When a disaster damages your property, the visible destruction is just the start. The real fight often begins when you have to prove the full financial impact of your loss, and that's where forensic accounting services come in. Think of them as financial detectives for your insurance claim, working to make sure every single dollar is accounted for.

Unraveling the Financial Truth in Your Property Claim

A major property claim is a lot like an iceberg. The physical damage you can see—the charred walls or a flooded-out basement—is only the tip. Underneath the surface lies a massive, complicated body of financial loss that’s much harder to see and even tougher to prove. This hidden part of the claim is where the real battle with the insurance company often takes place.

Insurance carriers are experts at dissecting every line of a claim. If you can’t provide ironclad proof, they have an opening to undervalue or even deny huge parts of your settlement. This is especially common for losses that aren't simple to calculate, like lost business income or the true value of personal belongings you've collected over a lifetime.

Why Your Regular Accountant Isn't Enough

Your day-to-day accountant is fantastic for keeping the books, handling taxes, and managing payroll. But they aren't equipped for the adversarial world of a high-stakes insurance claim. Their job is to record financial history, not to investigate and defend it in a dispute.

This is precisely where forensic accounting services make a difference. These professionals are part accountant, part detective. They are trained to dig deep, reconstruct records that might have been destroyed, and present financial evidence in a way that holds up under intense pressure.

A forensic accountant’s main job is to turn a chaotic pile of receipts, bank statements, and projections into a clear, logical, and defensible story of your financial loss. Their work gives your claim the factual foundation it needs to succeed.

Building an Undeniable Case

For homeowners and businesses in Oregon and Washington, a complex claim demands a solid strategy. To truly get to the bottom of your financial losses, especially for complicated issues like business interruption, understanding how forensic accountants help with BI insurance claims is a game-changer. Their detailed reports offer the kind of objective, third-party validation that an insurance company can't just brush aside.

A forensic accountant works right alongside your public adjuster, helping to build an airtight case. While your public adjuster steers the overall claim strategy, the forensic accountant provides the hard numbers to back it up. This teamwork means you're fully prepared for the tough process of negotiating with an insurance company and ready to counter their attempts to pay you less.

Ultimately, bringing in a forensic accountant is about leveling the playing field. They bring a level of financial rigor that empowers you to demand—and get—the full and fair settlement you're owed under your policy. This guide will walk you through exactly how they do it.

What Exactly Are Forensic Accounting Services?

Think of your regular accountant like a trusted family doctor. They handle your routine financial check-ups, make sure everything is healthy, and keep your records in good order. A forensic accountant, however, is the specialist you call when something has gone seriously wrong. They are the financial detectives brought in to investigate a problem, figure out what happened, and determine the financial impact.

Their work goes far beyond just crunching numbers. While a traditional accountant’s goal is to organize and report on financial data, a forensic accountant is trained to scrutinize that data. They blend accounting expertise with investigative skills to look for irregularities, errors, or signs of deception. The entire point is to uncover financial facts that can hold up under the intense pressure of a legal or insurance dispute.

This specialized field is growing for a reason. The global market for forensic accounting services hit USD 18.85 billion in 2024 and is expected to nearly double by 2034, driven by increasingly complex financial disputes and fraud cases.

The Focus on Litigation Support

What really sets forensic accounting apart is its purpose. Almost every forensic accounting engagement is done with a potential legal battle in mind, whether it's a major insurance claim, a courtroom case, or a dispute between business partners. This focus on litigation support changes everything.

From the very beginning, their process is designed to produce solid evidence. They don’t just accept the books as they are; they reconstruct the financial story piece by piece, often from messy or incomplete records. To build a complete picture from complex financial documents, these experts often use advanced document analysis techniques to connect the dots and uncover the full story.

The goal isn't to produce a standard tax return or a profit-and-loss statement. Instead, they deliver a detailed, defensible report that proves a financial loss, quantifies damages, or identifies hidden assets in a way that an insurance carrier, judge, or jury can clearly understand.

Standard Accounting vs. Forensic Accounting at a Glance

To put it simply, a standard accountant is there to ensure compliance and track performance when things are running smoothly. A forensic accountant is called in precisely because things are not running smoothly.

This table breaks down the core differences in their roles and mindsets.

| Aspect | Standard Accounting | Forensic Accounting |

|---|---|---|

| Objective | Record and summarize financial data for routine reporting. | Investigate financial data for a specific legal purpose. |

| Scope | Broad and ongoing, covering all financial activity. | Narrow and specific, focused on a particular issue or time period. |

| Mindset | Accepting and compliant; assumes data is accurate. | Skeptical and investigative; assumes data may be incorrect or manipulated. |

| Output | Financial statements, tax returns, management reports. | Expert reports, evidence for litigation, damage calculations. |

As you can see, while both professionals work with numbers, they operate in two completely different worlds with different goals and rules.

Think of it this way: a standard accountant paints a picture of what is. A forensic accountant analyzes that picture to find out what happened, how it happened, and who is financially responsible.

For a business or property owner facing a complex insurance claim, that difference is everything. Your insurer's team will challenge your financial calculations at every step. A forensic accountant provides the specialized expertise needed to not just state your losses, but to prove them with credible, unshakeable evidence. They turn a mountain of confusing data into your most powerful tool for recovery.

When You Need a Forensic Accountant for Your Property Claim

Knowing when to bring in a financial specialist can be one of the most critical decisions you make after a property loss. While a public adjuster is your go-to expert for managing the overall claim, some situations are just too financially tangled for anyone but a forensic accountant.

These aren't everyday scenarios. Think of them as specific red flags telling you that your claim is heading into choppy waters where hard financial proof isn't just helpful—it's essential.

Hiring a forensic accountant is a strategic move. It's about knowing when to deploy a specialist for a mission that requires a unique skill set. Understanding these signs also helps you know when to hire a public adjuster in the first place, as they're the ones who will recognize the perfect moment to bring in this financial expert.

Let's walk through the key situations where a forensic accountant becomes absolutely necessary.

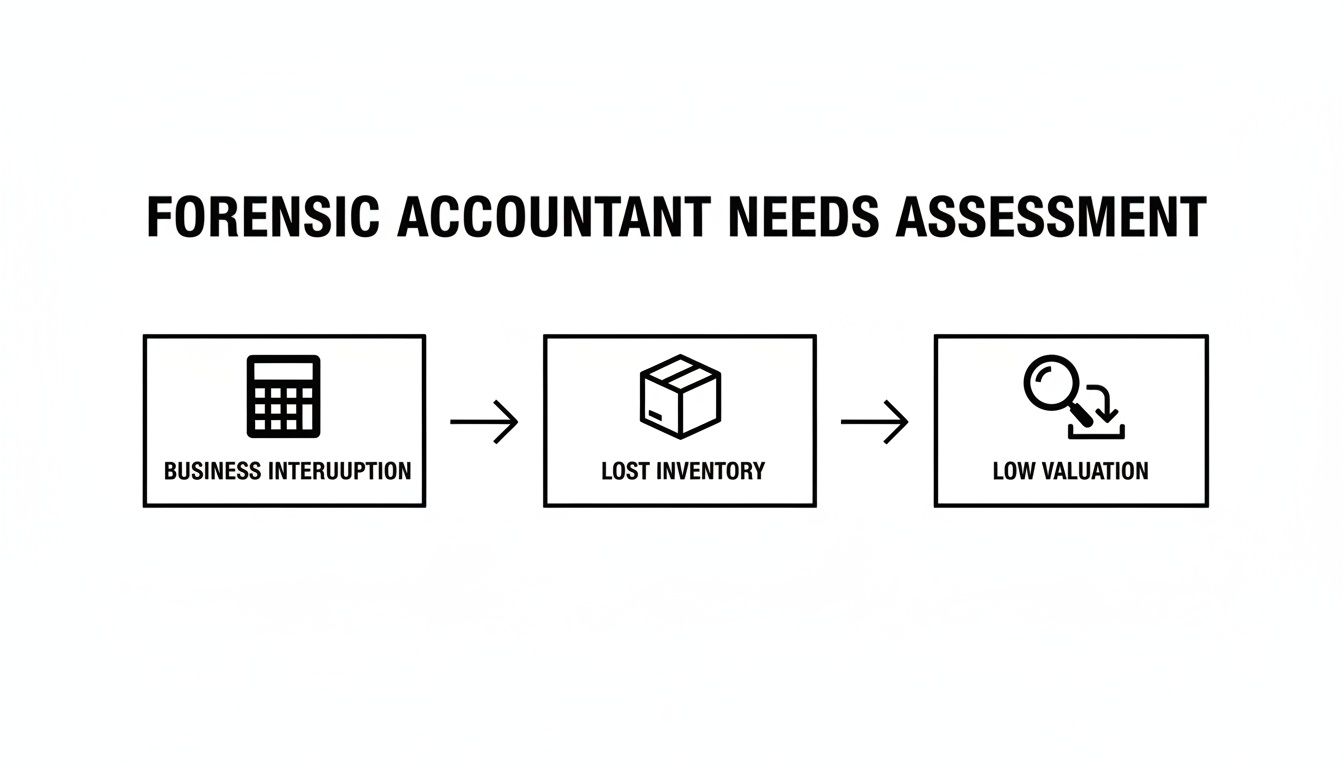

Calculating Complex Business Interruption Losses

When a fire, flood, or other disaster shuts your business down, your business interruption (BI) claim is about so much more than just lost sales. An insurance company's adjuster will often try to simplify the loss with a basic revenue formula. Frankly, this shortcut almost always misses the true, full financial impact of the shutdown.

A forensic accountant digs much, much deeper. Their job is to reconstruct a detailed picture of what your business’s financial performance would have been if the disaster had never struck.

This isn't guesswork. It's a meticulous analysis of:

- Historical Trends: They'll look at your seasonality, real growth patterns, and market conditions to project your future revenue with credibility.

- Saved Expenses: They properly identify and calculate costs you didn't incur during the shutdown (like certain raw material purchases), which makes your net loss figure fair and bulletproof.

- Extra Expenses: They document and justify every single dollar you spent to get back on your feet faster, from renting a temporary location to paying overtime wages.

Example: A thriving Portland restaurant suffers a kitchen fire and has to close for four months. The insurance company's initial offer is based on the previous year's sales. But a forensic accountant steps in and proves the restaurant was on a 25% year-over-year growth trajectory, had just launched a profitable catering division, and had major events booked. Their report, which projected this lost growth, led to a settlement that was nearly double the insurer's lowball offer.

Documenting High-Value or Extensive Personal Property

After a total loss like a house fire, the thought of creating an inventory of every single thing you owned is absolutely heartbreaking. For homeowners with unique collections, extensive wardrobes, or specialized gear, just listing items isn't nearly enough. You have to prove what they were worth.

A forensic accountant helps build an undeniable inventory and valuation report. They can trace purchases back through years of bank statements, research the market value for rare or antique items, and package it all in a way that insurance companies must take seriously. This process stops the insurer from just slapping a low, generic "used" value on your most cherished possessions.

Example: A Seattle-area homeowner loses everything in a fire, including a massive collection of vintage vinyl records and original local art. The adjuster offers a flat, insulting value for "used records and art." A forensic accountant gets to work, meticulously documenting the collection with auction records, gallery sales data, and expert appraisals to establish the true market value of each piece. This secured a fair payment for assets that were anything but generic.

Uncovering Financial Fraud or Misconduct

Unfortunately, property claims can sometimes get tangled up in accusations of fraud. One of the most serious is arson-for-profit, where an insurer alleges a property was intentionally destroyed to collect the insurance money. When this happens, the insurance company will unleash its own team of forensic accountants to build a case against you. You absolutely need your own expert to fight fire with fire.

Your forensic accountant will analyze your financial records to prove you had no motive. They can show that your business was profitable or that your personal finances were stable, directly countering the insurer's narrative that you were financially desperate. Their independent analysis is a powerful shield against a bad-faith denial.

Challenging the Insurer’s Low Valuation

This is probably the most common reason people need forensic accounting services: the insurance company’s settlement offer is drastically, insultingly low. Insurers use their own experts and estimators whose reports often seem designed to protect the company's bottom line, not to make you whole.

When you're up against a lowball offer, a forensic accountant provides the objective, third-party analysis you need to push back effectively. They conduct their own independent valuation of your damages, whether it's the cost to rebuild a commercial property or the true value of all your lost inventory.

Their report becomes powerful leverage in negotiations. It shows the insurer you have the facts on your side and are prepared to prove it. The dispute is no longer your word against theirs—it's a battle of documented, expert-backed evidence.

The Forensic Accounting Process From Start to Finish

Knowing you need forensic accounting services is one thing; understanding what actually happens when you hire one can make the whole process feel a lot less intimidating. It’s not just about dumping a box of receipts on a desk. A good forensic accounting engagement is a methodical investigation with a very clear goal: a rock-solid financial report that substantiates your insurance claim.

Think of it as a financial detective story. Instead of looking for a criminal, the forensic accountant is hunting for the undeniable truth of your financial loss. Every step is meticulously documented, building a case that can stand up to the toughest scrutiny from an insurance carrier.

Stage 1: The Initial Consultation and Engagement

It all starts with a kickoff meeting. This is far more than a casual chat—it’s a strategy session. Here, you, your public adjuster, and the forensic accountant will sit down to map out the scope and objectives of the investigation, digging into the specifics of your loss and exactly what needs to be proven.

During this first phase, the accountant will:

- Set Clear Goals: Are we calculating a complex business interruption loss? Valuing a massive inventory that went up in smoke? Or are we pushing back against an insurer's lowball offer?

- Review Key Documents: They'll want to see your insurance policy, the carrier's initial damage reports, and any back-and-forth you've already had.

- Draft an Engagement Letter: This is a formal document that lays out the scope of work, the estimated timeline, and the fee structure. It ensures everyone is on the same page from day one.

Getting this first step right is critical. It sets the entire investigation on the proper course and ensures the final report directly tackles the core issues of your claim. A solid roadmap at the beginning saves a lot of time and money down the road.

Stage 2: Evidence Gathering and Organization

Once the game plan is set, the real detective work begins. The forensic accountant starts pulling together every piece of relevant financial data. Frankly, this is often the most time-consuming part of the job because records can be messy, incomplete, or even lost in the disaster itself.

The accountant will be on the hunt for historical financial statements, tax returns, payroll records, bank statements, sales forecasts, invoices, and purchase orders. For a homeowner, this might mean combing through old emails for digital receipts and credit card statements to reconstruct a personal property inventory from scratch. Every single document matters.

The goal is to build a comprehensive financial picture of your life or business before the loss occurred. This baseline becomes the foundation for accurately measuring what was taken away.

Stage 3: Analysis and Modeling

This is where the magic really happens. The accountant shifts from simply collecting information to interpreting it. Using specialized techniques, they trace transactions, verify figures, and build a sophisticated financial model of your loss.

For instance, when calculating a business interruption claim, they don't just average your past profits. A true expert builds a dynamic financial model that accounts for seasonality, market trends, and your company’s growth trajectory to prove what your business would have earned. This is worlds away from the simplistic, and often unfavorable, formulas insurance adjusters tend to use. This financial analysis is also informed by the physical damage, making a thorough property damage assessment a crucial and complementary step.

Stage 4: Reporting and Resolution

With the analysis complete, all the findings are compiled into a formal, written report. This is no mere spreadsheet. It's a narrative-driven document that clearly explains the methodology, presents the supporting evidence, and lays out the final conclusion in a way that even non-accountants can easily grasp.

This report becomes your single most powerful negotiating tool. It gives the insurance company a defensible, third-party, expert-backed valuation that's incredibly difficult to argue with. Should the claim end up in court, the forensic accountant can then serve as a credible expert witness, ready to explain their findings to a judge and jury. This step-by-step process delivers a robust conclusion designed to get you the best possible settlement.

How Forensic Accountants and Public Adjusters Work Together

When you're navigating a major property insurance claim, it's easy to think you just hire one person to handle it all. But in reality, you're assembling a team of specialists. Two of the most important players you can have on your side are the public adjuster and the forensic accountant. They aren't overlapping roles; they form a powerful partnership, with each expert playing a crucial, complementary part.

Here’s a good way to picture it: Imagine rebuilding a custom home after a devastating fire. Your public adjuster is the general contractor. They manage the entire project from start to finish—interpreting the building codes (your insurance policy), coordinating all the moving parts, and negotiating with inspectors (the insurance company) to make sure the final result is exactly what you're owed.

But what if the project involves an incredibly complex structural element, like a cantilevered design or a tricky foundation on a hillside? A good general contractor knows their limits and brings in a structural engineer. The engineer doesn’t run the whole job site; they bring their specialized expertise to bear on one critical component. That's the exact role a forensic accountant plays in your claim.

The Public Adjuster: Your Claim's Quarterback

Your public adjuster is the strategic leader of your entire claim. They are your primary advocate, and their job is to see the big picture and manage every detail. An experienced public adjuster, like the team here at NW Claims Management, will:

- Run the entire claim process for you, from the moment you file until you have a settlement check in hand.

- Document all property damage, both the obvious destruction and the hidden issues that often get missed.

- Analyze your insurance policy to identify every bit of coverage you're entitled to.

- Lead all communications and negotiations with the insurance company's own adjusters and representatives.

A huge part of their value is knowing when a claim’s financial side becomes too complex for standard methods. A seasoned public adjuster knows exactly when to call in the "financial special forces" to make the case for your losses undeniable. It’s a key part of understanding the difference between a public adjuster vs an insurance adjuster.

The Forensic Accountant: The Financial Specialist

The forensic accountant is the specialist your public adjuster brings in for specific, high-stakes financial analysis. They don't manage the overall claim. Instead, they dive deep into the numbers to prove your most complicated financial losses, like a business interruption or a dispute over asset valuation.

Their only job is to produce a completely objective, evidence-based report that clearly documents your financial damages.

This partnership creates a powerful one-two punch. The public adjuster directs the overall strategy and manages the claim, while the forensic accountant provides the rock-solid financial evidence needed to win the toughest parts of the negotiation.

This need for deep financial investigation is becoming more common. In fact, the demand for forensic accounting services is growing fastest among regulatory bodies and law enforcement agencies trying to unravel complex financial crimes. This mirrors what we see in insurance, where policyholders must prove their financial losses with the same forensic rigor that investigators use to follow a money trail. You can read more about this trend in a recent forensic accounting market report.

By working together, the public adjuster and forensic accountant make sure nothing gets missed. The adjuster builds the complete framework of the claim, and the accountant reinforces it with bulletproof financial data. This collaborative strategy eliminates the weak spots an insurer might try to exploit, presenting a unified and powerful front that ultimately maximizes your recovery.

Choosing the Right Forensic Accountant in Oregon and Washington

When you’re facing a complex insurance claim, picking the right financial expert is one of the most critical decisions you'll make. This isn't just about finding someone who's good with spreadsheets. You need a specialist who has the right credentials, the right kind of experience, and a genuine understanding of our local business environment.

Getting the right pro on your team from the get-go sends a powerful message. It lends a level of credibility to your claim that an insurance carrier simply can't ignore.

Essential Credentials and Experience

First things first, let's talk about the non-negotiables. Certain professional qualifications are the bare minimum, acting as your assurance that an accountant has met rigorous industry standards.

Look for these two key certifications:

- Certified Public Accountant (CPA): Think of this as the foundation. A CPA has a strong, comprehensive background in all things accounting.

- Certified in Financial Forensics (CFF): This is the specialization that truly matters for your claim. Awarded by the American Institute of CPAs, the CFF credential is the gold standard, proving an accountant has specific training in financial investigation and dispute resolution.

But credentials alone aren't enough. You have to dig into their actual case history. An accountant who spends their days in divorce court or untangling internal corporate fraud won't know the first thing about the specific rules and documentation required for a business interruption claim.

What really matters is a proven track record of quantifying and successfully defending financial losses in property insurance claims. That specific, niche experience is infinitely more valuable than a general forensic accounting background.

The Importance of Local Knowledge

Having an expert who understands the Pacific Northwest economy isn't just a nice-to-have; it's a strategic advantage. A forensic accountant who knows the ins and outs of the business climate in Portland, Seattle, or the surrounding areas can build a far more accurate and defensible case for your losses.

For example, a local pro will already be familiar with regional supply chains, current labor rates in Oregon and Washington, and the unique market trends affecting your industry here. This ground-level insight makes their financial projections much more credible than numbers pulled from a national database by an out-of-state firm.

Critical Questions to Ask in a Consultation

Once you've narrowed your list down to a few qualified candidates, it’s time to interview them. Your goal here is to see beyond the resume and find out if they’re the right partner for your specific fight.

Don’t be shy about asking direct questions. Here’s what you need to know:

- Have you handled a claim like mine before? Get specific. Ask about their experience with a restaurant BI claim, a manufacturer's inventory loss, or whatever matches your situation.

- What percentage of your work is for policyholders in property insurance claims? This tells you if they are truly specialized or just dabbling.

- How do you structure your fees? You need total clarity on whether they charge by the hour, require a retainer, or use a different model. No surprises.

- Will you be the person personally handling my case? It's common for a senior partner to make the sale, then pass the real work to a junior associate. Make sure you know who you will actually be working with.

- Can you provide a redacted example of a report you've prepared for a similar case? Seeing their work product is the best way to judge its quality, clarity, and persuasiveness.

Asking these tough questions upfront empowers you to make an informed choice. You’re not just hiring an accountant; you’re partnering with an expert who has the precise skills and experience needed to get your claim paid fairly.

Common Questions About Forensic Accounting Services

If you're thinking about bringing a forensic accountant onto your team, you're probably wondering exactly what that entails. It's a specialized field, and it's completely normal to have questions before you commit. We've put together straightforward answers to the questions we hear most often from property and business owners.

Are These Services Only for Big Companies?

Absolutely not. It's a common misconception that forensic accounting is just for massive corporations dealing with multimillion-dollar fraud. In reality, their skills are valuable for any person or business facing a complex financial loss, regardless of size.

Think of it this way: the need isn't determined by the size of your business, but by the complexity of your financial paperwork. A small retail shop with a business interruption claim, a nonprofit struggling to document post-disaster expenses, or even a homeowner whose high-value personal property was undervalued can all benefit immensely. The goal is always the same: to get a fair and accurate settlement.

How Much Do Forensic Accountants Cost?

This is always a top concern, and the answer depends entirely on the scope of the work. Most forensic accountants charge by the hour, with rates typically falling between $250 to over $500 per hour.

While that hourly rate might seem high, it’s important to see the bigger picture. This cost is often just a small fraction of the additional settlement money a forensic accountant can help you recover. Their detailed reports provide the hard proof needed to substantiate losses that an insurer might otherwise deny or severely underpay. In most cases, their work pays for itself several times over.

The real question isn't just about the cost, but the return on your investment. A skillfully prepared financial report can be the difference between a lowball offer and a settlement that truly makes you whole.

Can I Just Use My Regular Accountant?

While your day-to-day accountant is a trusted expert for taxes and bookkeeping, they operate in a completely different world. Routine accounting is about compliance and organization; forensic accounting is about investigation and conflict.

A forensic accountant is specifically trained to dig into the details, find out what went wrong, and build a financial case that can withstand intense scrutiny from insurance company lawyers. They know the rules of evidence and how to present financial data in an adversarial setting. It’s a specialized skill set for a specialized problem. You can learn more about how policy details impact this process in our guide on understanding insurance policy limits.

How Long Does an Investigation Take?

The timeline for a forensic accounting investigation can vary quite a bit. A simpler case, like calculating the value of lost inventory from well-kept records, might wrap up in just a few weeks.

However, a more involved business interruption claim with messy documentation or a case involving suspected fraud will naturally take longer. A thorough investigation in these situations could take several months to complete correctly. Your forensic accountant will give you a much clearer timeline after they’ve had a chance to do an initial review of your situation.

Navigating the financial complexities of a major property claim requires a dedicated team. If you have questions about your claim, NW Claims Management provides free evaluations to help you understand your options and secure the full, fair settlement you deserve. Contact us today to learn more.