You walk into the living room and see water stains spreading across the ceiling. Or you pull into the driveway after a windstorm and find shingles in the yard, flashing peeled back, and a tarp already on your neighbor’s roof. At that point, most property owners in Oregon and Washington aren’t thinking about legal terminology. They’re thinking about safety, cleanup, and whether the insurance company is going to do the right thing.

That’s where a claim of damages becomes real. It’s the formal demand for the money needed to repair, replace, restore, and account for the loss tied to the event that hit your property. If you own a home, a rental, a business, a church, a school, or a nonprofit facility, the claim is not just paperwork. It’s the record that decides what gets paid and what gets left on you.

The problem is that many policyholders start the process as if it were a simple reimbursement request. It isn’t. It’s a proof exercise. You need to show what happened, why the damage is tied to that event, and what the loss is worth under the policy and, in some situations, under the law.

What Is a Claim of Damages

A claim of damages starts the moment you realize the loss is bigger than a quick patch or a cleanup bill. You may have smoke damage after a kitchen fire, wind-driven rain inside the walls, or vandalism that shuts down part of your building. The insurer opens a claim file, but your job is different from theirs. Their adjuster is evaluating exposure. You’re trying to prove the full value of the loss.

A practical way to think about it is this. A claim of damages is your documented case for being made whole after a covered loss. In insurance, that usually means showing the insurer what it owes under the policy. In a legal dispute, it can mean proving what a negligent party or a bad-faith insurer should pay.

In 2024, the average jury verdict for plaintiffs in federal lawsuits reached $16.2 million, nearly quadrupling from 2019, according to this analysis of rising federal lawsuit damages. That trend is often described as social inflation. For property owners, the takeaway isn’t that every claim turns into a lawsuit. It’s that damage disputes now carry serious financial consequences, which makes careful documentation and negotiation more important than ever.

What policyholders often miss

Many first-time claimants focus only on visible repairs. They gather a contractor quote for drywall, roofing, or flooring and assume that’s enough. It usually isn’t.

A strong claim of damages may also include:

- Hidden physical damage like wet insulation, smoke migration, structural movement, or code-triggered work

- Use-related losses such as lost rent, extra expense, temporary relocation costs, or interrupted operations

- Value-based losses when repair alone doesn’t fully restore what was lost

- Support for causation showing the damage came from the covered event and not wear, deferred maintenance, or a pre-existing issue

Practical rule: If a loss isn’t documented, insurers often treat it as if it doesn’t exist.

That’s why the first days matter. Photos, moisture readings, contractor findings, invoices, inventory, and timeline notes all become part of the claim. If you need a clear overview of what happens from notice through settlement, this guide to the property damage claim process lays out the sequence in plain terms.

What works and what doesn’t

What works is a disciplined file. Date-stamped photos. Room-by-room notes. A repair scope tied to the actual damage. Estimates that address code requirements, access issues, matching, and debris handling.

What doesn’t work is handing in a rough number and hoping the insurer fills in the gaps for you. Most carriers won’t build your claim for you. They’ll respond to the claim you present.

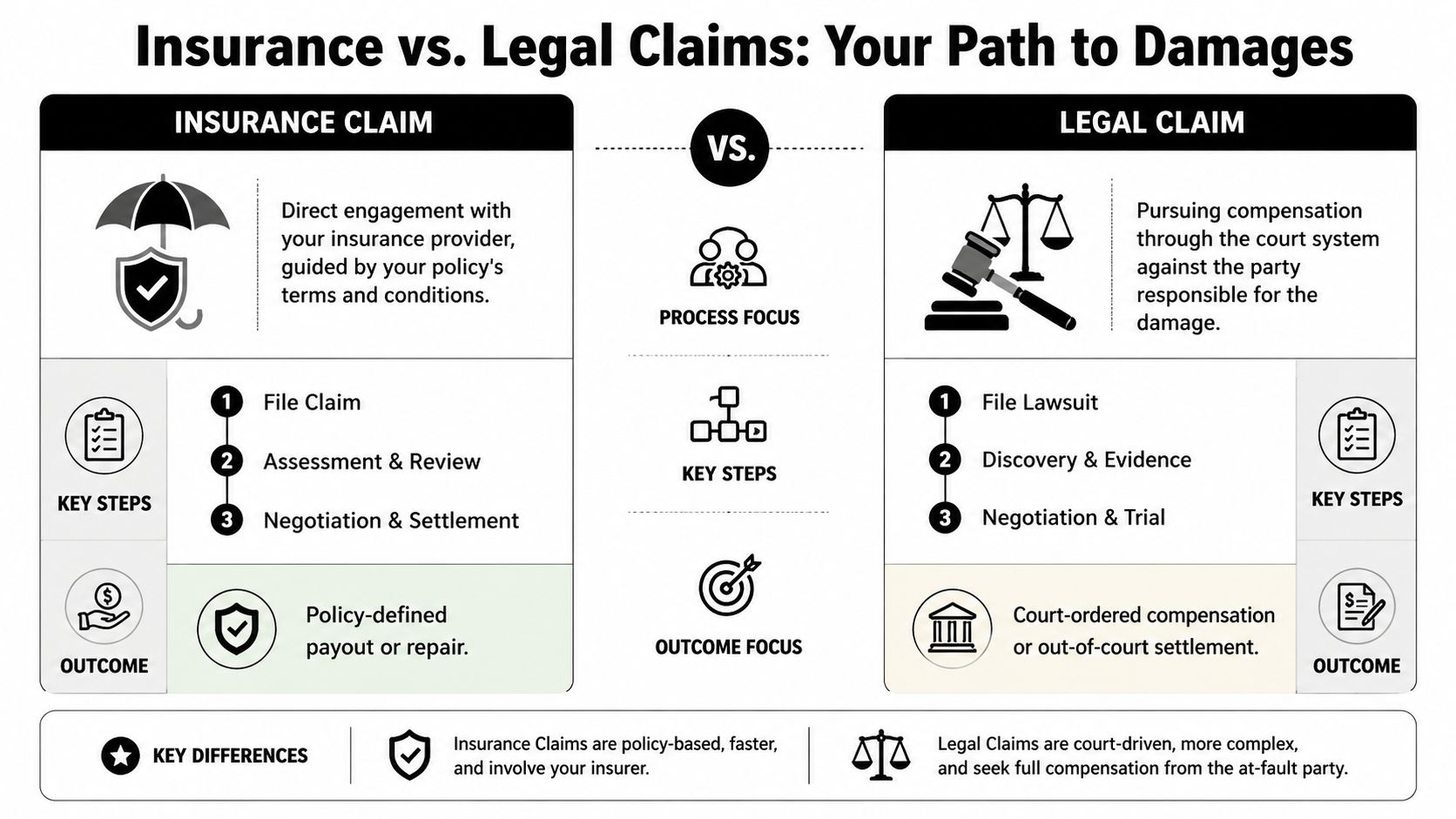

Insurance Claims and Legal Claims Explained

People often use the phrase claim of damages as if it means one thing. In practice, there are two very different paths.

An insurance claim is a contract claim. You paid premiums, the policy sets the rules, and you’re asking the carrier to perform under that contract after a covered loss.

A legal claim is different. You’re alleging that another party caused the damage or handled your claim improperly, and you’re seeking compensation through the legal system.

The simplest way to separate them

Think of an insurance claim as enforcing a promise already written down. The key questions are whether the loss is covered, what conditions apply, and how the amount should be valued.

A legal claim asks a different set of questions. Who caused the damage. Was there negligence or wrongful conduct. What losses flowed from that conduct.

Here’s the side-by-side difference:

| Path | What it’s based on | Who you pursue | Typical focus |

|---|---|---|---|

| Insurance claim | Your policy contract | Your insurance carrier | Coverage, valuation, compliance with policy conditions |

| Legal claim | Tort, statutory rights, or bad faith | Negligent third party or insurer | Fault, causation, broader damages, legal remedies |

Where these paths overlap

Sometimes both paths are in play. A windstorm tears off roofing because a contractor installed flashing badly. You may have an insurance claim under your property policy and a separate legal claim against the contractor. The insurer may later pursue that contractor through subrogation.

Other times the issue is the insurer’s own conduct. If the carrier underpays, delays unreasonably, or mishandles the claim, the dispute can move beyond a policy adjustment problem into a legal one. As noted in the earlier discussion of rising damages, some bad-faith cases have produced very large verdicts, which shows how different the outcome can be once the dispute leaves the ordinary claims track.

Why this distinction matters in Oregon and Washington

Most policyholders should begin by treating the matter as a disciplined insurance claim, because that’s usually the fastest route to restoring the property. But you also need to know when the issue has shifted.

You may be dealing with a contract problem when:

- Coverage is acknowledged but the scope is too small

- Pricing is low because labor, code work, or line items were omitted

- Depreciation is applied more aggressively than the policy supports

You may need legal review when:

- Liability is denied outright on grounds that don’t match the facts

- The insurer leans on technical policy language to avoid a fair evaluation

- The claim handling itself becomes the problem

A policy claim asks, “What does the contract owe?” A legal claim asks, “Who is responsible for the harm, and what remedies are available?”

If you want a useful outside example of how storm losses move through the insurance side before they ever become legal disputes, this overview of a Texas storm damage insurance claim shows a process many Northwest property owners will recognize, even though the state and policy details differ.

When policyholders are unsure who is protecting whose interests, it helps to understand the difference between your representative and the carrier’s representative. This breakdown of a public adjuster vs insurance adjuster is worth reading before major inspections or settlement talks.

Key Elements and Types of Recoverable Damages

A successful claim of damages usually stands on three legs. Remove one, and the file gets weak fast.

First, you need proof of a covered event. That might be wind, fire, water from a sudden plumbing failure, vandalism, or another insured peril. Second, you need causation. You must connect the event to the damage you’re claiming. Third, you need valuation. You have to show what it costs to repair, replace, or otherwise compensate for the loss.

The three elements that carry the claim

Start with the event itself. Carriers look for dates, weather records, fire reports, mitigation invoices, emergency service notes, and inspection findings. If the date of loss is fuzzy or the event description keeps changing, the claim gets harder to defend.

Causation is where many disputes begin. A roof may have storm damage, old repairs, brittle shingles, and long-term wear all at once. You don’t win that argument with opinions alone. You win it with inspection detail, photographs, testing, and consistent reporting from qualified professionals.

Valuation is the final step, but it shouldn’t be an afterthought. Pricing has to match the actual scope. If the estimate leaves out detach-and-reset work, code items, interior access, specialty finishes, or business-related loss components, the insurer may anchor the whole claim too low from the start.

What damages may be recoverable

Recoverable damages depend on the policy, the facts, and sometimes state law. In property claims, these categories often matter:

- Building damage involving structural repair, finish restoration, debris removal, and related work

- Personal property or contents such as furniture, equipment, supplies, electronics, inventory, or donated goods

- Loss of use including temporary living expenses or relocation costs when the property can’t be used as intended

- Business interruption or extra expense for commercial owners, schools, churches, and nonprofits that suffer operating disruption

- Loss tied to reduced value when repair doesn’t fully erase the market impact of the damage history

That last category is where many property owners leave money on the table.

Stigma damages in Oregon and Washington

A commonly missed part of a claim of damages is stigma damages, meaning the drop in market value that can remain after the physical repairs are done. The verified data here is significant. Post-disaster properties may suffer a 10 to 30 percent reduction in market value, and the same source notes that 40 percent of Oregon wildfire victims received 20 percent less than expected due to unclaimed stigma, according to this discussion of property loss damage measures.

Oregon and Washington don’t treat this issue identically. Oregon courts are shaped by the economic waste doctrine, while Washington may allow diminution-related recovery in a different way. The practical point is that “we repaired it” doesn’t always end the damages analysis.

If your property has a documented fire, flood, or major water history, ask whether repair cost alone fully addresses the loss in value. Don’t assume the insurer will raise that issue for you.

Policyholders also need to know where the policy ceiling is. A good claim can still run into sublimits, valuation clauses, or category-specific caps. This guide to insurance policy limits explained helps frame that part of the discussion before negotiations harden.

How to Value and Document Your Damage Claim

Documentation wins more claims than emotion does. That doesn’t mean emotion isn’t real. It means the insurer pays from the file. If the file is thin, disorganized, or inconsistent, even a legitimate loss can be underpaid.

The first step is to document the property as it sits before cleanup changes the evidence. Take wide photos, close photos, and video that shows how one damaged area connects to another. If the loss affects multiple rooms or systems, move methodically and label everything.

Build the claim like a project file

A property claim is easier to defend when you organize it by category rather than dumping everything into one email chain. Separate emergency mitigation from permanent repairs. Separate building damage from contents. Separate lost income from ordinary repair invoices.

This checklist helps:

| Category | Evidence to Collect | Why It's Important |

|---|---|---|

| Building damage | Date-stamped photos, videos, contractor scopes, mitigation records, inspection notes | Shows extent of damage and ties repair work to the event |

| Contents | Itemized inventory, photos, receipts, replacement quotes | Supports ownership, condition, and value |

| Cause of loss | Weather records, fire reports, plumbing reports, expert findings | Connects claimed damage to the covered event |

| Temporary repairs | Tarping invoices, dry-out bills, emergency labor receipts | Proves mitigation efforts and immediate out-of-pocket costs |

| Additional living expense or extra expense | Hotel bills, rent, meal records, relocation receipts, substitute equipment costs | Supports reimbursement for displacement or operational disruption |

| Business interruption | Financial statements, sales records, payroll data, scheduling records, cancellation logs | Helps measure income loss and ongoing expenses |

| Communications | Emails, claim letters, adjuster notes, inspection schedules | Creates a timeline and captures positions taken by the insurer |

Know the difference between RCV and ACV

Many settlement disputes start because the policyholder and the carrier are talking about two different valuation methods.

Replacement Cost Value (RCV) generally refers to the cost to repair or replace with like kind and quality, subject to the policy terms. Actual Cash Value (ACV) usually reflects depreciation. On older roofs, interiors, flooring, or equipment, that distinction can materially change what gets paid up front and what may be recoverable later after repairs are completed.

That’s why estimate review matters. Xactimate line items, depreciation schedules, matching issues, and code requirements all affect whether the number on paper is realistic or artificially low.

Use causation modeling for complex losses

For business owners, schools, nonprofits, and larger commercial properties, a claim of damages often extends beyond visible repairs. You may need to prove what operations would have looked like if the loss had not happened.

Damages experts use causation modeling by comparing the actual post-loss world with a but-for scenario. The verified data states that flawed assumptions in these models can reduce awards by 30 to 50 percent, according to this discussion of expert witness damages analysis. In practical terms, that means a weak income-loss model can shave a valid claim down because the assumptions were sloppy.

Examples of strong support include:

- Historical financials that show seasonal patterns before the loss

- Vendor and payroll records that prove ongoing expense pressure

- Enrollment, occupancy, or program records for schools and nonprofits

- Repair timelines that connect downtime to actual restoration constraints

Don’t just say the loss disrupted your operations. Show what normal looked like before the event, what changed after it, and why the difference is tied to the damage.

If the claim is large or technically disputed, professional help may be warranted. One option is a public adjuster. Another may be a contractor with strong estimating support, a forensic accountant for interruption loss, or an engineer for cause disputes. For Oregon and Washington property owners who need help assembling scope, pricing, and evidence, property damage assessment support can clarify what belongs in the claim before numbers get locked in.

Filing Procedures and Deadlines in Oregon and Washington

The most expensive mistake in a claim of damages can be a calendar mistake. Good evidence won’t save a claim that was filed late or a lawsuit brought after the legal deadline expired.

The first deadline is usually inside your policy, not in the courthouse. Most property policies require prompt notice of the loss. Many also require cooperation, documentation, inspection access, and, in some cases, a Sworn Statement in Proof of Loss within the timeframe stated by the policy or requested by the carrier. The exact wording matters. Don’t assume your deadline matches someone else’s policy.

What to do early

Once the loss happens, move on these items quickly:

- Give notice to the carrier as soon as you can and keep proof that you did

- Request a complete copy of the policy if you don’t already have it

- Ask in writing whether the insurer requires a proof of loss and by when

- Track every inspection and request in a dated claim log

- Preserve damaged materials when possible until the carrier has had a fair chance to inspect

Lawsuit timing is a separate issue

A legal claim for property damage has a different timeline from an insurance reporting obligation. In Oregon and Washington, the exact deadline depends on the type of claim, the parties involved, and whether you’re dealing with contract issues, tort issues, or both. That’s why policyholders shouldn’t rely on generic advice from friends, contractors, or online forums.

For readers trying to understand how Oregon limitation periods work on the injury side, this resource to understand Oregon injury claim time limits is useful context because it shows how unforgiving legal deadlines can be. Property cases involve different rules, but the lesson is the same. Once the clock runs, the advantage is lost.

The practical trade-off

Some owners wait because they don’t want to “escalate” the claim. That instinct is understandable, but delay can create new problems. Witness memories fade. Emergency repairs remove evidence. Rot, corrosion, and mold complicate causation. The insurer may later argue it lost the chance to inspect the original condition.

The safest approach is to act early, document steadily, and get the deadlines in writing. Verbal assurances don’t preserve rights.

If the claim is already dragging, ask for the carrier’s position in writing. A stalled file is easier to evaluate when the disputes are pinned down on paper.

Common Insurer Tactics and Effective Counter-Strategies

Most claim denials don’t arrive with a note that says, “We’re trying to narrow your recovery.” They come in the form of estimate omissions, causation disputes, depreciation arguments, repeated document requests, and technical readings of policy language.

That’s why it helps to treat claim handling like a negotiation with patterns. Once you can identify the tactic, you can answer it more effectively.

Tactic one and how to answer it

A common move is the incomplete estimate. The carrier’s scope may price the obvious repairs but leave out access costs, code items, painting continuity, overhead and profit, specialty materials, or the work needed to reach hidden damage.

The answer is not outrage. It’s a line-by-line rebuttal backed by photos, contractor scopes, building requirements, and a revised estimate built on the actual conditions.

Another common move is the documentation spiral. The insurer keeps asking for more records, but the requests stay broad and unfocused. Sometimes that’s legitimate. Sometimes it’s a way to slow the claim and wear the policyholder down.

Use a written response strategy:

- Ask for specificity about what is needed and why

- Respond in organized batches instead of piecemeal fragments

- Note what has already been provided with dates

- Request confirmation when the insurer has enough to move forward on a decision

Technical denial language around older property

Aging roofs and older building components trigger some of the hardest fights. Insurers often invoke the efficient proximate cause rule, arguing that wear, age, or another non-covered condition contributed to the loss. In Washington, verified data notes that recent rulings clarify the covered peril must be the dominant cause, and that for aging roofs, post-storm denial rates can reach 35 percent, while represented policyholders often recover over 50 percent more by successfully disputing these issues, according to this discussion of the efficient proximate cause rule.

That matters because many legitimate storm claims involve roofs that were not brand new. Age alone doesn’t erase coverage if a covered event caused the actionable damage.

Counter-strategies that actually help

What works against technical denials is disciplined proof:

- Separate condition from cause by documenting pre-loss age versus post-event damage pattern

- Use qualified inspections when the insurer claims the issue is only wear or maintenance

- Address matching and repairability instead of accepting a patch proposal too quickly

- Push for written coverage positions tied to specific policy language and actual facts

A denial based on mixed causes isn’t the end of the claim. It’s the point where the facts, the policy wording, and the quality of your evidence start to matter most.

For many owners, professional representation makes a difference in the file. A public adjuster can assemble scope, challenge omissions, and respond to policy-based minimization arguments. NW Claims Management provides that kind of representation for Oregon and Washington policyholders, including file review, loss documentation, and settlement negotiation. If you want to spot the patterns before they cost you money, this guide to common insurance adjuster tricks is a practical place to start.

Frequently Asked Questions About Your Claim

Should I handle the claim myself or hire help

Smaller, clean losses can sometimes be handled directly if coverage is clear, damage is limited, and the carrier’s scope is complete. Larger losses usually become harder once there are hidden damages, code issues, multiple buildings, interruption losses, or disputes about cause.

If you’re spending your nights chasing contractors, decoding policy language, and reworking estimates, the claim may have outgrown a do-it-yourself approach.

What does a public adjuster actually do

A public adjuster works for the policyholder, not the insurer. The job is to inspect the loss, review the policy, document damages, assemble the claim, value the scope, and negotiate with the carrier. In Oregon and Washington, that role matters most when the file is technical, underpaid, delayed, or denied for reasons that need a detailed response.

When is the right time to bring one in

Early is usually better than late, especially before the insurer’s first number becomes the anchor for the whole conversation. That said, a denied or underpaid claim can still be reviewed. The key is whether the missing evidence can still be gathered and whether deadlines remain open.

What should I say when I disagree with the insurer

Keep it direct and professional. Don’t rant. Don’t guess. Tie your position to facts and policy language.

A simple demand paragraph can look like this:

“I disagree with the current valuation of my claim. The estimate does not include all damaged areas and necessary repair items related to the reported loss. Please re-evaluate the claim based on the enclosed photographs, contractor scope, invoices, and supporting documentation, and provide your written coverage and valuation position with reference to the applicable policy provisions.”

That kind of language keeps the issue focused. It also creates a record.

Can I recover for damage to an older roof or older building materials

Yes, sometimes. Older materials create valuation and causation fights, but age does not automatically defeat a claim. The key issue is whether the covered event caused direct physical loss and what the policy says about depreciation, actual cash value, replacement cost, matching, and repairability.

What if repairs are finished but the property still lost value

That’s where diminution and stigma issues may need to be evaluated. If the property’s damage history affects marketability even after repairs, repair cost alone may not tell the whole story. This comes up more often after major fire, flood, or wildfire losses than most owners realize.

If your property claim in Oregon or Washington feels larger, slower, or more disputed than it should, NW Claims Management can review the loss, explain where the claim stands, and help you understand what support belongs in your claim of damages before you accept an underpaid outcome.