Think of an auto insurance appraisal as your secret weapon after an accident. It's a professional, detailed valuation that proves what your car was really worth right before it was damaged. This becomes incredibly important when an insurer calls your car a total loss and makes a settlement offer that just doesn’t feel right.

What Is an Auto Insurance Appraisal and Why It Matters

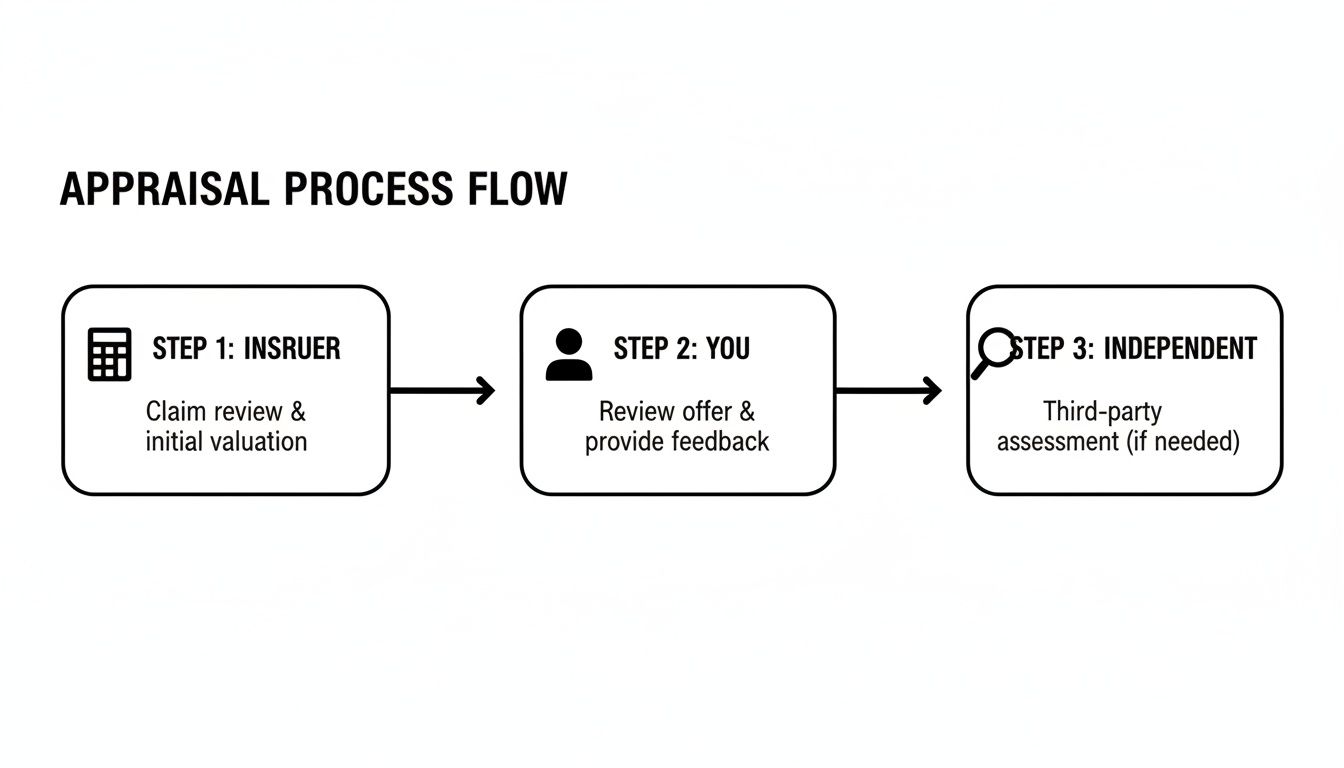

When your car is badly damaged, your insurance company will perform its own valuation to figure out its Actual Cash Value (ACV). This is the magic number they say your car was worth moments before the crash. If fixing the car costs more than a certain percentage of that ACV, they’ll declare it a "total loss" and offer you a check.

But here’s the thing: that first offer isn't a final, take-it-or-leave-it number. It’s a starting point for a negotiation. Understanding the power of an auto insurance appraisal is how you gain the upper hand in that negotiation.

Why You Need to Know Your Car’s True Worth

Most insurers use automated software to spit out a value. It's fast and easy for them, but these systems often miss the very things that made your car special and more valuable.

An independent appraiser, on the other hand, digs into the details that software overlooks, such as:

- Recent Upgrades: Did you just put on a brand-new set of tires or upgrade the stereo system?

- Exceptional Condition: Was your car a garage-kept gem with super low mileage for its age?

- Local Market Demand: Is your specific make and model a hot commodity in your area, commanding a higher price?

A generic report from an insurance company almost always misses these nuances. An independent appraisal, done by an expert you hire, focuses on building a case for a higher, more accurate value. For a deeper dive, check out this comprehensive guide to auto insurance appraisals.

To get comfortable with the appraisal process, it helps to know the terminology. These are the key concepts you’ll hear thrown around.

Key Appraisal Concepts at a Glance

This table breaks down essential terms you'll encounter during the auto insurance appraisal process, helping you understand the language used by insurers and adjusters.

| Term | What It Means for You |

|---|---|

| Actual Cash Value (ACV) | This is the insurer's estimated value of your car right before the loss. It's their starting offer and the number you'll be negotiating. |

| Total Loss | When repair costs exceed a certain percentage of the ACV (often 70-80%), the insurer decides it's not worth fixing and will pay you the ACV instead. |

| Independent Appraiser | A qualified, unbiased expert you hire to determine your vehicle's fair market value, separate from the insurance company's assessment. |

| Appraisal Clause | A provision in your policy that allows you and the insurer to resolve valuation disputes using appraisers and a neutral umpire. |

Knowing these terms empowers you to navigate the claims process with confidence and hold your ground during negotiations.

Appraisals in a Rising Total Loss Market

The need for a solid, independent appraisal is more critical now than ever. Recent industry data is eye-opening: as of April 2025, a staggering 22.6% of collision claims resulted in a total loss. This trend, highlighted in the CCC Crash Course report, is partly because vehicle values have dipped, making it easier for repair estimates to cross that total loss threshold.

An insurer's valuation is their opinion of what they owe you. An independent appraisal is a fact-based argument for what your vehicle was actually worth.

This difference is everything. The insurance company's job is to close the claim efficiently and manage costs. Your goal is to be fully compensated for your loss. Unfortunately, adjusters sometimes use specific tactics to keep settlement amounts down. Knowing what to watch for is half the battle; our guide on common insurance adjuster tricks can help you prepare.

Ultimately, the appraisal process gives you a structured, evidence-backed way to challenge a lowball offer and get the fair settlement you deserve.

Insurer Appraisals vs. Independent Appraisals

When your car is declared a total loss, the first thing you'll receive is a settlement offer from your insurance company. This number isn't pulled out of thin air; it’s their official valuation of your vehicle. But it's important to see this for what it is: an opening offer.

Let's be frank—there's an inherent conflict of interest at play. The insurer's goal is to close claims as efficiently and cost-effectively as possible. This creates a natural incentive to lean towards lower valuations. It's like letting the person who has to pay for the car also be the one who sets the final price.

The Insurer's Approach

Insurance carriers are all about volume and speed. To handle thousands of claims, they rely on standardized valuation software to generate an Actual Cash Value (ACV). While efficient, this software has some serious blind spots.

These automated systems often miss the very things that made your car valuable:

- Exceptional Condition: Was your car garage-kept with low mileage and a pristine interior? A database can't truly appreciate that.

- Recent Investments: What about the brand-new tires you just put on? Or the upgraded sound system? These are real dollars you spent that add to the car's value.

- Local Market Scarcity: Is your specific model and trim package a hot commodity in your area? That local demand absolutely drives up the real-world market price.

Because of these gaps, the insurer’s first offer is just their opinion of your car's value. It’s a starting point for a negotiation, not the final word.

The Power of an Independent Appraisal

This is precisely where an independent appraisal can completely change the game. An independent appraisal is a detailed, evidence-backed report crafted by an unbiased professional who works for you. Their only job is to determine your vehicle’s true, fair market value.

A qualified independent appraiser does the real legwork the software can't. They'll dig into local comparable sales, factor in your car's specific condition and maintenance history, and account for every aftermarket part and recent upgrade. This thorough, manual process frequently uncovers thousands of dollars in value the insurer's report completely missed.

An independent auto insurance appraisal acts as a powerful reality check. It replaces the insurer’s potentially biased opinion with a fact-based, market-driven valuation and gives you the leverage you need to contest a low offer.

Bringing in your own appraiser is a lot like hiring a public adjuster for a major home insurance claim. You're enlisting an expert to advocate for your financial interests against the insurance company's initial assessment. To see how this works in property claims, you can learn more about the crucial differences between a public adjuster and an insurance adjuster in our detailed guide. An independent appraisal is your first and most important step toward getting paid what you're rightfully owed.

How to Use the Appraisal Clause in Your Policy

So, you've sent in your research, you've argued your case, and the insurance company still won't budge on their lowball offer for your totaled car. When you’ve hit a wall with the adjuster, it’s time to pull out the big guns.

Buried in the dense language of your auto policy is a powerful provision called the Appraisal Clause. This isn't just a friendly suggestion; it's a contractual right you have to formally challenge the insurance company's valuation.

Think of it as your legal lever. Invoking this clause officially moves the dispute out of the informal back-and-forth with the adjuster and into a structured, binding resolution process designed to determine a final, fair value.

This process takes the negotiation away from the adjuster and puts it into a more defined system. Here’s a look at how it generally unfolds:

The key takeaway here is that you're no longer just reacting to the insurer’s low number. You’re taking control and evening the odds by bringing your own expert into the ring.

Kicking Off the Appraisal Process

You can't just tell your adjuster over the phone that you want to start the appraisal process. To make it official and protect your rights, you have to put it in writing. This creates the paper trail you need.

Getting the ball rolling is a pretty direct process:

- Send a Written Demand: You’ll need to draft a formal letter or email to your insurance company. In it, clearly state that you are exercising your right to appraisal under the terms of your policy to settle the dispute over your vehicle's Actual Cash Value.

- Name Your Appraiser: Your letter should also name the independent appraiser you've hired to represent you. This signals that you're serious and ready to proceed immediately.

- Wait for Their Move: Once your demand is received, your insurer is contractually required to hire their own appraiser.

This simple act forces the insurance company’s hand. They can no longer just delay or deny; they must participate in the resolution process outlined in the very policy they wrote. It completely changes the power dynamic.

How the Tie-Breaker Works

The appraisal process is built to find a resolution. Once both you and the insurer have your appraisers, the two of them will get to work. Their first job is to review all the evidence and try to negotiate an agreed-upon value for your car. If they can come to an agreement, that’s it—that figure becomes the binding amount of the settlement.

Your policy's appraisal clause is the built-in fairness mechanism. It ensures a dispute over value isn't decided by the company on the hook for the check, but by impartial experts.

But what happens if they can’t see eye to eye? That’s where the umpire steps in. If the two appraisers are at a stalemate, they will together select a neutral, qualified umpire to act as a tie-breaker.

Each appraiser will then present their case to the umpire. The final, binding settlement amount is locked in when any two of the three parties sign off on a value. This could be your appraiser and the umpire, or the insurer's appraiser and the umpire. Either way, the decision is final.

Your Step-by-Step Guide to Contesting a Low Offer

Getting that low settlement offer for your totaled car is a gut punch. It’s frustrating, but it’s definitely not the end of the road. In reality, it’s just the start of a negotiation.

Don't ever feel intimidated by that first number. Think of it as the insurance company's opening bid, not the final word. With a solid strategy, you can push back effectively and build a compelling case for what your vehicle was actually worth.

1. Demand the Valuation Report

First things first: you need to formally request a complete copy of the insurer's valuation report. This is the document—the "proof"—they used to calculate their offer, and you have every right to see it.

This report is your playbook. It will break down the comparable vehicles they used, the condition rating they slapped on your car, and every adjustment they made. It’s where you’ll find the weak spots in their argument.

2. Scrutinize the Report for Errors

With their report in hand, it's time to go through it with a fine-tooth comb. Most of these reports, typically outsourced to third-party companies, are riddled with inaccuracies that can drag down your car's value.

Look for these common mistakes:

- Wrong Trim or Package: This is a big one. Did they value your top-tier "Limited" or "Touring" model as a stripped-down base model? That's thousands of dollars right there.

- Missing Options and Features: They often miss things. Check if they accounted for that sunroof, the premium audio system, a factory tow package, or advanced safety features you paid for.

- Unfair Condition Rating: If you meticulously maintained your vehicle and they labeled it "average" or "fair" without any justification, that’s a major point of contention.

- Bad "Comps": Take a hard look at the "comparable" vehicles they used. Are they truly similar? Are they from your local market, or did they pull them from another state where prices are lower?

Finding these errors is the cornerstone of your counter-offer. Every mistake you uncover is an opportunity to add value back to your settlement.

A low offer isn’t just about the final number; it's about the flawed data used to calculate it. By correcting those flaws with your own evidence, you force the adjuster to defend an indefensible position.

3. Build Your Evidence-Based Counter-Offer

Now you get to fight back with facts. Start building a file with your own documentation that proves the higher, true value of your vehicle.

Gather everything you can find that tells your car's story:

- Service Records: A thick stack of maintenance receipts shows a well-cared-for vehicle.

- Receipts for Recent Work: Did you just put on 4 new tires, replace the battery, or get a brake job done? Prove it.

- Your Own Comparable Listings: Find online listings for the exact same year, make, model, and trim with similar mileage from sellers in your immediate area. Print them out.

Using this evidence, you can draft a detailed counter-offer. You're not just pulling a number out of thin air; you're presenting a logical, evidence-based argument that the adjuster can’t just dismiss. This methodical approach is a huge part of successfully negotiating with an insurance company and signals that you’re serious.

It’s especially important to be prepared. The global auto insurance market is projected to swell from USD 940.4 billion in 2025 to over USD 1.2 trillion by 2035. As costs rise, insurers are under immense pressure to control payouts. A well-documented counter-offer is your best tool to ensure you get a fair deal in this environment.

Costs and Timelines for Oregon and Washington

So, you've decided to challenge your insurance company's lowball offer. That's a big step, and it's smart to know what to expect in terms of both time and money. While invoking your policy's appraisal clause isn't free, understanding the process for Oregon and Washington gives you a real strategic advantage.

First things first: you'll need to hire a qualified, independent appraiser. It's easy to see this as just another expense, but I always tell clients to think of it as an investment in getting a fair payout. A good appraiser might cost a few hundred dollars, but that fee is often tiny compared to the thousands of extra dollars they can help you recover.

What Is a Realistic Timeline?

When it comes to an auto insurance appraisal, you'll need to have some patience. This isn't an overnight fix. From the day you formally demand an appraisal to the day you have a check in hand, the process usually takes anywhere from several weeks to a few months.

A few things can stretch out that timeline:

- The complexity of your car's damage or valuation.

- How quickly (or slowly) the insurance company and their appraiser respond.

- Whether the two appraisers hit a roadblock and need to bring in a neutral umpire.

Specifics for Oregon and Washington

If you live in the Pacific Northwest, you're in a good position. Both the Oregon Insurance Division and the Washington Office of the Insurance Commissioner have strong consumer protection rules that keep insurers in check. Knowing these local regulations can make a huge difference, especially when it comes to repair costs.

Insurers often try to cut their costs by insisting on cheaper components. To build a strong case, you should get familiar with the difference between OEM and aftermarket parts so you can argue effectively for what your vehicle truly needs.

The total cost of hiring your own expert, including potential umpire fees, is often a fraction of the value an independent appraisal can recover. Our guide on understanding public adjuster costs provides more context on this type of investment.

Don't forget the big picture: market trends show that while some parts of the insurance industry are stabilizing, we've all seen massive premium hikes lately. This is driven partly by a 3.7% jump in vehicle repair costs just this year. In this kind of environment, an accurate, independent appraisal isn't just a good idea—it's essential. For more on this, you can check out the latest 2025 insurance market trends on S&P Global.

When to Hire a Public Adjuster for Your Dispute

Sometimes, a lowball offer on your car's value isn't just a simple disagreement. It's a symptom of a much bigger problem with how the insurance company is handling your entire claim. An independent appraiser is the perfect expert for nailing down the correct Actual Cash Value (ACV), but what happens when the dispute goes far beyond that single number?

That’s when you might need to bring in a public adjuster. Think of it like this: an appraiser is a specialist focused on one critical task—getting the vehicle's price right. A public adjuster, on the other hand, is the project manager for your entire claim, overseeing the strategy, negotiations, and final settlement from start to finish.

Signs You Need More Than an Appraiser

A public adjuster becomes crucial when the fight isn't just about money, but about the insurer's conduct. If you run into any of these red flags, it's a strong signal that you need a licensed professional in your corner:

- Significant Delays: The adjuster is constantly "losing" your paperwork, goes silent for weeks, or simply won't return your calls and emails. You're getting the classic runaround.

- Bad Faith Tactics: You get the feeling the insurer is being dishonest, twisting the facts, or misrepresenting what your policy actually covers. They might be using pressure tactics to get you to accept a low offer out of sheer frustration.

- Complex or High-Value Claims: Your claim is a tangled mess involving multiple cars, serious injuries, or other circumstances that feel completely overwhelming to manage on your own.

- Policy Interpretation Disputes: The denial of your claim hinges on confusing policy language. The insurer insists a clause means one thing, but it seems intentionally ambiguous or unfair.

A public adjuster is your licensed advocate, hired to manage the entire claims process on your behalf. They take over all communications, decipher dense policy documents, and use the auto insurance appraisal as one piece of evidence in a much broader strategy to get you a full and fair settlement.

Hiring a public adjuster takes the immense stress of battling an insurance company off your shoulders. They step in to level the playing field, letting you focus on what matters while they fight for the financial outcome you're entitled to. For a deeper dive, our guide on when to hire a public adjuster breaks down the process even further. Their job is to make sure you receive everything you are owed under the terms of your policy.

Answering Your Questions About Auto Appraisals

Going through a total loss claim brings up a ton of questions. It's a confusing process, and feeling like you're in the dark only makes it worse. Let's clear things up with some straightforward answers to the most common questions we hear about auto insurance appraisals.

Can I Keep My Car If It's a Total Loss?

Yes, in most situations, you have the option to keep your car even after the insurance company has declared it a total loss. This is sometimes called “owner retention.”

If you go this route, here's what happens: the insurer calculates the Actual Cash Value (ACV) of your car and then subtracts its salvage value. The salvage value is what they would have gotten by selling the wrecked car to a salvage yard. You get a check for the difference. Just be aware that the car will now have a salvage title, which can make it very difficult to insure or sell down the road.

Who Is Qualified to Be an Appraiser?

You might be surprised to learn there isn't a single, universal license for auto appraisers. What truly matters is deep, hands-on experience in the automotive world.

When you're looking for an appraiser, you need someone who is:

- Competent: They need an encyclopedic knowledge of vehicle values, condition grading, and the trends in your specific local market.

- Impartial: Their opinion must be completely unbiased. They can't have any stake in the outcome of your claim.

- Disinterested: This is a big one. A legitimate appraiser works for a flat fee or an hourly rate, not on contingency. Their pay should never depend on the final settlement amount.

Don’t just hire the cheapest person you can find. An appraiser with a rock-solid reputation and years of experience builds a much stronger case and earns more respect from the insurance company and, if it comes to it, the umpire.

What If My Appraiser and the Insurer’s Appraiser Can’t Agree?

This happens, and the appraisal clause has a built-in solution: the umpire. If your appraiser and the insurance company's appraiser hit a wall, they will work together to select a neutral, qualified expert to act as a tie-breaker.

Both appraisers will present their findings and arguments to the umpire. The final, binding settlement value is set as soon as any two of the three parties (your appraiser, the insurer's appraiser, or the umpire) come to an agreement. This structure guarantees that a resolution can always be reached, even when the two sides start far apart.

Feeling like you're fighting an uphill battle with your insurance claim? You don't have to do it alone. NW Claims Management is a licensed public adjusting firm that advocates for property owners like you in Oregon and Washington. Our team digs in to handle every detail, from documenting the full extent of your loss to negotiating with the insurer, making sure you get the maximum settlement you're entitled to. Get your free claim evaluation and find out how we can help.