You're probably reading this after a bad day. Maybe a fire tore through part of your house in Portland. Maybe a pipe burst in Seattle and soaked walls, flooring, and cabinets. Maybe you've already opened your policy and found language that looks familiar until you need it to mean something.

Then two phrases jump out at you: agreed value and replacement cost.

Those aren't technical side notes. They decide whether your insurance claim helps you rebuild or leaves you covering a painful gap yourself. And when a carrier wants to control the claim, these clauses provide them with an advantage. The policyholder sees “covered.” The insurer looks for conditions, depreciation, limits, timing requirements, and loopholes.

That's why the agreed value vs replacement cost question matters so much. Not because it sounds complex, but because it determines who holds the stronger position after a loss. If you understand how these clauses work before the claim gets away from you, you keep more control. If you don't, the insurer usually does.

The Most Important Clause You Have Never Read

A homeowner stands in a damaged kitchen, staring at smoke-stained drywall and a warped ceiling. The contractor says the room has to be gutted. The insurer says it's covered. That sounds reassuring for about five minutes.

Then the main fight starts.

The carrier asks for photos, inventories, estimates, proof of repairs, proof of replacement, and sometimes a second round of paperwork after the first check goes out. The homeowner assumes the policy will pay what it takes to put the home back. The insurer reads the same policy and starts applying valuation language that policyholders never focused on when they bought coverage.

Why this clause matters after a loss

Agreed value and replacement cost are often treated like simple definitions. They're not. They are claim outcomes disguised as policy language.

With agreed value, the amount is set in advance. That can limit post-loss arguments if the policy is written correctly and the property fits that structure.

With replacement cost, the amount is usually determined after the loss based on what the insurer says it should cost to repair or rebuild with comparable materials. That sounds fair until you're the one challenging a thin estimate, delayed payments, or depreciation holdbacks.

The most expensive mistake property owners make is assuming “replacement cost” means a full check arrives when they need it most.

Where owners get blindsided

Most policyholders never compare valuation clauses with the same care they use when comparing deductibles or premiums. That's understandable. Insurance is sold as peace of mind, not as a post-loss negotiation manual.

But after a serious loss, this clause often matters more than anything else on the declarations page. It affects:

- How the insurer values the damage

- Whether depreciation reduces your initial payment

- How much money you must front before full reimbursement

- How much room the insurer has to argue

If you own property in Oregon or Washington, this matters even more. Rebuild disputes, material matching fights, and local code issues can turn a “covered claim” into a drawn-out payment battle fast.

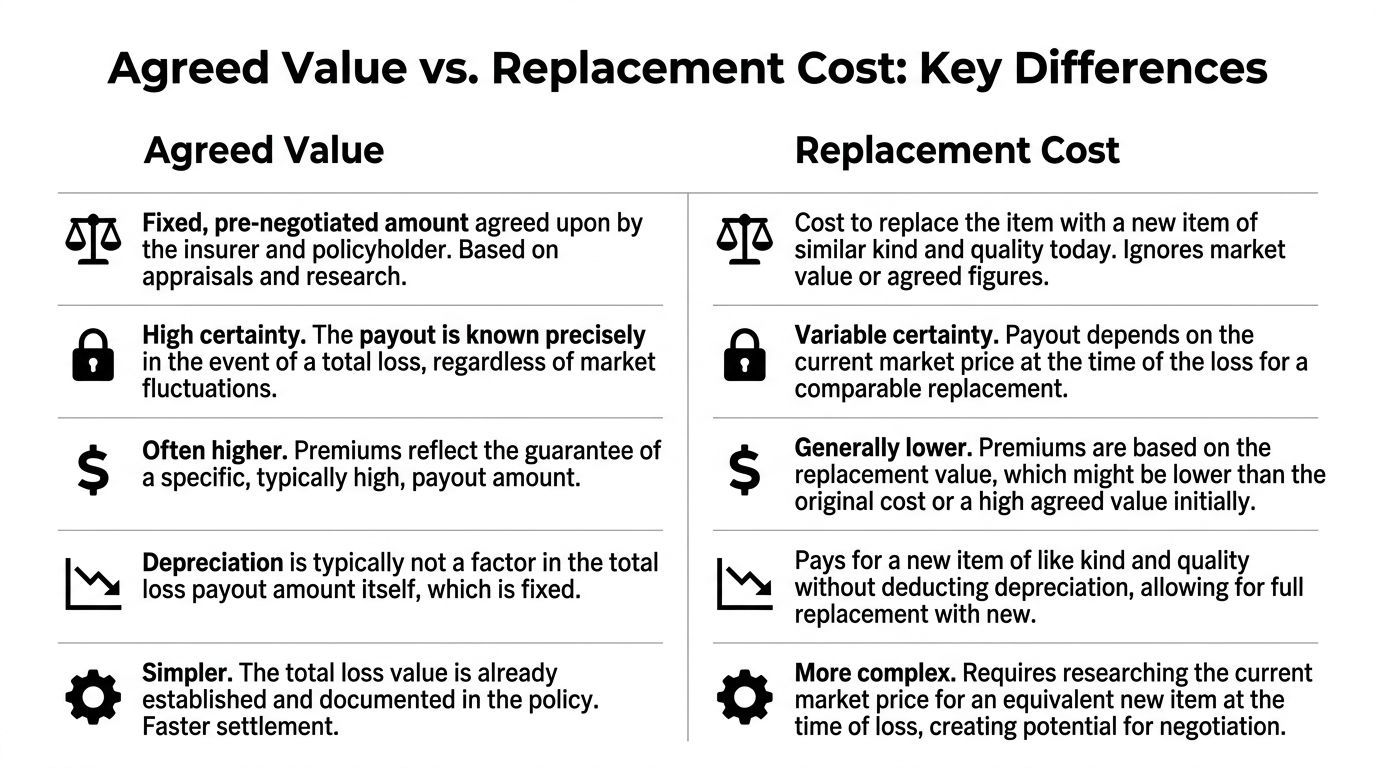

Defining Agreed Value and Replacement Cost

Let's strip the jargon out of this.

Agreed value means you and the insurer settle on a value before the loss happens. It functions similarly to a fixed-price contract. If the covered loss triggers that valuation structure, the pre-set number drives the payout instead of a fresh argument after the damage occurs.

Replacement cost means the policy aims to pay what it costs to repair or replace damaged property with materials of like kind and quality, subject to the policy's terms, limits, and conditions. Think of it more like a cost-based arrangement that gets argued after the fact.

Agreed value in plain English

Agreed value works best when the property is unusual, custom, historic, or otherwise hard to price with a generic estimate. A standard replacement calculator may miss the actual value of specialty materials, handcrafted features, or one-off construction.

The upside is certainty. The downside is that agreed value has to be set correctly at the start. If the agreed amount is stale or too low, certainty won't help you much.

Replacement cost in plain English

Replacement cost is common on homes and buildings because insurers prefer a structure that lets them evaluate the loss after it happens. That gives them more room to inspect, estimate, depreciate, and question scope.

Many owners often confuse replacement cost value with actual cash value. They are not the same. Actual cash value usually means the insurer subtracts depreciation. Replacement cost is supposed to get you to the repair or rebuild cost, but many policies pay in stages. You may first receive an actual cash value payment and only recover withheld depreciation after repairs are completed and documented.

If you want a clean breakdown of that distinction, this guide on actual cash value vs replacement cost is worth reading.

The key distinction

Here's the simplest way to remember agreed value vs replacement cost:

- Agreed value is decided before the loss.

- Replacement cost is usually fought over after the loss.

That difference alone tells you why insurers often prefer replacement cost language on ordinary property and why policyholders need to read the conditions attached to it.

Core Differences A Side-by-Side Comparison

The fastest way to understand agreed value vs replacement cost is to compare them where claims break down.

| Feature | Agreed Value | Replacement Cost |

|---|---|---|

| Valuation basis | Set before the loss | Determined after the loss |

| Payout certainty | More predictable if the policy wording is clear | Less predictable because scope and pricing can be disputed |

| Depreciation | Typically not the main battleground in a total loss structure | Often used to reduce the initial payment |

| Claim process | Usually more direct on value | Often involves estimates, supplements, receipts, and payment stages |

| Best fit | Unique, custom, historic, or hard-to-price property | Standard homes and buildings with easier market-based estimating |

| Common insurer tactic | Challenge whether the agreed amount applies as written | Underscope repairs, over-depreciate items, or delay release of withheld amounts |

| Cash flow burden on owner | Usually lower if coverage responds as expected | Often higher because owners may need to front repair costs |

| Main risk for policyholder | Setting the value too low before the loss | Discovering after the loss that “replacement” comes with strings attached |

Agreed value gives you certainty, if it's written right

Agreed value reduces one major source of claim friction: post-loss valuation. That matters when the property doesn't fit cookie-cutter pricing. A custom home, older structure with specialty details, or unique commercial building can be hard to price fairly after disaster hits.

But don't confuse agreed value with automatic safety. If the insured amount was selected casually, never updated, or based on wishful thinking, the insurer will still rely on the written number.

Replacement cost sounds generous, but it often gives insurers more room

Replacement cost is attractive in marketing because it sounds like full restoration. The claim reality is rougher. Carriers often control the estimate, decide what materials are “comparable,” and pay less up front than owners expect.

That's not necessarily bad faith by itself. It's how many policies are structured. The problem is that policyholders hear “replacement cost” and assume smooth payment, when the process itself can involve multiple rounds of review and proof.

Why the claim process matters more than the label

Two policies can both say replacement cost and behave very differently in practice. One carrier may handle supplements reasonably. Another may force repeated documentation, narrow the scope of repair, and resist code-related upgrades until pushed.

Practical rule: Don't judge coverage by the headline term alone. Judge it by the conditions for getting paid in full.

When comparing agreed value vs replacement cost, ask which option leaves the insurer with fewer opportunities to reinterpret your loss after the fact. That is usually the better answer for your financial interests.

How Payouts Are Calculated in the Real World

Definitions are fine. Claims are where policy language provides an advantage.

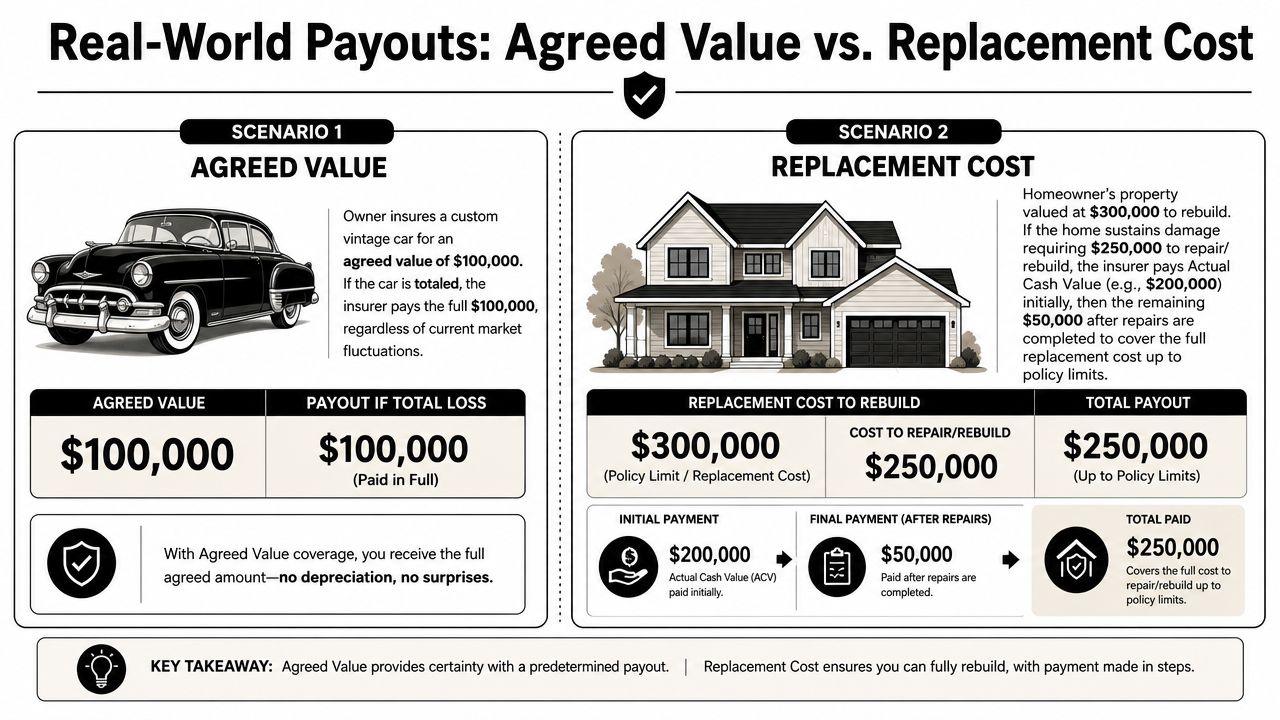

Scenario one with agreed value

A property owner in Bend has a custom home with distinctive finishes, built-ins, and features that don't fit standard estimating templates well. Before any loss occurred, the owner and insurer agreed on a value for coverage purposes.

A fire later causes a total covered loss.

The key advantage here is that the biggest valuation fight happened before the disaster, not after it. The owner doesn't have to stand in the debris field and argue about whether the custom millwork, specialty stone, or nonstandard layout should be priced like builder-grade construction. If the policy language is solid and the agreed amount applies, the claim path is more direct.

That doesn't mean the insurer won't review causation, exclusions, or compliance with policy conditions. It means the value itself is less available for post-loss manipulation.

Scenario two with replacement cost

A homeowner in Seattle suffers a kitchen fire. Cabinets are damaged, smoke travels into nearby rooms, and the flooring may need matching work beyond the immediate burn area.

The insurer sends an adjuster and issues an estimate. The estimate may leave out some demolition, underprice finish work, or assume lower-grade replacement materials. Then the carrier calculates depreciation on parts of the claim and pays an initial amount based on actual cash value.

The homeowner now has several problems at once:

The repair scope may be too narrow

The estimate might address visible damage but miss hidden smoke contamination, electrical checks, insulation removal, or matching issues.The first payment may not be enough to start work comfortably

Contractors usually don't care that the insurer withheld depreciation. They care about deposits, scheduling, and signed scopes.The withheld amount may require proof before release

Many replacement cost claims require the owner to complete repairs, submit invoices, and satisfy deadlines before recoverable depreciation is paid.

A lot of owners don't realize how estimate software shapes these disputes. If you want a closer look at the tool many carriers and adjusters rely on, review this explanation of the Xactimate estimating platform.

What this means in practice

Agreed value can reduce uncertainty when the property is difficult to price. Replacement cost can work well too, but only if the estimate is accurate, the conditions are realistic, and the carrier handles supplements fairly.

If not, the policyholder ends up financing part of the claim while arguing for the rest. That's the quiet problem with replacement cost. It may promise full repair value in theory while creating a cash-flow squeeze in practice.

Special Considerations for Oregon and Washington

Insurance disputes are local. Policy wording matters everywhere, but state law and claim handling standards shape how these fights play out on the ground.

Oregon issues that owners should know

Oregon property owners need to pay close attention to how total fire losses are treated under the state's valued policy law, ORS 742.240. In plain terms, that law can affect how policy limits are paid in a total loss by fire. For some owners, that creates protection that functions more like an agreed value outcome in that narrow setting.

That doesn't solve every dispute. Insurers may still contest scope, cause, exclusions, compliance, or whether the loss meets the standard for that result. But Oregon owners should know this issue exists because it can materially change the settlement discussion.

Washington disputes often center on quality and scope

In Washington, one of the most common battlegrounds in replacement cost claims is what counts as like kind and quality. The insurer may say a lower-grade material is close enough. The owner may know it isn't.

That fight shows up in roofing, flooring, cabinetry, finish carpentry, and commercial interiors all the time. Matching also becomes a pressure point. A patch may technically repair damage, while still leaving the property with an obvious mismatch.

For owners in either state, local claim knowledge matters. A licensed advocate who understands regional practices, contractor pricing, and policy interpretation can spot issues that a generalist misses. If you need help understanding who represents policyholders rather than carriers, review what a licensed public adjuster does.

In Oregon and Washington, the dispute usually isn't whether the policy exists. It's what the insurer says the policy owes.

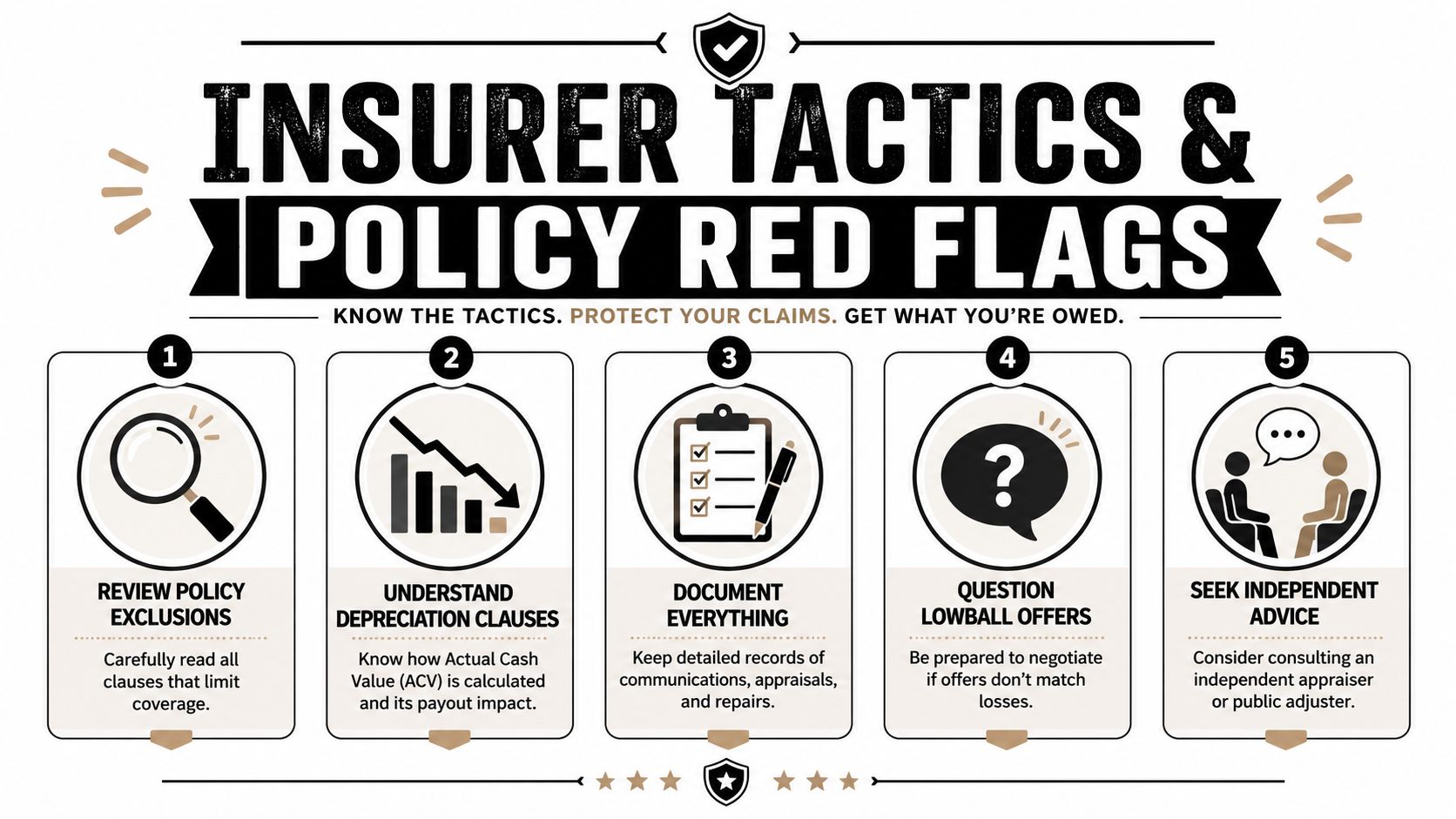

Insurer Tactics and Red Flags in Your Policy

Most policyholders assume the fight starts after they file the claim. Often, the groundwork for underpayment was laid when the policy was written.

Tactics carriers use on replacement cost claims

Here are the patterns property owners run into again and again:

Low initial estimates

The first estimate may omit code items, hidden damage, specialty trades, overhead, profit, or realistic finish pricing.Aggressive depreciation

Carriers may apply depreciation broadly, including to components that don't make practical sense in context, which shrinks the first check.Inferior material assumptions

The policy promises like kind and quality, but the estimate prices lower-end cabinets, flooring, roofing, or trim.Artificially narrow repair scopes

The insurer focuses on visibly damaged areas while minimizing related repairs needed to complete the job correctly.Delay through documentation requests

Some requests are legitimate. Some are used to slow momentum and pressure acceptance.

If any of that sounds familiar, this breakdown of common insurance adjuster tricks will feel uncomfortably accurate.

Red-flag phrases in your policy

Read your policy with suspicion, not optimism. Watch for wording like this:

“We will pay no more than the actual cash value of the damage until actual repair or replacement is completed.”

That means you may wait for part of your money until after work is done.

“Replacement cost does not include increased costs unless specifically provided by endorsement.”

That can become a code-upgrade problem fast.

“Like kind and quality” without further clarity

That phrase sounds reasonable until the insurer uses it to justify a visibly inferior substitute.

“Repair or replacement must be completed within the time required by the policy.”

Miss a deadline during a chaotic recovery and the carrier may argue that withheld amounts are gone.

What owners should do immediately

Don't just ask whether you have replacement cost. Ask how it is paid, what conditions apply, and what proof the insurer will demand before releasing every dollar owed.

Use this short review process:

Pull the declarations page and full policy

Not the marketing summary. The actual policy form and endorsements.Find every valuation provision

Building coverage, contents coverage, endorsements, exclusions, and conditions.Circle payment-stage language

If the policy splits payment into ACV first and later reimbursement, note every deadline.Compare the insurer's estimate to real contractor scopes

Don't assume the carrier's numbers are objective.

When owners lose these disputes, it's often because they trusted broad promises and missed narrow conditions.

Your Checklist for Discussing Coverage with Insurers

You don't need to speak like an adjuster to protect yourself. You need better questions.

Questions to ask before a loss

Bring this list to your agent or broker and make them answer plainly:

Is this agreed value or replacement cost coverage?

Don't accept vague language like “full coverage.”If it's replacement cost, do you first pay actual cash value?

Ask when depreciation is withheld and when it is released.What must I do to recover the full replacement cost amount?

Get the exact requirements for repairs, receipts, timing, and proof.How do you define like kind and quality?

Push for examples involving roofing, flooring, cabinets, and trim.Does this policy include any coinsurance or underinsurance penalty?

If it does, understand how that could affect a partial loss.

Questions to ask after a loss

If the damage has already happened, the conversation changes:

- What line items did your estimate exclude and why?

- What depreciation did you apply and how did you calculate it?

- What deadlines control my right to recover withheld amounts?

- Will you pay for matching, code-triggered work, and related repairs?

- What documents do you require before releasing additional payment?

Ask the insurer to point to the exact policy language supporting its position. If they can't do that clearly, don't accept a casual verbal answer.

What a good answer sounds like

A useful insurance answer is specific, written, and tied to policy wording. A bad answer is polished but fuzzy. If you hear phrases like “that's usually how we handle it” or “you should be fine,” keep pushing.

This is one of those situations where being direct protects you. You're not being difficult. You're preventing an avoidable payment dispute.

When to Call a Public Adjuster for Your Claim

Some claims are manageable on your own. Many are not.

If the loss is modest, the damage is obvious, and the carrier's estimate is complete and fair, you may not need outside representation. But the moment the claim gets technical, expensive, delayed, or one-sided, the balance shifts hard in the insurer's favor.

Clear signs you should get help

You should seriously consider bringing in a public adjuster when:

The property is commercial, nonprofit, municipal, or otherwise complex

Multiple buildings, specialized operations, code issues, or business interruption can overwhelm a standard claim fast.The insurer's estimate feels low

If contractors say the scope is missing major items, trust that warning and investigate.Depreciation and holdbacks are choking the rebuild

Cash flow problems during repair are not minor. They can derail the whole recovery.The carrier keeps changing adjusters or asking for more paperwork

Repetition and delay wear policyholders down. That's often the point.You're exhausted

A serious property claim is a second job you never asked for.

Why representation changes the dynamic

A public adjuster reads the policy like a claim document, not a sales brochure. They review scope, valuation, exclusions, endorsements, timing requirements, and supporting documentation with one goal: protecting the policyholder's side of the file.

That matters because insurers already have trained adjusters, estimating tools, supervisors, and claim procedures working for them. Property owners usually have stress, partial information, and a damaged building.

If you're trying to decide whether this is the point to get help, this guide on when to hire a public adjuster gives a practical framework.

The short version is simple. If the claim is large, technical, disputed, or draining your time and money, don't wait for the insurer to “sort it out.” Protect yourself early.

If you're facing a property damage claim in Oregon or Washington and you want someone on your side reading the policy, documenting the loss, and challenging underpayment, contact NW Claims Management. They represent policyholders, not insurers, and they offer a free claim evaluation to help you understand your options before the claim drifts further off course.