The call usually comes after a bad day. A branch came through the roof. A pipe let go upstairs. Wind drove rain behind the siding. You're trying to stop further damage, answer your insurer, and find someone who can start work fast.

Then a contractor slides a form across the table. The title might say “Assignment of Benefits,” “Claim Assignment,” or something similar. You're told it will “help move things along” or “let us deal with the insurance.” In that moment, most property owners in Oregon and Washington aren't asking a legal question. They're asking a practical one: If I sign this, am I still in control of my claim?

That's the right question. Claim assignment isn't just paperwork. It changes who can ask for money, who can receive money, and sometimes who gets to fight about scope, supplements, and unpaid balances. If you understand that before you sign, you'll make better decisions and avoid a lot of expensive confusion later.

Your Contractor Handed You a Form What Is It

A roofer finishes tarping the house. A mitigation company has fans running in the living room. Before they leave, they ask for one more signature. “This just lets us bill insurance directly.”

That explanation is often incomplete.

A claim assignment usually means you transfer some part of your right to collect insurance money to someone else. In residential property losses, that “someone else” is often a contractor, restoration company, or service provider. They aren't just getting permission to do work. They may be getting the right to pursue payment tied to your claim.

For homeowners, the pressure is real. You need drying now. You need emergency roofing now. You may not have the cash to front the work. If you've already had a storm damage roof inspection, you've probably seen how quickly repair decisions start piling up after a loss. The paperwork can move just as fast as the repairs.

What that form often means in plain English

Think of it this way. If your insurer owes money on a covered loss, a claim assignment can redirect some or all of that payment stream away from you and toward the company you signed with.

That's why this isn't the same as a work authorization.

- A work authorization lets a company start mitigation, tarping, board-up, or repairs.

- A payment authorization tells someone how they may be paid.

- A claim assignment can transfer legal rights tied to the claim itself.

Those are very different documents, even when they're stapled together.

Practical rule: If the form affects who can collect insurance proceeds, don't treat it like routine intake paperwork.

Before signing anything, it helps to understand how contractors and adjusters fit into the process. This overview of roof inspection contractors is a useful place to sort out who does what after a property loss.

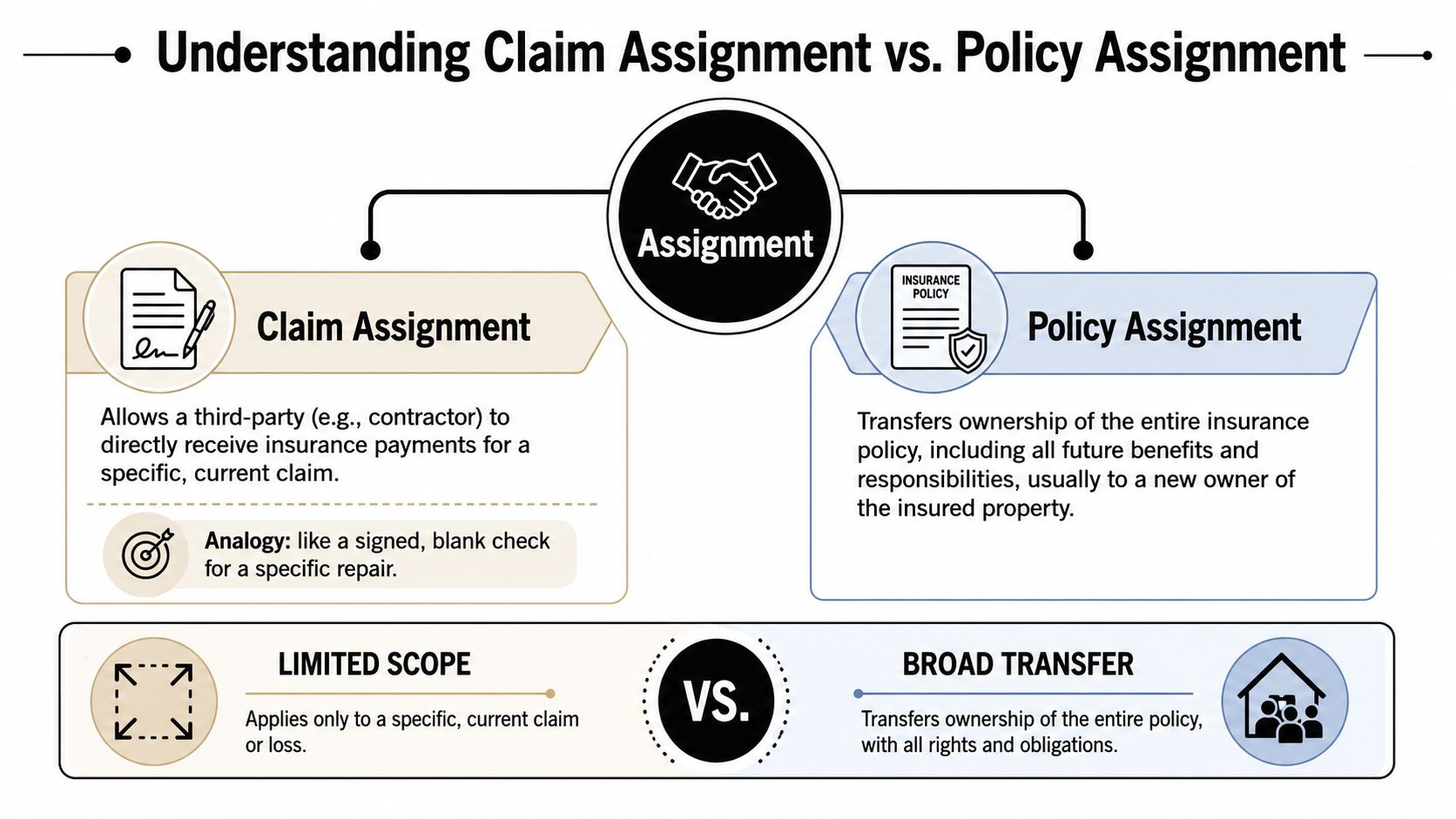

Understanding Claim Assignment vs Policy Assignment

Most confusion starts here. People hear “assignment” and assume it all means the same thing. It doesn't.

A claim assignment deals with rights tied to a specific loss. A policy assignment deals with the insurance policy itself. Those are different legal moves with different consequences.

Claim assignment is limited. Policy assignment is broad

After a loss happens, policyholders may generally assign post-loss claims or benefits even when an anti-assignment clause exists, while the policy itself usually isn't freely transferable without insurer consent, as discussed in this Maryland coverage analysis.

That distinction matters more than most forms make clear.

A claim assignment is closer to saying, “For this water loss, this company can collect certain insurance proceeds.” A policy assignment is closer to saying, “This other party now stands in my place under the insurance contract.” The second one is far broader and usually not what a homeowner intends.

Why the difference matters in real life

When a contractor says, “We're just getting paid directly,” the document should match that limited purpose. If the wording reaches beyond a specific invoice, a defined scope of emergency work, or a particular category of proceeds, your risk goes up.

Here's the simplest analogy I use with property owners. A narrow payment authorization is like writing a check for a known bill. A broad claim assignment can feel more like handing over access to the claim proceeds before the final scope has even settled.

That's where trouble starts.

- Specific claim rights: A narrow document may address payment for drying, roof tarping, or a completed repair scope.

- Future control: A broad document may affect supplements, disputed line items, or later payments tied to the same loss.

- Communication power: The company may try to step into direct negotiations with the insurer.

If you can't tell from the wording whether the form covers one invoice or your broader insurance recovery, stop and ask for a revised version.

A fast test before you sign

Read the nouns. They tell you almost everything.

If the form says “assigns claim,” “assigns benefits,” “assigns proceeds,” “transfers rights,” or “all rights under the policy for this loss,” you're not looking at a simple courtesy payment request. You're looking at a transfer of rights.

If it says the insurer “may pay contractor directly for approved services performed,” that's a different document with a different effect.

The Legal Rules for Claim Assignments in the Northwest

In Oregon and Washington, the first legal question is usually not whether a contractor can ever receive insurance money. Instead, the question is what right you are transferring, and at what stage of the claim.

That distinction matters because a post-loss claim right is different from assigning the policy itself. A homeowner can sign a document after a loss that affects payment for that loss without transferring the entire insurance contract. I make that point often because owners are usually handed one form and told it is routine, even though the wording may reach much further than routine payment handling.

The rule people miss: policy assignment and claim assignment are not the same

Many policies contain anti-assignment language. That does not automatically end the discussion. Courts often draw a line between assigning the policy before a loss and assigning rights tied to a loss that has already happened.

A useful illustration appears in 2.210(d) of the Texas Business & Commerce Code, which lawyers often cite to explain the broader contract rule. A restriction on assigning the contract does not always block assignment of a claim arising from that contract. In plain English, performing the work and collecting money tied to a dispute are separate issues.

That is not Oregon or Washington statutory text. It still reflects the same practical problem I see in Northwest files. The document may be presented as a payment form, while the wording tries to transfer claim rights.

Oregon and Washington owners need to focus on scope, timing, and authority

State-specific disputes usually turn on the wording of the document and the facts surrounding the signature. That is why I tell policyholders to stop treating claim assignment as a clerical step. It is a claim-control decision.

A few facts usually decide how much trouble the form can cause:

- Scope of the transfer. Does it assign payment for completed mitigation, or insurance benefits tied to the entire loss?

- Timing of the signature. Was the claim still developing, with supplements, code issues, or pricing disputes still unresolved?

- Authority given to the contractor. Does the form only authorize direct payment, or does it also let the contractor pursue the carrier in its own name?

- Exposure if there is a dispute. If the insurer questions part of the bill, can the contractor still pursue you for the balance?

Those are not technicalities. They shape who controls negotiations, who receives funds first, and who has room to argue about the scope and value of the loss.

Formality matters more than homeowners are usually told

The law tends to treat assignments seriously because they transfer rights, not just paperwork. If a form is vague, overbroad, or signed before the payment issues are clear, the fight later is usually about interpretation.

That is one reason I prefer precise, limited documents over broad assignment language. Homeowners in Oregon and Washington need room to make claim decisions as facts develop. A large water loss or fire claim rarely stays static. The estimate changes. The repair plan changes. The insurer's position changes. A broad assignment signed on day one can age badly by day thirty.

For a plain-language discussion of protecting your settlement check, the same general caution applies here. Signing over payment rights sounds simple until there is a disagreement about scope, fees, or who gets paid first.

The practical takeaway in Northwest claims

In the field, the legal fight is rarely about an abstract right to assign something. The harder question is whether signing that form helps or hurts your recovery strategy.

For policyholders in Oregon and Washington, that strategy matters. If the claim is still being adjusted, a public adjuster protects your position far better than a contractor asking for control over proceeds. Contractors repair property. They do not represent your full financial interest in the claim.

If you are trying to sort out who is handling what on a file, this explanation of third-party administrator companies helps clarify the roles. That context matters because homeowners often assume everyone touching the claim is aligned with their interests. They are not.

The safest rule is simple. Treat any assignment form as a legal transfer of rights until the wording proves otherwise. In Oregon and Washington, that caution is not paranoia. It is good claim practice.

Why Signing a Claim Assignment Can Be Risky

The biggest risk is loss of control.

Once you assign claim rights, even partially, you may no longer be the only person steering the payment side of the file. That can create friction with your insurer, with your contractor, and eventually with your own budget.

You may give up leverage before the scope is settled

Early in a claim, the numbers are fluid. Emergency drying turns into tear-out. Roof repair turns into decking issues. Smoke cleaning turns into contents questions. If you sign away rights too early, you may discover later that the document reached further than the job you thought you were approving.

That matters because legal analysis in 2024 raised a question many homeowners never hear about: not just whether a claim can be assigned, but which benefits are already vested, which are still contingent, and what documentation is required, as discussed in this analysis of unaccrued or contingent benefits.

In plain terms, some money may be clearly tied to completed work. Other money may depend on future approvals, supplements, replacement decisions, code issues, or later documentation. If your assignment language is broad, you may be transferring rights you didn't realize were still in play.

Disputes get messier, not simpler

Contractors often present claim assignment as a way to reduce hassle. Sometimes it does the opposite.

If the insurer questions price, scope, causation, or necessity, you can end up with a three-corner dispute:

- The contractor says the carrier underpaid.

- The carrier says the bill is unsupported or outside coverage.

- You are stuck in the middle, especially if the document doesn't clearly limit your personal responsibility.

That's why homeowners should spend a little time learning about protecting your settlement check before signing over payment rights to anyone. The legal context differs, but the core caution is the same. Once someone else controls the flow of settlement funds, your flexibility narrows.

A document that promises convenience can become a problem if it separates payment control from your ability to approve scope and pricing.

Broad forms create practical claim problems

These are the trouble spots that show up over and over:

- Open-ended benefit language: The form doesn't cap payment to a defined job.

- Direct negotiation language: The company claims authority to deal with the insurer beyond billing.

- Supplement ambiguity: It's unclear who controls later payments or disputed additions.

- Collection pressure: If insurance doesn't pay what the contractor wants, you may still face demands.

Homeowners also need to watch for insurer tactics while all this is unfolding. If you're already dealing with delay, scope pushback, or shifting explanations, this guide to insurance adjuster tricks helps identify pressure points before they get worse.

Safer Ways to Authorize Payments to Contractors

You usually don't need a claim assignment to get work started or to pay a legitimate contractor fairly. There are safer ways to handle payment while keeping control of the claim in your hands.

Direction to pay keeps the purpose narrower

A Direction to Pay is often the cleaner option. Instead of transferring claim rights, you authorize the insurer to send a specific approved payment, or a payment tied to a defined invoice or completed scope, directly to the contractor.

That arrangement doesn't have to give away your right to question pricing, dispute incomplete work, or manage the broader claim. It's a payment instruction, not a wholesale transfer of your benefits.

This is usually a better fit when:

- emergency mitigation was necessary and already documented

- the work scope is specific and priced

- you want the contractor paid without surrendering claim control

- supplements or disputed items may still arise later

Public adjuster representation solves a different problem

A contractor repairs property. A public adjuster handles the insurance claim.

Those roles should stay distinct. If the challenge is valuation, documentation, policy interpretation, scope presentation, or insurer negotiation, a public adjuster works for the policyholder, not for the repair vendor. One option in Oregon and Washington is NW Claims Management's public adjuster service, which represents policyholders through the claim process while contractors remain contractors.

That separation helps because the person arguing coverage and value isn't also the one billing for repairs.

Claim Payment Options Compared

| Feature | Assignment of Claim | Direction to Pay | Public Adjuster Agreement |

|---|---|---|---|

| Who controls the claim | Often shared or partly transferred | Policyholder keeps claim control | Policyholder keeps ownership, adjuster represents policyholder |

| Purpose | Transfers some payment or claim rights | Authorizes payment for defined work | Authorizes claim advocacy and negotiation |

| Risk of overbroad language | High if poorly drafted | Lower if limited to invoice or scope | Different risk profile, focused on representation terms |

| Effect on future benefits | May reach supplements or contingent proceeds if broad | Usually limited if drafted correctly | Does not assign repair proceeds to a contractor |

| Best use case | Rarely ideal for homeowners | Paying a contractor for approved work | Managing a complicated or underpaid property claim |

What works better in practice

For most property losses, the safer sequence looks like this:

- Authorize emergency work clearly

Use a work authorization that describes immediate services. - Keep claim rights with the policyholder

Don't transfer them just to make billing easier. - Approve payment in stages

Tie payments to actual work performed and documented. - Use separate professionals for separate jobs

Contractors repair. Public adjusters value and negotiate claims.

That structure preserves accountability. If repairs are disputed, the repair dispute stays a repair dispute. If the insurer underpays, the claim advocate can push back without the payment rights being tangled up in a contractor form.

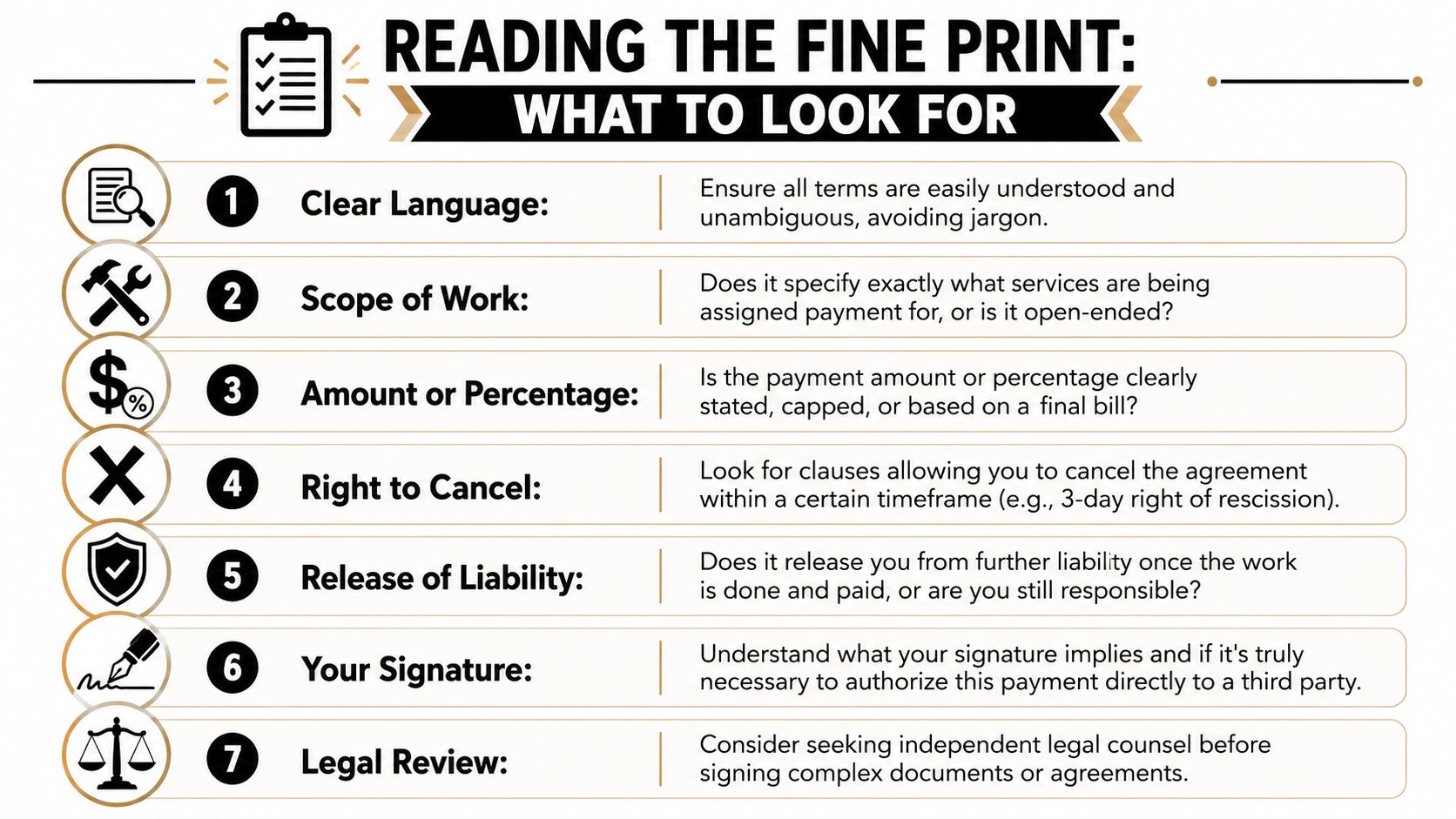

Reading the Fine Print What to Look For

If a company puts a signature page in front of you, slow the process down. You're not being difficult. You're doing what careful policyholders do.

The federal Assignment of Claims framework shows how formal assignments can be. Under that framework, assignment applies only when contract payments aggregate $1,000 or more, and even then the process is limited to specified conditions under FAR Subpart 32.8. Different setting, same lesson: assignment is not casual paperwork.

What safer language looks like

A narrower payment clause usually sounds something like this:

The insured authorizes the insurer to issue payment directly to Contractor for approved services actually performed at the property, limited to the invoiced amount for those services.

That kind of wording is tied to work performed and payment amount. It doesn't automatically transfer the whole claim.

By contrast, risky language often includes phrases like “assigns all benefits,” “transfers any rights to insurance proceeds,” or “authorizes contractor to pursue, negotiate, collect, or litigate the claim.” That's where you should pause.

Red flags worth circling with a pen

When reviewing the form, look for these issues:

- No clear scope: The document doesn't say exactly what work the payment relates to.

- No payment limit: It assigns benefits without tying them to an estimate, invoice, or approved amount.

- Rights language instead of payment language: It talks about “claims,” “benefits,” or “proceeds,” not just direct payment.

- One-sided collection terms: The contractor can pursue payment broadly, but your rights to dispute work are vague.

- Bundled paperwork: Work authorization, payment assignment, and broad legal language appear in one packet.

If you're vetting vendors at the same time, these practical notes on Turning Point Ventures' insights can help you ask better questions before paperwork becomes a problem.

One more thing to compare against your policy

Always read the proposed document alongside your coverage and limits. This plain-language guide to insurance policy limits explained helps homeowners understand where payment can and can't come from under the policy, which makes overbroad assignment language easier to spot.

Your Claim Assignment Questions Answered

Can a contractor require me to sign a claim assignment before starting work

A contractor can make that request. You still have a choice.

For Oregon and Washington homeowners, that choice matters more than it first appears. A broad assignment can shift control of part of the claim before the full scope of damage, coverage position, or repair pricing is clear. In many cases, emergency mitigation or urgent repairs can start under a work authorization, with payment handled separately once the claim is better defined.

If a contractor says broad assignment language is required before any work begins, treat that as the contractor's business policy. It is not automatically the safest option for your claim.

I already signed one. What should I do now

Start by getting a complete copy of every page you signed, including anything attached by reference. Then read the assignment closely for three points. What rights were transferred, whether the form can be canceled, and whether payment is tied to specific work or a specific amount.

Move quickly, but do not panic.

I tell policyholders the same thing in this situation. Verbal explanations do not control a written contract if the wording on the page is broader. If the document gives the contractor collection rights, claim rights, or the ability to settle or pursue payment beyond completed work, get legal advice or have the form reviewed before the dispute gets more expensive.

Does claim assignment change my deductible responsibility

Usually, no.

Your deductible comes from your policy. The contractor's payment rights come from your contract. Those are separate obligations, and signing an assignment usually does not make the deductible disappear. If anyone suggests otherwise, ask them to put that promise in writing with clear terms showing who is absorbing that cost and under what conditions.

That is a good point to slow down. A form that looks like a payment shortcut can create confusion about who owes what at the end of the job.

Can any assignment be signed at any time

No. Timing and context matter.

As noted earlier, federal law places strict limits on the assignment of certain claims against the government, and those rules only allow assignment after specific claim and payment milestones are met. That rule applies in a particular legal setting, but the practical lesson for homeowners is still useful. Signing away rights early, before coverage, pricing, and scope are settled, creates more risk for the policyholder.

For Oregon and Washington claims, the safer course is usually to keep claim rights with the policyholder unless there is a narrow, well-defined reason to transfer a specific payment interest. That preserves your ability to question the scope, challenge underpayment, and make strategic decisions based on your own financial recovery, not someone else's collection rights.

The safest position for most homeowners is simple. Authorize the work you want done. Keep control of the claim unless you fully understand what rights are being transferred and why.

If you are being pressured to sign fast, pause long enough to get the form reviewed. A short delay usually costs far less than untangling a payment dispute after the work is underway.

If you want a second set of eyes before signing anything, NW Claims Management reviews property claims for Oregon and Washington policyholders and can help you sort out the difference between repair paperwork, payment authorization, and a true claim assignment before your rights get tangled up.