A sprinkler line lets go at 2:00 a.m. on the third floor. By sunrise, water has moved through ceiling cavities, elevator lobbies, tenant suites, and the HVAC path. The first calls usually go to maintenance, a restoration contractor, and the insurer. By noon, another problem appears. No one agrees yet on the full scope, who pays for what, how long tenants will be displaced, or how lost income will be documented.

That's the moment commercial property restoration stops being a cleanup story and becomes a financial recovery project.

Owners in Oregon and Washington often find out the hard way that fixing the building is only half the job. The other half is proving what happened, preserving the claim, documenting business interruption, and pushing back when the insurer's first scope leaves out real costs. If you only manage drying and demolition, you can still end up with a repaired property and an underfunded claim.

What Is Commercial Property Restoration Really About

Commercial property restoration starts with visible damage, but it doesn't end there. A soaked office floor, a smoke-damaged restaurant, or a vandalized nonprofit facility creates three parallel problems at once: physical damage, operational disruption, and insurance valuation.

The scale of this work matters. The global property restoration services market is projected at USD 55.81 billion in 2026 according to the property restoration services market report from Research and Markets. That tells you something important. This isn't a fringe service category. It's a large recovery system tied directly to disasters, claims handling, and the need to get buildings back into service fast.

The building problem and the money problem

Owners usually see the first problem immediately. Carpet is saturated. Drywall is wicking moisture. Smoke odor is moving into adjacent suites. A contractor can start extraction, containment, and stabilization.

The second problem is less visible and often more expensive. Rent may stop. Staff may be displaced. Tenants may demand answers before you have them. Vendors still expect payment. The insurer may issue a reservation, ask for more documentation, or scope the damage too narrowly.

Practical rule: If the loss affects operations, treat documentation as part of restoration, not as office paperwork you can catch up on later.

That's why I tell owners to think of commercial property restoration as two jobs running at the same time. One team restores the property. Another team has to restore the claim.

What owners need in the first week

A smart first-week approach usually includes:

- Emergency mitigation: Stop further damage and stabilize the site.

- Loss documentation: Photos, moisture readings, damaged area mapping, tenant impacts, and expense tracking.

- Claim strategy: Confirm how building damage, contents, and income loss will be presented and supported.

- Decision discipline: Avoid signing broad authorizations before someone reviews scope, pricing, and claim implications.

For a practical contractor-side reference on emergency drying and cleanup expectations, this guide for Phoenix business owners is useful because it reflects the urgency business owners face in the first hours after a water loss.

Owners who need help organizing the claim side of the loss often benefit from formal claim management solutions so the financial track keeps pace with the physical one.

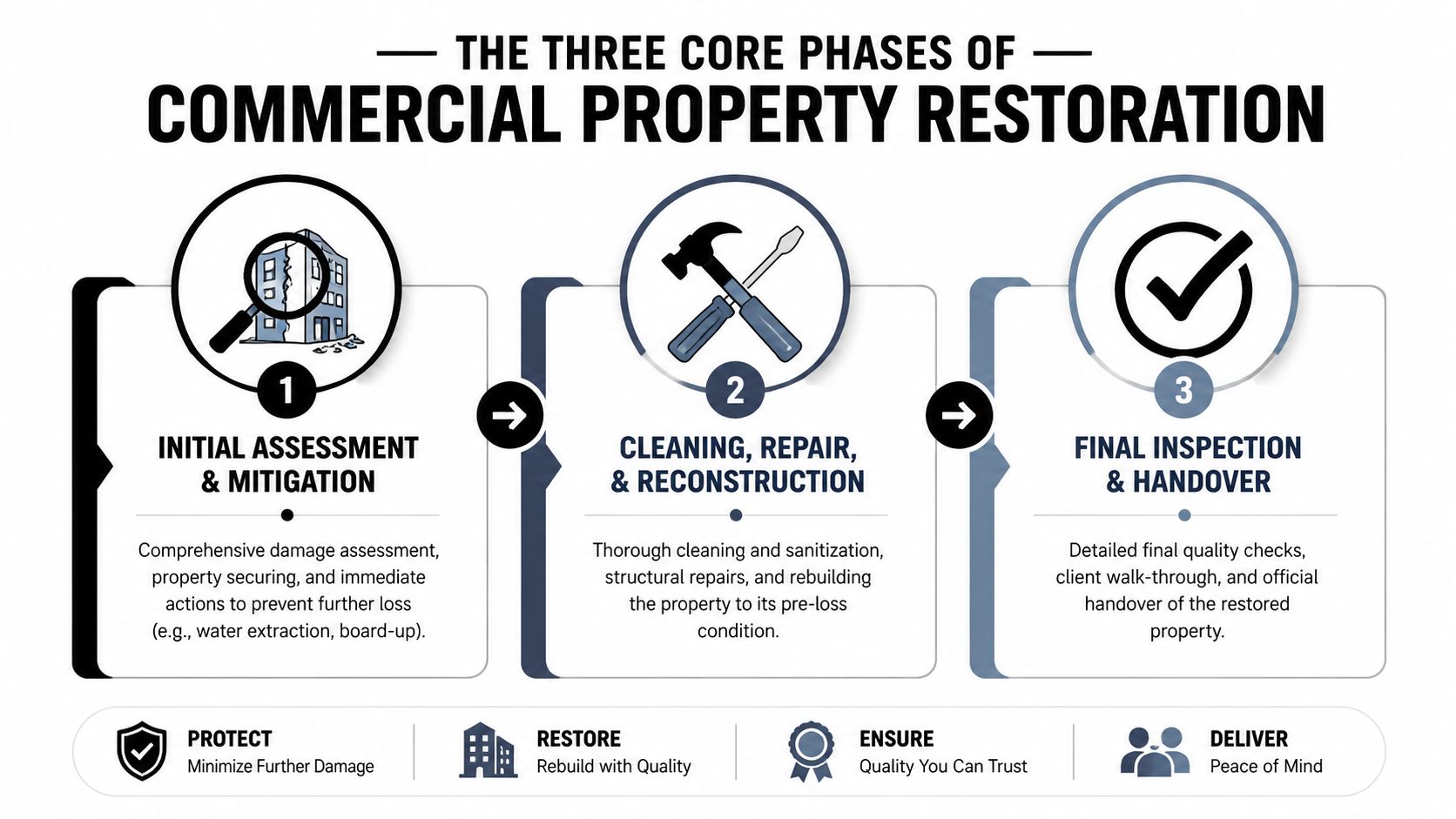

Understanding the Three Core Phases of Restoration

Commercial restoration follows a sequence, but it rarely feels neat while you're in it. In a commercial building, systems overlap. Water that starts in one suite can affect corridors, shared mechanicals, lower floors, and tenant property that you don't directly control.

Commercial properties are also harder to assess than homes. Large open floor plates, shared occupancies, HVAC, elevators, electrical panels, plumbing risers, and multi-floor layouts usually require containment and system isolation before demolition starts. Detailed documentation with moisture meters, thermal cameras, photos, and drying logs comes first, as described in this commercial restoration workflow overview.

Phase one is stabilization

This is the emergency window. The immediate goal is to stop conditions from getting worse.

During this phase, a competent contractor typically handles site protection, extraction, temporary board-up if needed, and containment. In a commercial setting, they should also decide quickly whether smoke or moisture entered the HVAC distribution path and whether affected zones need to be isolated.

What works here is speed with control. What doesn't work is tearing out materials before the damage is documented well enough to support the claim.

Phase two is cleaning, removal, and rebuild planning

This is usually the messiest part. Wet drywall, insulation, flooring, ceiling systems, and contaminated materials may need removal. Fire losses can involve soot cleaning, odor work, and surface-specific treatment. Sewage or biohazard conditions raise the standard even further.

A few trade-offs show up in this phase:

- Selective demolition vs aggressive tear-out: Too little removal leaves hidden damage behind. Too much removal can inflate cost and create disputes if the demolition wasn't necessary.

- Fast rebuild decisions vs accurate scoping: Owners want speed. But ordering finishes before hidden damage is understood can create change orders and delays.

- Occupied operations vs clean work zones: In multi-tenant buildings, keeping some areas open may preserve revenue, but only if containment is real and safe.

In commercial losses, the contractor's first good decision is often what not to demolish until the cause, spread, and system impacts are documented.

Phase three is contents and operational return

Contents restoration gets overlooked because the building itself takes center stage. That's a mistake. Servers, office furniture, retail inventory, kitchen equipment, files, teaching materials, and nonprofit program supplies can drive a large share of the disruption.

This phase often includes:

Triage of contents

Separate salvageable items from total losses. Don't rely on memory later.Cleaning and storage

Some items can be cleaned, dried, packed out, or stored off-site while the building work continues.Return-to-service planning

Reoccupancy isn't just moving things back in. It means the space is functional for staff, tenants, customers, or program delivery.

The owners who manage this phase best don't ask only, “When will repairs be done?” They ask, “When can this property operate normally again?”

What Determines the Cost and Timeline of Your Restoration

The two questions every owner asks first are the right ones. How much is this going to cost, and how long will we be down? The frustrating answer is that both depend on facts that often aren't clear on day one.

Some losses look straightforward and then expand once the contractor opens up walls, checks under flooring, or inspects mechanical systems. Others appear severe but dry cleanly with limited demolition. The actual timeline comes from the building systems involved, the contamination level, and whether the claim process keeps pace with the work.

According to this commercial damage restoration technology overview, the benchmark for time-sensitive commercial losses is rapid extraction within 24 to 48 hours, followed by a 3 to 5 day dry-out phase and 1 to 3 weeks for cleanup. Major structural rebuilds can take months.

What pushes a job toward the expensive end

A few variables matter more than owners expect.

- Type of loss: Clean water is different from smoke, sewage, or mixed contamination.

- Building complexity: A warehouse, medical office, school, and restaurant all restore differently.

- Hidden spread: Moisture behind millwork, under finished flooring, or inside shafts changes the scope.

- Material lead times: Custom storefront systems, specialty finishes, elevator work, and mechanical components can hold up reoccupancy.

- Stakeholder approvals: Tenants, lenders, landlords, and municipal requirements can delay the handoff even after repairs are physically complete.

Downtime often costs more than owners planned for

Business interruption is where many claims go sideways. Owners focus on repair invoices because they're obvious. Lost revenue, extra expense, reduced tenant use, and operational slowdown are harder to organize, so they get underdeveloped.

That's a problem because every lost operating day affects cash flow. In practice, the timeline on paper and the timeline in your bank account are not the same thing. A suite may be dry and still not be usable. A retail floor may reopen while sales remain impaired. An office may technically function while key departments stay displaced.

Field note: The fastest way to lose money on a commercial claim is to document the wet drywall and ignore the weeks of disrupted operations around it.

If you're comparing contractor estimates or insurer scopes built in Xactimate, some owners find it helpful to understand how those pricing frameworks are assembled and challenged through Verisk Xactimate training. That doesn't replace expert review, but it does help explain why two estimates can differ so sharply.

How to Manage the Commercial Property Insurance Claim

The claim process feels collaborative at first. Everyone inspects. Everyone asks questions. Everyone talks about getting the property back together. Then the differences in incentive become clear.

The insurer's adjuster works for the insurer. The restoration contractor works to perform restoration work. You, the owner, need the building repaired and the full loss paid correctly. Those goals overlap, but they are not identical.

The biggest bottleneck in many commercial losses isn't the cleanup itself. It's the insurance side. Delays in investigation, disputes over scope, and narrow valuation can produce more financial pain than the physical damage. That's why commercial restoration claim guidance increasingly emphasizes documentation, business interruption tracking, and scope verification.

Who's who in your commercial property claim

| Player | Who They Work For | Primary Goal |

|---|---|---|

| Property owner | The ownership entity, business, or nonprofit | Restore operations and recover the full covered loss |

| Insurer's adjuster | The insurance company | Evaluate the claim under the carrier's interpretation of coverage and scope |

| Restoration contractor | The party hired to mitigate and repair | Perform emergency work, drying, cleanup, and reconstruction |

| Public adjuster | The policyholder | Document, value, and negotiate the claim in the owner's interest |

That table matters because confusion here causes expensive mistakes. Owners often assume the insurer's adjuster is a neutral guide. They aren't. They may be professional and courteous, but they still represent the carrier.

What good claim management looks like

A well-managed commercial claim usually has these traits:

- Early policy review: Coverage issues are identified before major commitments are made.

- Scope control: The damage description matches what the building needs, not just what was visible on the first walk-through.

- Business interruption support: Revenue records, payroll effects, lease impacts, and extra expenses are gathered while events are current.

- Communication discipline: Key decisions are confirmed in writing, not left to hallway conversations or verbal assurances.

Owners should also separate contractor authority from claim authority. A contractor can explain what the property needs physically. That doesn't mean the contractor is the right party to frame every part of the insurance loss.

If the insurer controls the timeline, the inspection sequence, and the first draft of scope without meaningful pushback, the owner usually starts the negotiation from behind.

For a practical overview of the steps and friction points involved, review the property damage claim process before major documents are signed or large portions of the building are opened up.

Your Guide to Documentation and Contractor Selection

When a commercial loss hits, owners want action. That instinct is right, but rushed action without documentation creates claim damage that can last longer than the physical damage.

The goal is simple. Preserve evidence, track the loss in real time, and hire people who can perform commercial work without letting the claim drift off course.

Build the record before memory fades

Photos taken three weeks later are not as useful as photos taken the same day. A tenant's recollection after a stressful move-out is not as reliable as a dated written log. The record should start immediately and continue until operations normalize.

A strong documentation file often includes:

- Photos and video: Capture wide shots, room-level shots, equipment tags, damaged finishes, standing water, debris, and affected common areas.

- Cause and timeline notes: Record when the loss was discovered, who observed it, what emergency actions were taken, and when utilities or systems were shut down.

- Contents inventory: List damaged equipment, furniture, stock, files, and specialty items before they're discarded or packed out.

- Communication log: Track calls, emails, site meetings, and promises made by contractors, tenants, brokers, and insurer representatives.

- Expense file: Keep invoices, temporary protection costs, relocation expenses, cleanup charges, and any extra operating costs tied to the loss.

Choose the contractor like you're hiring for a dispute, not just a cleanup

The right contractor for a commercial property restoration loss isn't always the first crew on site. Emergency response matters, but so do documentation habits, commercial systems experience, and the ability to justify scope.

When vetting contractors, ask about:

Commercial project history

Multi-tenant offices, schools, kitchens, warehouses, and nonprofits each create different restoration problems.Documentation standards

Do they use moisture maps, drying logs, thermal imaging, and room-by-room records?Scope clarity

Can they explain why each demolition or cleaning step is necessary?Licensing, insurance, and trade coordination

Especially in Oregon and Washington, you want a contractor who understands regulated work and permit-sensitive repairs.

Insurer-preferred vendors can be perfectly capable. But don't accept any scope, price, or work authorization just because the referral came through the carrier. Independent review protects you.

If the loss involves roof failure or suspected water entry from above, a separate inspection can also help isolate cause and spread before repairs begin. In those situations, owners often look for qualified roof inspection contractors to support the file.

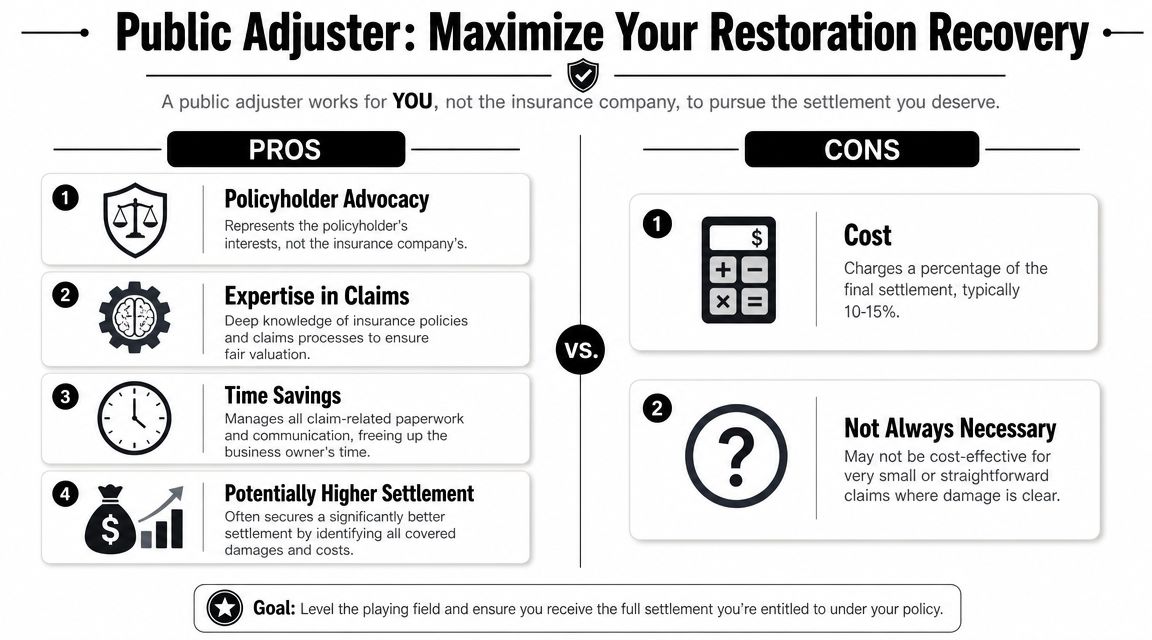

Maximizing Recovery with a Public Adjuster

At a certain point, owners have to decide whether they're going to personally run the claim while also running the property, the business, and the restoration. On a meaningful commercial loss, that's rarely an efficient use of time.

A public adjuster represents the policyholder, not the insurer. That changes the entire dynamic of the claim. Instead of reacting to the carrier's scope, the owner has someone building an independent valuation, interpreting the policy, organizing evidence, and negotiating from the owner's side of the table.

The U.S. damage restoration industry had over 60,000 businesses in 2025, and commercial property restoration represented 35% of the total market share, according to IBISWorld industry data. In a market that large, owners shouldn't assume the insurer's first numbers automatically capture the full value of a commercial loss.

What a public adjuster actually does

A good public adjuster doesn't just “check the estimate.” The work usually includes:

- Policy analysis: Review building, contents, extra expense, and business income provisions.

- Damage documentation: Organize site evidence, expert input, inventories, and repair support.

- Valuation: Prepare or challenge scopes, pricing, and loss calculations.

- Negotiation: Handle insurer communications and push disputed items toward resolution.

- Claim coordination: Keep the financial side aligned with what contractors, tenants, and stakeholders are experiencing on the ground.

In Oregon and Washington, licensing matters. Owners should work with properly licensed professionals because claim handling affects rights, deadlines, and settlement posture.

When hiring one makes practical sense

Not every claim needs a public adjuster. Small, clean, obvious losses may move without much dispute. Commercial claims often aren't like that. They involve layered coverages, incomplete early inspections, code questions, and operating losses that don't fit neatly on a contractor invoice.

For owners who want an example of what this service looks like in practice, NW Claims Management is one Oregon and Washington option that handles policy interpretation, loss documentation, and settlement negotiation on behalf of policyholders.

The best time to bring in claim help is before the file hardens around an incomplete scope.

Achieving a True Operational Recovery After a Loss

A commercial property restoration project is successful only when two things happen. The building is repaired, and the business side of the loss is settled in a way that allows normal operations to resume without lingering financial damage.

That's why “complete” restoration means more than new drywall, paint, and flooring. Current industry guidance on commercial recovery notes that a complete restoration in 2026 includes code-upgrade coordination, tenant management, HVAC contamination review, and the documentation needed for lenders or landlords. A building can be repaired and still remain functionally unusable if those issues are left unresolved, as outlined in this commercial services overview from Paul Davis.

What owners should confirm before calling the job done

Use a final-readiness mindset, not a cosmetic one.

- Operational clearance: Can staff, customers, tenants, or program users return and function normally?

- Stakeholder sign-off: Have landlord, lender, tenant, or board requirements been satisfied?

- System verification: Were HVAC, life-safety, access, and other building systems reviewed after the loss?

- Claim completeness: Have indirect losses, extra expenses, and unresolved scope items been addressed?

In Oregon and Washington, that final check matters even more for mixed-use properties, nonprofits, schools, and occupied commercial sites where multiple parties depend on the same building performing as promised.

If the loss affected building access points, loading areas, or overhead doors, practical post-loss safety checks matter too. For example, this resource on spotting emergency door problems is worth reviewing when a damaged entry system could delay secure reoccupancy.

The goal isn't just to reopen. It's to reopen with the building, the paperwork, and the claim aligned.

If you're facing a commercial loss in Oregon or Washington, NW Claims Management can review the claim, identify gaps in scope or documentation, and help you pursue a fair settlement that supports both restoration and business recovery.