You open the mail, look at the insurance estimate, and feel a little relief. Then your contractor's bid arrives, and that relief disappears.

The numbers don't line up. The insurer says one thing. The actual rebuild cost says another. If you're recovering from fire, water, storm, or another major property loss, that gap can feel personal. It can make you wonder whether you're overreacting, whether the contractor is inflating the price, or whether you're missing something in your policy.

In many cases, you're not missing anything. You're running into construction cost inflation.

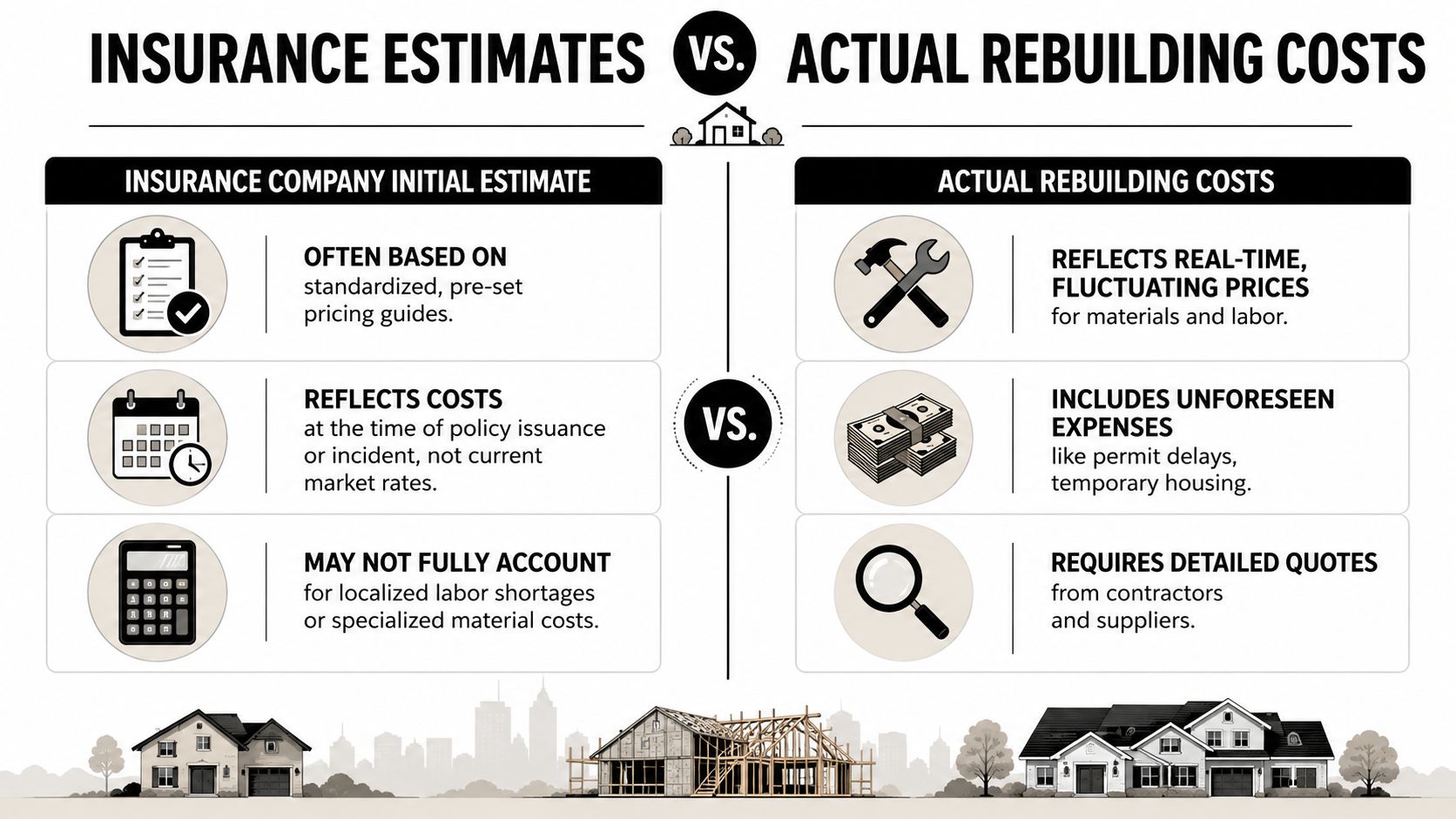

That phrase sounds technical, but the problem is simple. The cost to put your home or building back together may have moved faster than the pricing assumptions behind your insurer's initial valuation. When that happens, the first payout can fall short of what local contractors are charging to rebuild today.

Your Insurance Payout Versus Reality

A homeowner after a kitchen fire often sees the same pattern. The insurance company issues an initial estimate. It may look detailed. It may even include line items for drywall, cabinets, flooring, paint, and labor. Then the homeowner brings in a local contractor who has crews booked out, suppliers quoting current prices, and subcontractors charging today's rates. The contractor's bid comes in much higher.

That doesn't automatically mean someone is acting in bad faith. It usually means the estimate and the rebuild are being priced from two different realities.

One reality is the insurer's starting point. The other is the market you have to hire from.

This is also where many people get confused about actual cash value and replacement cost. If your claim involves depreciation, holdbacks, or staged payments, the timing of what gets paid can make the shortfall feel even worse. If you need a plain-English refresher, this guide on actual cash value vs. replacement cost helps clarify why your first check may not reflect the full amount required to complete repairs.

The key point is reassuring. If your contractor says the work costs more than the insurer's first number, that doesn't make you unreasonable. It often means the market moved, the estimate needs updating, or the scope needs to be documented in more detail.

What Construction Cost Inflation Really Means

Construction cost inflation means the price to repair or rebuild a property rises over time, often faster than homeowners expect. After a loss, that increase shows up in a very practical place. The insurer may have one number on paper, while contractors in your area are quoting a different number for the same job.

A construction bid works a lot like a full project bill, not a shopping receipt. The wood, shingles, and drywall matter, but they are only part of the cost. You are also paying for skilled labor, job supervision, equipment, scheduling, permit coordination, subcontractor availability, insurance, and the contractor's operating margin. If any one of those pieces gets more expensive, the rebuild total moves with it.

That is why a homeowner can look at a line item and say, “The materials alone do not cost that much,” and the contractor can still be right about the final bid. The gap usually comes from everything wrapped around the materials. In a claim, that distinction matters because insurers often start with estimating assumptions, while your contractor is pricing an actual job under current local conditions.

Why construction inflation differs from everyday inflation

The inflation discussed on the news usually refers to broad consumer prices, such as food, gas, or rent. Rebuilding a house follows a different cost pattern. Construction pricing depends on trade labor, supplier lead times, code requirements, equipment costs, and what contractors must charge to keep a project moving without delays.

Industry research from Turner & Townsend explains that construction costs should be tracked with building-specific indices rather than general CPI because broad inflation measures do not reliably reflect what projects cost to complete in the field, as explained in Turner & Townsend's global construction cost trends analysis.

Here is the plain-English takeaway. If an insurer's estimate is based on generalized pricing, but your contractor is pricing a live rebuild with current labor and supplier quotes, the difference deserves documentation. It should not be brushed aside as a misunderstanding.

Many estimates are built with pricing software and databases. Those tools help create consistency, but the result still depends on the selected line items, the local pricing updates, and whether the scope matches the actual work needed at your property. If you want to understand how those estimating systems influence claim values, this guide to Verisk Xactimate training gives useful background.

The same inflation pressure also affects property owners outside the insurance setting. For a broader market view, these strategies for real estate during inflation show how rising costs can change investment and rebuilding decisions.

Why Rebuilding Costs Keep Rising

The short answer is that rebuilding costs rise when several pressures hit at the same time. Materials shift. Labor tightens. suppliers adjust pricing. Contractors protect themselves against uncertainty. A homeowner usually sees only the final number, but that number reflects a chain of decisions and constraints behind the scenes.

The recent jump was not minor. Construction cost inflation in the United States experienced a historic surge in 2022, with residential building inflation reaching 15.8% and nonresidential building inflation hitting 12.8%, marking the most severe annual increases in over a decade. These rates were more than triple the typical long-term construction inflation rate, according to Ed Zarenski's construction inflation analysis.

The drivers don't arrive one at a time

A rebuild estimate can climb even when one category seems stable, because several categories are moving together.

| Cost pressure | What it looks like in a claim |

|---|---|

| Supply chain disruption | Longer waits, substitute products, rush ordering, and revised bids |

| Skilled labor shortages | Higher labor pricing and fewer contractors willing to commit quickly |

| High construction demand | Contractors prioritize larger or easier jobs, which can raise pricing on smaller restoration work |

| Energy and transport costs | Delivery, hauling, equipment use, and production costs ripple into bids |

| Trade and procurement friction | Some materials become harder to source or less predictable to price |

A homeowner often asks, “If material prices settled down, why is my estimate still high?” The answer is usually labor, scheduling pressure, or margin. Construction pricing is not a single dial. It's a dashboard.

The market reset is sticking

Recent global market analysis shows global construction cost inflation rose 4.15% in 2024, with North America at 3.8% and the UK at 3.5%, while skilled labor shortages continued to push costs upward. That same analysis indicates the persistent 3.5% to 4% annual escalation in the US suggests costs aren't returning to pre-pandemic levels, but are settling onto a new, higher baseline, as described in Turner & Townsend's market review.

For property owners, that matters because an insurer's estimate may be anchored to pricing logic that lags behind the bids you're receiving now. Even if the first estimate looked reasonable months ago, the current rebuild market may no longer support it.

Rebuilding after a loss is not like buying from a shelf. You're entering a live market where contractors price current risk, current labor availability, and current supplier terms.

Local stress can be worse than the average

National averages can hide local spikes. Projection-focused market guidance for early 2026 notes that metals and energy-related inputs are under particular pressure, with the ENR Materials Index showing a 4% increase for the 12-month period ending February 2026 compared with 2.4% the prior year. The same guidance warns that tariff-driven scenarios and tech-sector growth could push escalation to 7% to 10% in specific hotspots, above broader regional averages, and recommends contingency funds of 5% to 10% for materials exposed to volatility, according to Skanska's winter construction market trends outlook.

That kind of localized pressure is especially relevant in areas where labor and procurement compete with large commercial and technology projects. Even when a national pricing database shows moderation, your neighborhood contractor may be bidding against a very different local reality.

If you own rental property or investment real estate, it helps to look beyond claim handling and understand how inflation changes property strategy more broadly. BatchData's guide to strategies for real estate during inflation offers a useful owner-side perspective on how inflation affects planning and decision-making.

The Impact on Your Property Insurance Claim

Construction inflation matters in a claim because insurance doesn't pay abstract economics. It pays based on policy language, valuation methods, documented scope, and support for current pricing. If any one of those pieces is thin, the settlement can come in below what rebuilding costs.

Where the first estimate often falls short

Insurance carriers usually begin with a structured estimate. That estimate may rely on pricing software, preset assemblies, standard labor assumptions, and a scoped version of visible damage. That approach creates a starting point, not always a final number.

A real rebuild can be more complicated. Once demolition begins, contractors may find hidden damage, code-related upgrades, specialty trade needs, permit delays, or product availability issues. Even without adding new damage, the cost of completing the same scope may rise because the market changed between the date of loss and the date of repair.

ACV and RCV can feel like two different claims

Policyholders often hear two phrases early in the process:

- Actual Cash Value or ACV. This is generally the depreciated value used for an initial payment under many policies.

- Replacement Cost Value or RCV. This is the amount tied to repairing or replacing with like kind and quality, subject to policy terms and conditions.

When construction costs rise quickly, the distance between those concepts can become painfully obvious. You may receive an ACV payment that already feels lean, then discover the actual replacement cost is higher than everyone expected.

That doesn't always mean the policy is wrong. It can mean the claim needs supplemental support.

Generic inflation adjustments don't solve this

Industry analysis confirms that long-term construction cost inflation typically runs at about double the Consumer Price Index, which means ordinary inflation assumptions can understate what a rebuild really costs. That's why construction-specific cost indices are needed to value rebuilding accurately, as noted in the Turner & Townsend analysis cited earlier.

For a homeowner, the practical takeaway is simple. If your insurer adjusts a claim using broad inflation thinking while your contractor prices actual current construction conditions, the settlement may not reflect the true cost to restore the property.

Watch for underinsurance and policy limit stress

Policyholders can feel trapped. If costs climbed after you bought the policy, your limit may not stretch as far as you expected. A partial loss can become a financing problem. A major loss can expose underinsurance risk.

A few warning signs deserve immediate attention:

- Your bids exceed the carrier estimate early. That often means you need line-by-line review, not a quick verbal dispute.

- Contractors won't honor the insurer's pricing. That suggests the local market has moved beyond the estimate assumptions.

- Your policy limit feels tight before upgrades or unforeseen issues. Limit pressure can appear fast when rebuild costs rise.

- You're being told to proceed, but the numbers still don't work. Starting work without clarifying payment can leave you carrying the gap.

If no qualified local contractor will perform the work for the insurer's number, that's evidence. It's not just frustration.

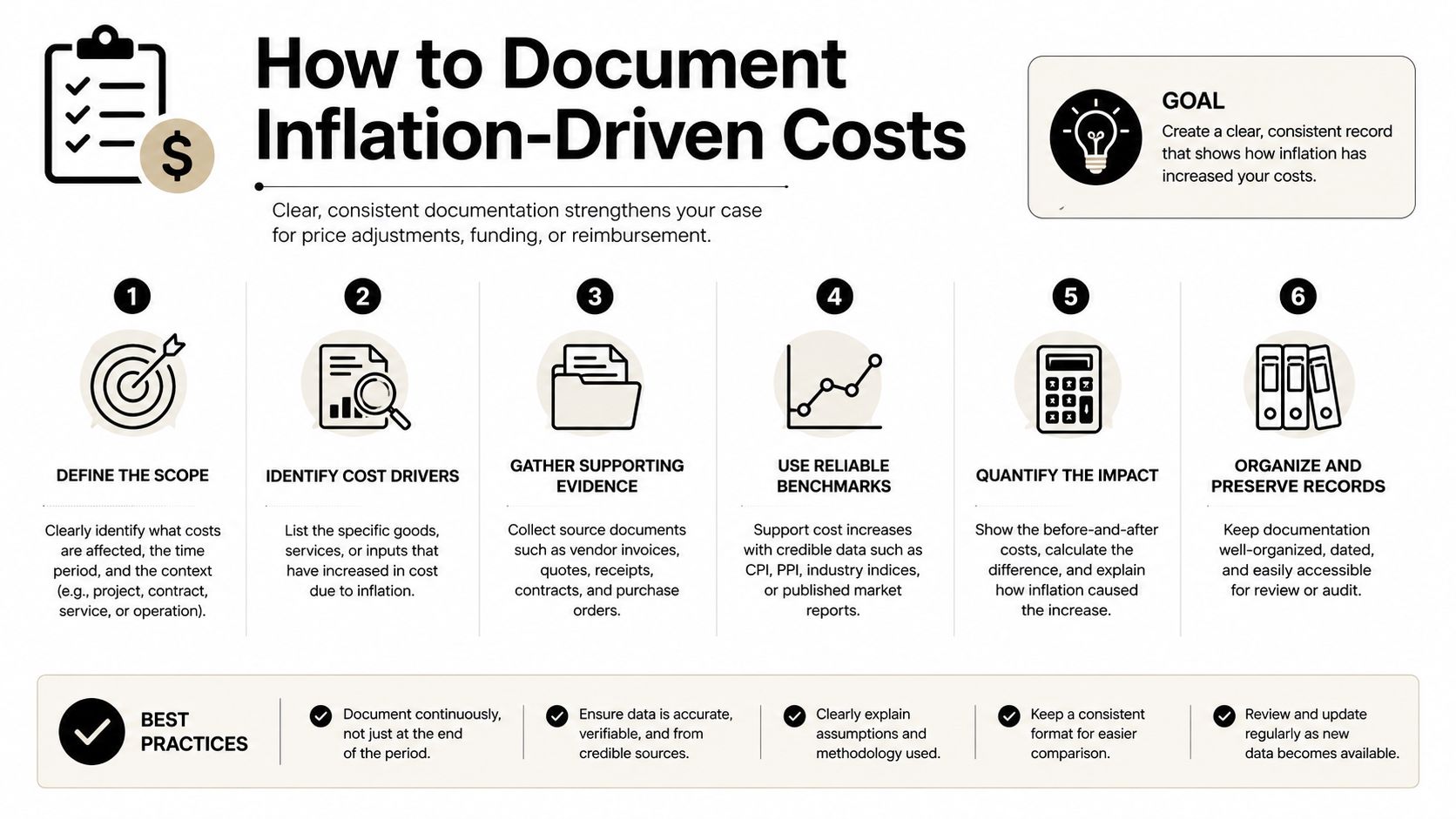

How to Document Inflation-Driven Costs

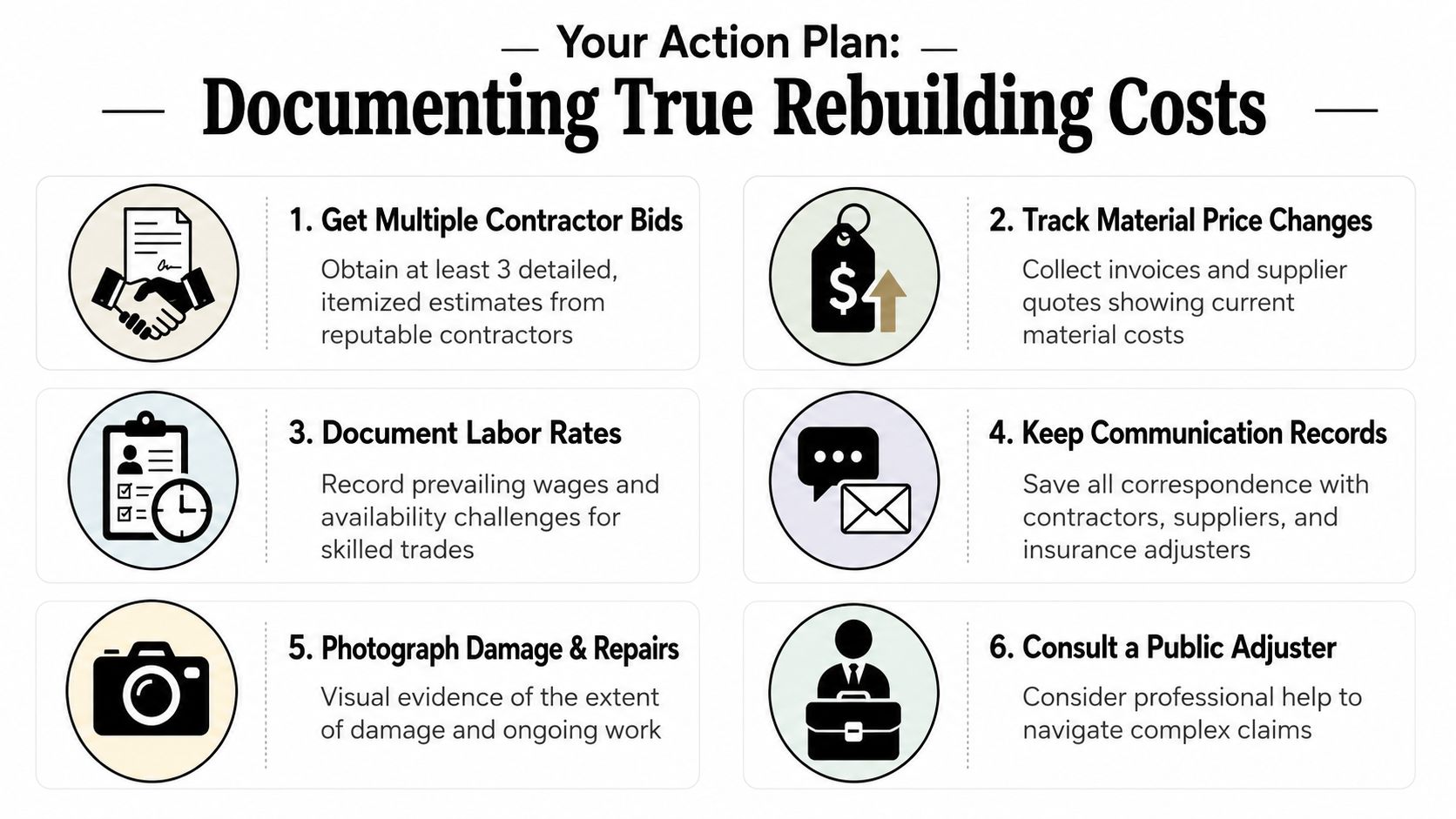

The strongest response to a low estimate is not anger. It's documentation.

Insurance carriers are much more likely to revise a valuation when you present organized proof that current rebuild costs differ from the initial pricing assumptions. A phone call that says, “Everything costs more now,” usually goes nowhere. A package of itemized bids, supplier quotes, trade notes, and dated correspondence is harder to ignore.

Ask for bids that separate the moving parts

Many property owners collect estimates, but they collect the wrong kind. A one-page total price is better than nothing, yet it doesn't show where the dispute sits.

Ask contractors for bids that break out:

- Labor by trade so you can see where pricing pressure is strongest

- Materials with product descriptions or allowances

- Overhead and profit when included

- Lead time notes if pricing depends on availability

- Exclusions and assumptions so the insurer can't dismiss the bid as vague

A large portion of construction inflation comes from shifting contractor and supplier margins, especially during high-demand periods. In those periods, nonresidential inflation can average 8% and residential up to 10%, driven significantly by margin expansion rather than material cost alone, according to Ed Zarenski's construction cost inflation analysis from 2026.

That's one of the most overlooked issues in claims. A carrier may focus on whether lumber or drywall moved, while the difference lies in contractor capacity, supplier terms, and margin changes.

Build a file that tells the story clearly

You don't need a perfect spreadsheet. You need a claim file that a stranger can read and understand.

Use a simple evidence stack:

- Contractor bids with dates, signatures, and line items.

- Supplier quotes or invoices for current materials when available.

- Emails about delays or price validity showing that quotes can expire or change.

- Photos tied to scope so pricing matches actual damage.

- A comparison summary showing where the insurer estimate differs from market bids.

If your loss involves plumbing, mechanical, or trade-heavy repair work, specialized estimating tools can also help contractors explain their pricing logic. For example, some owners find it useful to understand how trade-specific systems such as Exayard plumbing estimating software structure scope and pricing for complex plumbing work. The point isn't to replace the claim process. It's to show that disciplined estimating exists outside the insurer's own platform.

Turn documentation into a supplement, not a complaint

A supplement is a formal request to revise the claim amount based on better evidence. Many policyholders lose momentum at this stage. They gather support, then send scattered emails and hope the adjuster pieces it together.

A better approach is to organize one concise submission. Include a cover note, the revised scope areas, the supporting bids, and a side-by-side comparison. If you want a practical overview of how that process works, this guide on an insurance claim supplement is a solid reference.

Field advice: The clearer your evidence package is, the easier it becomes for an adjuster to justify internal approval for added payment.

Working With Your Insurer on Cost Discrepancies

Once you have evidence, your tone matters almost as much as your paperwork. The goal is to move the claim forward, not to win an argument.

Use calm, specific language

Many adjusters respond better to precision than to pressure. Instead of saying, “Your estimate is way too low,” try language like this:

We've obtained current contractor pricing for the approved repairs, and the bids show a material difference from the initial estimate. Please review the attached line-item support and advise what additional information you need to update the valuation.

That wording does three things. It stays professional. It points to evidence. It invites a response.

If the estimate problem is concentrated in a few categories, say so. If the mismatch runs through labor pricing, material allowances, or overhead and profit, identify those line items directly. Specific disagreements are easier to evaluate than broad complaints.

Submit one organized package

A clean supplement package usually includes:

- A cover letter identifying the claim, property, and reason for review

- A summary sheet listing the disputed categories

- Supporting bids and quotes arranged in the same order as the estimate

- Damage photos and contractor notes where scope is contested

- A request for written response so the next step is documented

If the carrier still resists, ask for a line-by-line explanation of what was rejected and why. That often reveals whether the issue is pricing, scope, policy language, or documentation quality.

Know when appraisal may help

Many property policies include an appraisal clause. It's a dispute-resolution process used when the fight is about the amount of loss rather than whether the loss is covered. Appraisal isn't right for every claim, but it can be powerful when both sides agree damage exists and disagree on value.

Homeowners often avoid appraisal because it sounds formal and expensive. In practice, it can be a structured way to break a valuation deadlock. If you want a straightforward explanation of how that process works, this guide to home insurance appraisal is worth reviewing.

One caution matters here. Don't invoke appraisal just because the conversation feels frustrating. Use it when the dispute is mature, the evidence is assembled, and the issue is valuation.

When to Call a Public Adjuster for Help

Some claims stay manageable. Others turn into a second job.

You should think about professional help when the loss is large, the scope keeps changing, the insurer is slow to respond, or you can't tell whether the estimate reflects your policy and the actual rebuild market. That need becomes even more obvious when you're juggling contractors, temporary living issues, business interruption, or code-related questions at the same time.

A lot of homeowners assume the insurance adjuster assigned to the claim is there to guide both sides equally. In practice, that adjuster works for the insurer. A public adjuster works for the policyholder.

That difference matters when construction cost inflation creates a gap between the initial valuation and the actual cost of rebuilding. A public adjuster can review policy language, evaluate the scope, assemble support, and negotiate from the position of documented claim value instead of guesswork.

You don't have to wait for a denial to ask for help. It can make sense when:

- The numbers don't match local bids

- Your supplement isn't getting traction

- The claim is complex or high value

- You feel too overwhelmed to manage the process yourself

If you're unsure whether it's time, this resource on when to hire a public adjuster can help you make that call.

If you're dealing with a property loss in Oregon or Washington and the rebuilding numbers still don't make sense, NW Claims Management can help you evaluate the gap between the insurer's estimate and today's real-world repair costs. Their team represents policyholders, not insurance companies, and offers free claim evaluations so you can understand your options before making your next move.