The first night after a house fire rarely feels real. You're answering questions from the fire department, trying to figure out where everyone will sleep, calling family, finding medications, and staring at a home that no longer feels stable. Then the insurance process starts, often before you've had a chance to catch your breath.

That's where a fire damage public adjuster can make a real difference. Not because every claim needs one, and not because every insurer acts unfairly, but because fire claims are unusually easy to under-document. Burned rooms are obvious. Smoke migration, water from suppression, warped framing, damaged contents, and temporary living costs are not.

If you're in Oregon or Washington, the practical question isn't just “Should I file a claim?” You already are. The better question is, “Who is going to build this claim correctly, and is it worth bringing in help now?”

After the Fire The First 24 Hours

In the first 24 hours, most families are forced into two jobs at once. They're dealing with a personal emergency, and they're being asked to start an insurance file. Those are very different tasks, and trying to do both at the same time is where mistakes begin.

The immediate priorities are simple. Make sure everyone is safe. Secure emergency housing if you can't stay in the home. Protect the property from further damage if the fire department or your contractor says it's safe to do so. Start a basic record of what happened, who responded, and what you were told.

The claims side gets complicated fast. The U.S. Fire Administration reported that heat and flames caused more than $3.8 billion in residential building fire losses in 2021 (Tiger Adjusters). That scale matters because fire losses often involve more than charred materials. A file may need to account for smoke, soot, water intrusion, damaged contents, and displacement costs.

What to do before the scene changes

Once cleaning crews, mitigation vendors, and contractors start moving through the property, the original condition disappears. That's why the earliest documentation matters so much.

- Photograph first: Take wide shots of each room, then closer images of damaged surfaces, contents, appliances, vents, and windows.

- Save temporary living receipts: Hotel stays, meals, clothing, pet boarding, and other extra costs may become part of the claim if your policy allows it.

- Don't rush disposal: Burned or smoke-affected items can be evidence. Don't throw things away until they're documented.

- Write down conversations: Names, dates, and what each person said will help later if the claim gets disputed.

If smoke odor is lingering through the home, this guide from Purified Air Duct Cleaning on smoke removal gives homeowners a useful overview of why smell often remains even after obvious cleanup.

Practical rule: If a loss involves fire, smoke, and water, assume the claim is broader than it looks on day one.

A public adjuster enters the picture here as a policyholder-side advocate. Not a restoration contractor, and not the insurance company's representative. Their job is to help organize the loss, preserve evidence, review coverage, and keep the claim from being defined too narrowly at the start. If you need a step-by-step checklist during this stage, NW Claims Management has a useful guide on what to do after a house fire insurance loss.

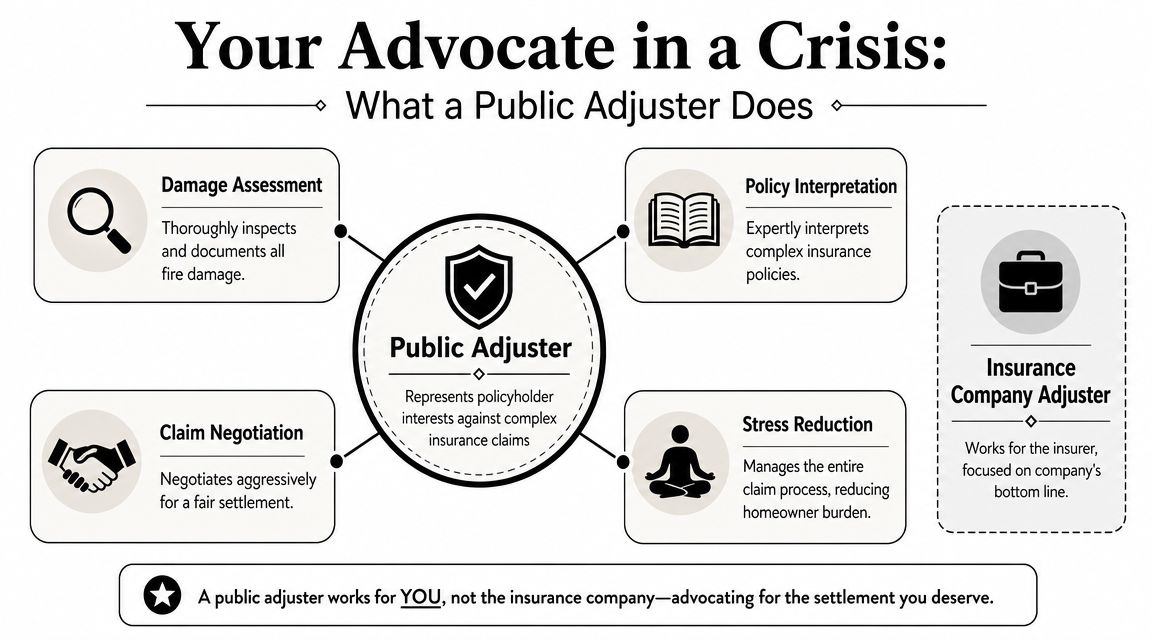

Your Advocate in a Crisis What a Public Adjuster Really Does

Most homeowners meet an adjuster only after a major loss, so the roles are easy to confuse. The insurance company's adjuster works for the insurer. A public adjuster works for the policyholder.

That distinction matters most in a fire claim because the file isn't just about what burned. It's about what the policy covers, how the damage is categorized, and whether each category is documented in a way the insurer will recognize.

The real job is part translator and part claim manager

A fire damage public adjuster usually does three things at once.

First, they reconstruct coverage. Industry guidance describes this technical edge clearly: adjusters review terms and limits, identify recoverable areas such as dwelling, contents, debris removal, and additional living expenses, and translate physical damage into categories the insurer can evaluate and pay (Fire Cash Buyer).

Second, they build the proof. A family may say, “The whole house smells like smoke.” That may be true, but claims are paid on evidence. The adjuster turns that concern into photos, inventories, estimates, reports, and written support.

Third, they handle negotiation. That includes responding to insurer questions, clarifying scope disagreements, and pushing back when parts of the loss are minimized or left out.

What that looks like in practice

Think of a public adjuster as the quarterback for the claim. The contractor can price repairs. The mitigation company can dry out and clean. Specialized consultants may test or inspect. But someone still has to connect those moving parts to the insurance policy and present one coherent claim.

That often includes:

- Policy review: Reading the actual policy language, not just the summary page.

- Scope organization: Separating structural damage, contents loss, cleanup issues, and living expense claims.

- Evidence management: Making sure documents, photos, estimates, and inventories support one another.

- Insurer communication: Keeping discussions focused on documented loss rather than rough assumptions.

The strongest fire claims are built, not improvised.

For a side-by-side explanation of who represents whom, this comparison of public adjuster vs insurance adjuster is worth reviewing before you decide who should manage your file.

What a public adjuster does not do

A good adjuster doesn't replace every other professional. They don't perform reconstruction. They don't remediate smoke. They don't serve as legal counsel. They also shouldn't promise a certain settlement number before they've reviewed the loss and the policy.

What they can do is keep the claim from drifting. After a fire, drift is expensive. It shows up as missing contents, under-scoped smoke damage, unpaid debris costs, and living expenses that never get presented correctly.

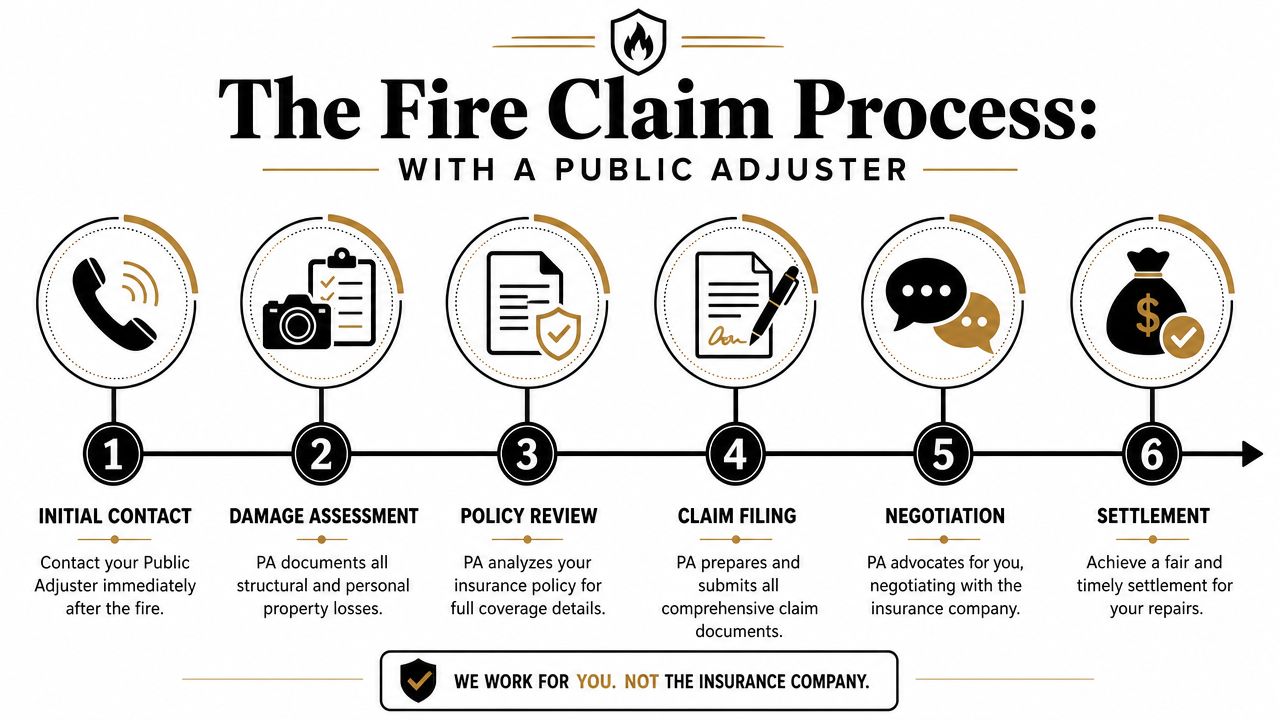

The Fire Claim Process from Start to Finish

A well-run fire claim follows a sequence. Not because insurance companies require a tidy narrative, but because the quality of the result depends on the order of the work.

Step one is preserving the scene

The first serious task is scene documentation and loss scoping. Independent guidance on fire claims describes a rigorous workflow that starts with photos, video walkthroughs, measurements, and a room-by-room inventory, because hidden damage such as heat distortion in framing, smoke infiltration into HVAC systems, and water inside walls can be missed if the file is built too loosely (Sill).

That means walking the property carefully, not just looking at the room where the fire started. Kitchens, attics, crawlspaces, duct runs, closets, and adjacent rooms often tell the fuller story.

Then the contents claim starts

For many homeowners, contents are the most draining part of the process. Structural damage is visible. Personal property takes time.

A thorough contents inventory usually includes:

- Item identification: Brand, model, serial number, and a plain description where available.

- Condition before loss: Whether the item was new, older but functional, repaired, upgraded, or custom.

- Location in the home: Which room or storage area it came from.

- Support documents: Photos, receipts, warranties, account history, or family photos showing ownership.

This is slow work. It's also where many do-it-yourself claims lose value, because general descriptions like “clothes,” “tools,” or “kitchen stuff” don't tell the full story.

Repair pricing and claim assembly

Once the damage is scoped, the next phase is turning observations into a claim package. That often means gathering contractor bids, line-item estimates, specialty cleaning recommendations, and any needed third-party evaluations.

A solid file usually contains these core pieces:

| Claim Component | What it should show | Why it matters |

|---|---|---|

| Structural scope | What parts of the building were damaged | Prevents repair omissions |

| Contents inventory | What personal property was lost or contaminated | Supports item-by-item valuation |

| Supporting estimates | Contractor or specialist pricing | Grounds the claim in current repair realities |

| Coverage mapping | Which policy section applies to each loss | Reduces confusion during review |

A rushed inspection often finds obvious damage. A disciplined claim file finds payable damage.

After submission, negotiation begins. That's usually not one meeting and one check. It's a series of questions, revisions, supplemental items, and coverage discussions. Homeowners who want a broader overview of timelines and checkpoints can review this guide to the home insurance claim process.

Where hidden damage gets missed

What works is objective support. Photos of soot at a register. Notes showing smoke travel. Moisture evidence after suppression. Estimates that include cleanup and replacement where contamination can't be reasonably resolved.

What doesn't work is arguing in general terms. Saying “everything is affected” may feel true after a fire, but broad statements don't carry a claim. Specific proof does.

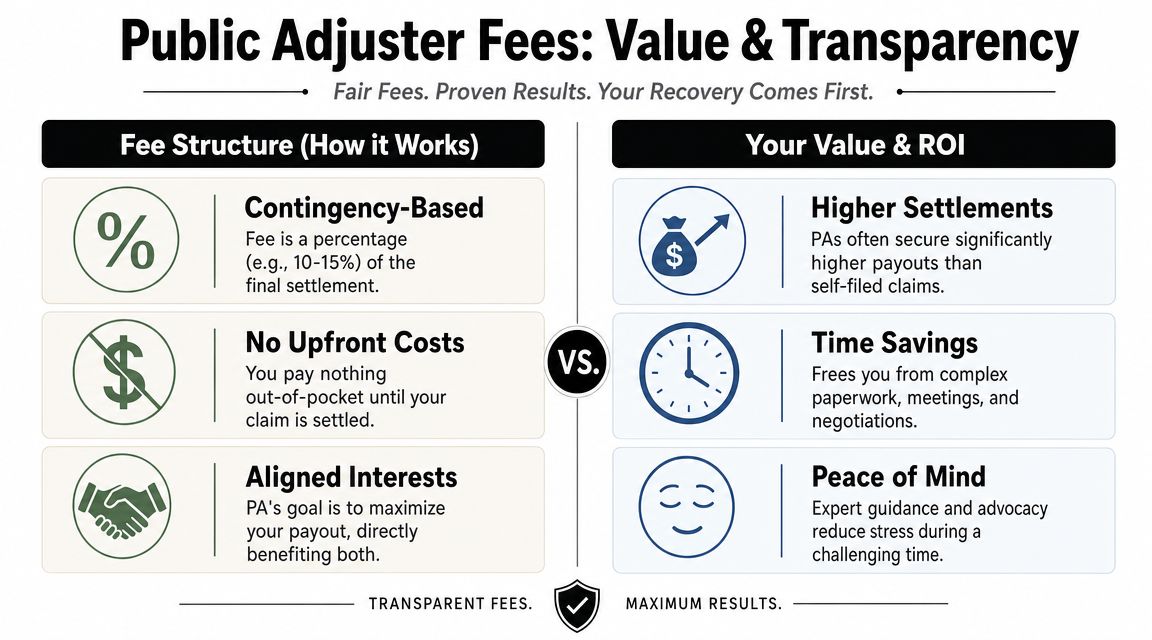

Understanding Fees and Calculating Your Real Value

The kitchen is blackened, the bedrooms smell like smoke, and a mitigation crew is asking for approval while your insurer is still deciding what belongs in the scope. That is usually when the fee question becomes urgent.

Most fire damage public adjusters work on a contingency fee. You do not pay hourly as the claim unfolds. The adjuster is paid from the settlement, and the percentage depends on the state, the size of the loss, and sometimes the stage at which the adjuster is hired. The Florida Association of Public Insurance Adjusters describes contingency fees as a common model for public adjuster compensation (FAPIA).

Fees matter. Net recovery matters more.

A family does not benefit from a larger gross settlement if the unpaid portions of the loss still fall on them. The right way to judge value is to compare the fee against what the adjuster is likely to add back into the claim. In fire losses, that often means smoke contamination the carrier treated as light cleaning, contents that were undervalued or omitted, code items, overhead and profit, specialty testing, and additional living expense documentation that was never fully presented.

That is also why broad promises are not useful. A public adjuster earns the fee by proving items that are easy to miss, easy to minimize, or hard for a homeowner to document while the family is displaced.

When the fee is usually justified

Hiring a PA often makes financial sense when the claim involves proof problems, not just visible damage. Common examples include:

- Mixed loss conditions: Fire, smoke, soot, and water from suppression all affected different parts of the home.

- Whole-house smoke migration: The insurer accepts the fire occurred but disputes how far contamination traveled.

- Large contents claims: Clothing, furniture, electronics, and soft goods must be evaluated item by item.

- Hidden or technical damage: HVAC contamination, insulation replacement, odor sealing, or specialty cleaning is disputed.

- Long displacement: Additional living expenses need to be tracked carefully over months, not days.

- Scope gaps: The insurer's estimate leaves out rooms, materials, detach and reset work, or code-related costs.

In these files, the fee is often outweighed by what gets added, corrected, or properly documented.

When self-handling may be reasonable

Some fire claims are limited enough that a homeowner can handle them without paying a percentage fee. That is more realistic when the fire was contained to a small area, smoke did not spread far, contents loss is modest, and the insurer is responding with a complete scope and clear communication.

The Illinois Department of Insurance notes that public adjusters usually charge a percentage of the settlement and that the policy does not pay that fee for you (Illinois Department of Insurance guidance on public adjusters). That makes this a math decision, not a stress decision.

Use a simple test: if you can clearly identify the damage, value the loss with reliable estimates, and keep up with the paperwork without missing deadlines, self-handling may work. If the claim depends on proving contamination, rebutting a narrow scope, or organizing a large contents file, professional help usually has a stronger case.

A practical way to calculate real value

Before signing, ask one question: What part of this claim is currently underdeveloped, underpriced, or denied, and how will you prove it?

Then evaluate the answer in four buckets:

| Value Area | What to look for | Why it changes the math |

|---|---|---|

| Scope expansion | Missed rooms, omitted materials, incomplete demolition or cleaning | Small omissions add up fast in fire claims |

| Pricing correction | Contractor pricing, specialty cleaning, code upgrades, contents valuation | Underpriced work reduces settlement even when coverage is accepted |

| Hidden damage proof | HVAC contamination, smoke spread, sealed cavities, insulation, odor remediation | These items are often disputed unless documented carefully |

| Time and claim control | File organization, supplemental submissions, meeting management, deadline tracking | A strong file reduces costly mistakes and missed recoverable items |

A good adjuster should be able to point to likely pressure points in your claim and explain the proof strategy in plain language. If the answer is only “we get more money,” keep looking.

Homeowners who want a clearer explanation of fee structures and contract terms can review this breakdown of public adjuster cost. If you are comparing claim types, the economics differ from hiring a public adjuster for roof damage because fire losses usually involve contamination, contents, and living-expense issues that expand the documentation burden.

Decision rule: The harder it is to prove the full extent of damage, the more likely a public adjuster adds measurable value after fees.

How to Choose the Right Public Adjuster for Your Claim

At 8 p.m., a family is standing in a driveway, smoke still hanging in the air, and three different people have already offered to “help with the claim.” That is usually the moment bad hiring decisions get made. After a fire, the right public adjuster is not the person who talks fastest or promises the biggest check. It is the one who can explain, in plain language, how they will prove your loss, where the insurer is likely to push back, and whether hiring them makes financial sense after fees.

Start with a simple question. What is hard about this claim? If the fire was small, the scope is obvious, and the carrier is responding reasonably, you may not need much help. If smoke moved through the HVAC system, cabinets must be detached to check hidden contamination, contents are spread across several rooms, or the insurer is minimizing demolition and cleaning, professional representation often pays for itself. A good adjuster should be able to say exactly which disputed items they expect to document and how they plan to support them.

Interview them like you're hiring someone to handle a six-figure file

Ask direct questions. Then listen for specifics, not confidence.

| Vetting Category | Key Question | What a strong answer sounds like |

|---|---|---|

| Licensing | Are you licensed in Oregon, Washington, or both for this claim? | A clear yes, with license details you can verify |

| Fire claim experience | How often do you handle residential fire losses? | They describe recent fire work, not just “property claims” in general |

| Damage proof | How do you prove smoke spread, odor, insulation impact, and HVAC contamination? | They explain inspection steps, documentation, and when outside experts are needed |

| Claim strategy | Where do fire claims usually get underpaid? | They point to scope gaps, cleaning limits, code issues, contents, or ALE documentation |

| Communication | Who is my contact, and how often will I hear from you? | You get a real process, with names and timing |

| Contract terms | How is your fee calculated, and when is it earned? | The fee is explained plainly, with no evasive language |

| Existing claim takeover | Can you help if I already gave a statement or accepted part of the scope? | They explain what can still be corrected and what may be harder to reopen |

One practical test helps. Ask them to walk through your house, room by room, and tell you where they expect disagreement. An experienced fire adjuster usually spots pressure points quickly. Attic insulation. Return air contamination. Detached and reset items. Contents handling. Temporary repairs versus permanent repair scope. If all you hear is “we get more money,” keep interviewing.

Watch for answers that create risk

Some responses are enough to end the conversation.

- “Don't worry about the paperwork.” You should review the contract, cancellation terms, fee percentage, and what happens if you already have partial payments.

- “Fire claims are basically the same.” They are not. A stovetop flare-up, an electrical wall fire, and a heavy smoke loss with little visible burning all require different proof.

- “We can figure out the details later.” Fire claims are won on details early. Photos, site notes, contents logs, cleaning protocols, and expert input matter.

- “You don't need to be involved.” You do. A good adjuster reduces your burden, but you still need to understand decisions that affect your home and your settlement.

If you are comparing options close to home, look for a local public claims adjuster near you who can explain regional contractor pricing, inspection access, and the claim habits they see in your area.

The vetting standard also changes by claim type. The issues involved in hiring a public adjuster for roof damage overlap on licensing and fees, but fire losses usually involve more contested categories at once, including smoke migration, contents, cleaning, code items, and additional living expense.

NW Claims Management is one Oregon-based firm homeowners may encounter for fire claim documentation and negotiation in Oregon and Washington. Whether you speak with that firm or another one, use the same standard. Ask how they prove hidden damage, how they handle supplements, what their fee applies to, and when they would tell a homeowner that hiring a public adjuster is not worth the cost. That last answer tells you a lot.

Oregon and Washington Specific Rules You Must Know

After a fire, out-of-state contractors, consultants, and adjusters often appear quickly. Some are legitimate. Some are not. In Oregon and Washington, licensing is not a small detail. It's one of the simplest ways to protect yourself.

Verify before you sign

A public adjuster in these states should be properly licensed for the work they're performing. Before signing a contract, verify that the person and firm are authorized to represent policyholders in your state.

Check with:

- Oregon regulators: Confirm licensing through the Oregon Division of Financial Regulation.

- Washington regulators: Confirm licensing through the Washington Office of the Insurance Commissioner.

- Contract details: Make sure the written agreement names the correct business entity and explains the fee arrangement.

This step matters because post-loss stress makes people vulnerable to pressure. A homeowner who's displaced, exhausted, and trying to save a damaged property is more likely to sign quickly. Slow down enough to verify who you're hiring.

Local compliance matters in practical ways

State compliance is not just paperwork. A licensed local adjuster should understand how claims are handled in the region, how to communicate with carriers operating in Oregon and Washington, and how to avoid procedural mistakes that can complicate a file.

That's also why local availability matters. A fire claim often needs site visits, follow-up inspections, and coordination with contractors and vendors. Searching for a claims adjuster near me can help you start with firms that serve your area rather than chasing storm-chasing or disaster-chasing solicitations.

If someone asks you to sign before they clearly identify their license, fee terms, and role, that's a reason to stop the conversation.

Frequently Asked Questions About Fire Damage Claims

How do you prove smoke damage if the insurer says the house is clean enough

This is one of the hardest disputes in a fire claim because it often turns on competing opinions. The homeowner smells smoke or sees residue. The insurer says cleaning was sufficient.

Industry guidance points to a more technical answer. Public adjusters may use forensic investigation and third-party reports to validate contamination in materials and systems when subjective visual review isn't enough (For The Public Adjusters). That can matter for HVAC systems, porous materials, insulation, contents, and areas far from the flame origin.

What works is narrowing the question. Don't argue “the whole house is bad” unless you can support it. Show where contamination remains, how it migrated, and why ordinary cleaning doesn't resolve the issue.

Is a public adjuster worth it for a smaller fire

Sometimes yes, sometimes no.

A smaller fire may still create a complicated claim if smoke moved widely, if cabinets and contents were affected, if water entered hidden cavities, or if your living expenses are piling up while repairs stall. On the other hand, a limited loss with straightforward repair pricing and no major contents dispute may not justify a contingency fee.

Use a common-sense test:

- Hire help sooner if the claim is becoming technical, disputed, or too time-consuming to manage well.

- Consider handling it yourself if the loss is narrow, well documented, and progressing without serious disagreement.

The issue isn't just claim size. It's claim complexity.

Can I bring in a public adjuster after I already started the claim

Yes, in many cases. Homeowners often call after the first inspection, after a low scope, or after they realize the contents inventory is overwhelming.

At that point, the adjuster's role is often different from a day-one assignment. They may need to review what was already submitted, identify what was missed, and determine whether the claim can still be strengthened with supplemental documentation or additional support.

What are the most common mistakes homeowners make after a fire

The biggest ones are usually practical, not legal.

- Throwing items away too early: Once evidence is gone, it's harder to prove the loss.

- Accepting a narrow scope too soon: Early estimates don't always include the full damage picture.

- Underestimating contents work: Contents claims are labor-intensive and often underdeveloped.

- Failing to track displacement costs: Temporary living expenses can be significant if your policy allows them.

- Signing with the wrong professional too quickly: Not every contractor, cleaner, or adjuster is the right fit.

What should I do if I feel overwhelmed and behind

That feeling is normal after a fire. The answer is to get organized, not to give up. Gather your policy, claim number, photos, receipts, and any insurer correspondence into one place. Write down what parts of the claim feel unresolved. Then get a professional review if you need one.

A clear second opinion can tell you whether the file is on track, under-scoped, or worth escalating.

If you're dealing with a fire loss in Oregon or Washington and need a calm, honest review of the claim, NW Claims Management offers no-obligation evaluations for policyholders who want to understand their options before the process drifts any further.