

If you don't know who the adjuster works for, you can't accurately judge what the estimate is meant to accomplish.

How to Document Damage and Prepare for the Inspection

Before the adjuster sees the vehicle, your job is to preserve evidence. Not to argue. Not to guess at repair cost. Preserve evidence.

The reason is simple. The Bureau of Labor Statistics projects a 5% decline in employment for claims adjusters, appraisers, examiners, and investigators from 2024 to 2034, and 50% of auto appraisers report moderate automation, using software with preset formulas for parts and labor, according to the BLS occupational outlook for claims professionals. In practice, that means your claim may be touched by estimating systems that are efficient but not always complete.

Detailed documentation helps when software-driven estimates come in light.

Your photo set should be deliberate

Don't just take one shot of the dent and move on. Build a record that shows the full condition of the vehicle.

Use this shot list:

- Wide-angle photos: Capture all four corners of the vehicle and the overall resting position.

- Mid-range photos: Show each damaged area in relation to adjacent panels.

- Close-ups: Focus on cracks, gaps, scrapes, broken lamps, bent suspension areas, deployed airbags, and wheel damage.

- Identification photos: Take the VIN label, license plate, and odometer.

- Interior photos: Capture warning lights, airbag deployment, broken trim, seatbelt locking, or glass debris.

- Undercarriage or wheel area shots: If safely accessible, document anything bent, leaking, or out of alignment.

If the damage may involve hidden prior repairs or older collision history, it helps to understand the signs. This guide on inspecting used cars for past collisions is useful because many of the same clues matter when separating new damage from pre-existing issues.

What not to do before inspection

Some mistakes hurt good claims.

- Don't clean the damaged area: Dirt patterns, transfer marks, fluid residue, and shattered material can all matter.

- Don't authorize major repair work too early: Emergency measures are fine, but full repairs before documentation can create avoidable disputes.

- Don't minimize the damage on calls: Casual comments like “it's probably just cosmetic” can come back later.

- Don't throw away broken parts or debris: Keep what you can safely store.

Build your own baseline estimate

A reputable body shop can help identify likely hidden damage, necessary scans, and repair procedures. That doesn't mean the first shop estimate will control the claim, but it gives you a baseline against the insurer's version of events.

Independent documentation becomes powerful in this situation:

- You show the condition of the car before teardown.

- The shop identifies what the initial insurer estimate may have missed.

- Supplements become easier to justify because the record is organized.

For owners dealing with a more involved valuation dispute, professional auto insurance appraisals can help frame the disagreement around evidence instead of frustration.

Bring the adjuster to your documentation, not the other way around. A claim file with organized photos, receipts, and notes is harder to discount.

Disputing a Low Settlement Offer

Low offers usually don't arrive with a dramatic announcement. They show up as an estimate that looks official, detailed, and final. It may list dozens of line items, but still miss what matters.

That's why disputes should start with scope, not emotion. If the number is low, ask what damage was excluded, what operations were omitted, what parts were priced, and whether the insurer assumed repair where replacement is safer or more appropriate.

According to AdjusterPro's auto claims training material, improper damage scoping can lead to 15% to 25% variance in claim payouts. The same source notes that mis-scoping a bent control arm as repairable rather than requiring replacement can increase post-repair failure risk by 40%, and that public adjusters use this technical support to argue for replacement under OEM guidelines, often increasing recovery by 20% to 30%.

Where low estimates usually break down

Not every bad estimate is bad for the same reason. Some are incomplete because the car hasn't been disassembled yet. Others are low because the estimate makes aggressive assumptions.

Common pressure points include:

- Repair versus replace decisions: Structural and suspension parts should not be treated casually.

- Missing operations: Calibrations, scans, corrosion protection, seam sealer, or teardown steps may be absent.

- Parts disputes: The estimate may assume a lower-cost part that your shop challenges.

- Causation disputes: The insurer may label damage as unrelated or pre-existing.

Practical ways to challenge the number

Start with documents, not accusations.

Ask for:

- the full estimate with line-item detail

- the photos used by the adjuster

- the basis for any denied or omitted operations

- clarification on part type assumptions

- a written explanation if the insurer says damage was pre-existing

Then bring in competing support from the repair side. OEM procedures, body shop documentation, teardown findings, and third-party appraisals all help move the discussion away from opinion.

Many policies also include an appraisal mechanism for valuation disputes. The exact wording matters, and so does the nature of the disagreement. Appraisal usually works better when both sides agree there is covered damage but disagree on value. It's less useful if the insurer is disputing coverage or cause.

If you're already in that negotiation stage, guidance on negotiating with an insurance company can help you frame the dispute more effectively.

A low offer isn't the end of the claim. It's often the first serious draft.

You may also hear about diminished value, especially when the vehicle will carry an accident history even after proper repairs. Whether that claim is available and worth pursuing depends on the facts, the type of claim, and the governing law. It's a separate issue from repair cost, so don't let anyone fold it into the main estimate without making the distinction clear.

Navigating Claims in Oregon and Washington

Oregon and Washington policyholders often run into a problem national articles ignore. The claim may be local, but the insurer's process is national. That can create friction when local repair practices, state consumer rules, and real shop conditions don't line up neatly with a standardized estimate.

Why local handling matters

In both states, vehicle claims often intersect with weather-related property losses. A storm doesn't care whether the damage lands on a roof, a fence, a detached garage, or the vehicle parked beside it. But carriers often separate those losses into different workflows.

That creates practical risks:

- Inconsistent cause-of-loss descriptions: One claim file may accept storm impact while another questions it.

- Documentation drift: Photos and notes submitted to one department never make it into the other file.

- Repair timing conflicts: The owner may move the car, clean the site, or authorize emergency work on the property before the vehicle evidence is fully preserved.

What Oregon and Washington owners should do differently

Keep one master loss file for the whole event. Include photos, dates, receipts, weather records, witness names, towing documents, and shop communications in one organized timeline, even if the insurer splits the claims internally.

If the vehicle was inside a structure when the event happened, document the relationship between the two. Show where the car sat, what fell on it, what debris contacted it, and whether fire, smoke, water, or collapse affected both the building and the vehicle.

For policyholders who need local help sorting out the right kind of claims professional, a search for a qualified claims adjuster near me should focus on licensing, claim type experience, and familiarity with Oregon and Washington practice, not just proximity.

The overlooked point is this: local claims rarely fail because the damage wasn't real. They fail because the file became fragmented. In Oregon and Washington, the strongest claims are the ones where the vehicle story and the property story match from day one.

Taking Control of Your Auto Damage Claim

The auto damage adjuster has an important job, but that job isn't to think like your repair shop or advocate like your representative. The adjuster evaluates damage through the insurer's claim process. That's why your preparation matters so much.

A strong claim usually comes down to a few basics. Document the vehicle thoroughly. Keep the timeline clean. Get repair input early. Challenge scope problems with evidence, not guesswork. If the auto loss is part of a larger storm, fire, or vandalism event, treat the vehicle claim and property claim as connected parts of the same story.

That approach won't eliminate every dispute, but it gives you an advantage when the first estimate misses damage, prices the wrong parts, or pushes the claim toward an outcome that doesn't restore what you lost.

When people feel overwhelmed, it's usually because the file has gotten bigger than expected. More moving parts. More departments. More pushback. At that point, control comes from organization, technical support, and knowing when to bring in expert help rather than continuing to argue the same points by phone.

Frequently Asked Questions About Auto Damage Adjusters

Can the insurance company force me to use its preferred body shop

In most situations, you can choose your repair shop. Insurers may recommend direct repair program shops, and those shops can be convenient, but convenience isn't the same as obligation. If you prefer a shop you trust, say so clearly and early.

Is the first estimate usually the final amount

Often, no. Initial estimates are commonly written before full teardown. Hidden damage may appear once the shop disassembles the vehicle, and that can lead to supplements. The key is making sure those supplements are documented properly.

What if the adjuster says some damage was already there

Ask for the basis of that conclusion in writing. Then compare it against your photos, maintenance records, prior repair invoices, and the shop's findings. Pre-existing damage disputes are easier to challenge when your file is organized from the start.

What makes a vehicle a total loss

That decision usually depends on the relationship between repair cost, vehicle value, and salvage considerations. The specific method can vary by insurer and claim facts. If the carrier shifts the claim toward total loss, ask for the valuation support and review it carefully.

Should I talk to the adjuster before I get a shop estimate

Yes, but keep your comments factual. Give the basic loss information, explain what happened, and avoid guessing about repairability. A shop estimate helps, but your first priority is preserving evidence and opening the claim cleanly.

Does a public adjuster handle only house claims, or can they help when vehicle damage overlaps with property damage

Many people associate public adjusters only with buildings, but overlap claims are where experienced representation can be especially valuable. If a storm, fire, or collapse damages both the structure and property connected to the event, coordinated documentation can prevent one part of the loss from undermining another.

If your claim is getting complicated, or the vehicle damage is part of a broader fire, storm, flood, or vandalism loss, NW Claims Management can help you evaluate the file, understand your options, and push for a fair outcome. As a licensed public adjusting firm serving Oregon and Washington, the team advocates for policyholders, not insurers, and offers a free claim evaluation to help you decide your next step.