The phone rings before you've had coffee. Your property manager says the sprinkler line burst overnight. Water ran through the ceiling grid, into tenant suites, server closets, inventory storage, and electrical rooms. Or maybe it wasn't water. Maybe it was a kitchen fire, a wind event, vandalism, or a vehicle through the storefront. Either way, your business isn't operating normally, vendors are calling, employees want direction, and your insurer wants a statement.

That moment feels like chaos because it is chaos. But your commercial insurance claim isn't just paperwork. It's a business recovery negotiation that will decide how much cash comes back into your operation, how fast repairs move, and whether you absorb losses that should have been covered.

If you've ever read a homeowner storm guide like this Upstate SC homeowner's guide to roof damage, you already know the basic truth: the first hours after damage matter. On the commercial side, the impact is greater because building damage often turns into downtime, payroll pressure, tenant issues, code upgrades, and a separate fight over lost income. If your operations are disrupted, your business interruption claim help matters just as much as the physical damage file.

Your Business Suffered a Loss Now What

You need to get organized before the insurer gets comfortable defining your loss for you.

A business owner usually starts in the wrong place. They call the carrier, answer questions on the fly, let emergency vendors in, sign whatever gets put in front of them, and assume the adjuster will sort out the numbers fairly. Sometimes the claim moves smoothly. Many times it doesn't. The insurer's team is already thinking about cause, scope, exclusions, depreciation, deductible application, and whether part of the damage can be classified as pre-existing, maintenance-related, or outside the policy period.

You need to think about recovery in the same disciplined way.

Your first job is control

Right now, your priorities are simple:

- Stop further damage: Board up openings, dry affected areas, secure the site, and keep people safe.

- Preserve evidence: Don't throw away damaged materials, electronic logs, maintenance records, or photos.

- Create one command point: Assign one person inside your business to track vendors, insurer communications, and documents.

- Avoid casual statements: Don't guess about the cause, timeline, or dollar value before you've investigated.

Practical rule: Treat day one like the beginning of an audit. If it isn't documented, expect resistance later.

This is a negotiation, not a favor

A commercial carrier owes obligations under the policy, but that doesn't mean every category of loss will be embraced without friction. The insurer has experts. You should assume every major loss will be reviewed through the insurer's financial lens.

That isn't paranoia. It's basic claim reality.

When owners understand that early, they make better choices. They photograph before cleanup. They separate emergency mitigation from permanent repair contracts. They save damaged stock lists. They ask for everything in writing. Most important, they stop expecting the insurer to build the best version of the claim on their behalf.

Decoding Your Commercial Insurance Claim

The fastest way to lose the upper hand is to misunderstand who works for whom.

A commercial claim has several players, and they don't share the same financial incentives. If you treat everyone involved as a neutral helper, you'll make expensive mistakes.

Know the roles before you answer questions

Think of the claim like a business dispute with technical rules.

- Insurance company adjuster: This person represents the insurer. Their job is to investigate, apply the policy, and value the loss from the carrier's side.

- Independent adjuster: Despite the name, this adjuster is usually independent from the carrier as a contractor, not independent in loyalty. They are hired by the insurer.

- Public adjuster: This is the adjuster who represents the policyholder.

- Third-party administrator: In some claims, a TPA helps manage claim handling for an insurer or self-insured program.

- Coverage counsel or claim counsel: Lawyers may appear when the file turns contentious, especially around exclusions, valuation disputes, or denial issues.

The money involved explains why the process is tightly managed. In the United States, commercial lines insurance accounted for 48.6% of all premiums in 2023, totaling $416.5 billion according to Fit Small Business insurance statistics. That volume tells you something important. Claims handling isn't casual. It is structured, documented, and financially defended.

The adjuster is not your project manager

Many owners assume the field adjuster will help them assemble the strongest claim possible. That's the wrong assumption.

The insurer's adjuster may be professional, responsive, and reasonable. You should still remember their assignment is to evaluate coverage and value from the insurer's position. They are not your estimator, your forensic accountant, or your advocate for overlooked categories such as code issues, hidden damage, soft costs, or extra expense coverage after a loss.

The most common commercial claim mistake is emotional trust without procedural protection.

Why policyholders need their own expert

Large commercial losses often turn on technical issues, not obvious ones. Was the cause of loss covered? Did water enter from a roof opening created by wind, or from deferred maintenance? Is equipment repair enough, or is replacement justified? Is downtime caused by physical damage, utility interruption, civil authority restrictions, or supply chain disruption?

Those aren't small questions. They decide the value of the claim.

A public adjuster organizes scope, documentation, pricing support, and presentation of the loss. In plain terms, your insurer has professionals reviewing your file. You need your own professional reviewing their work.

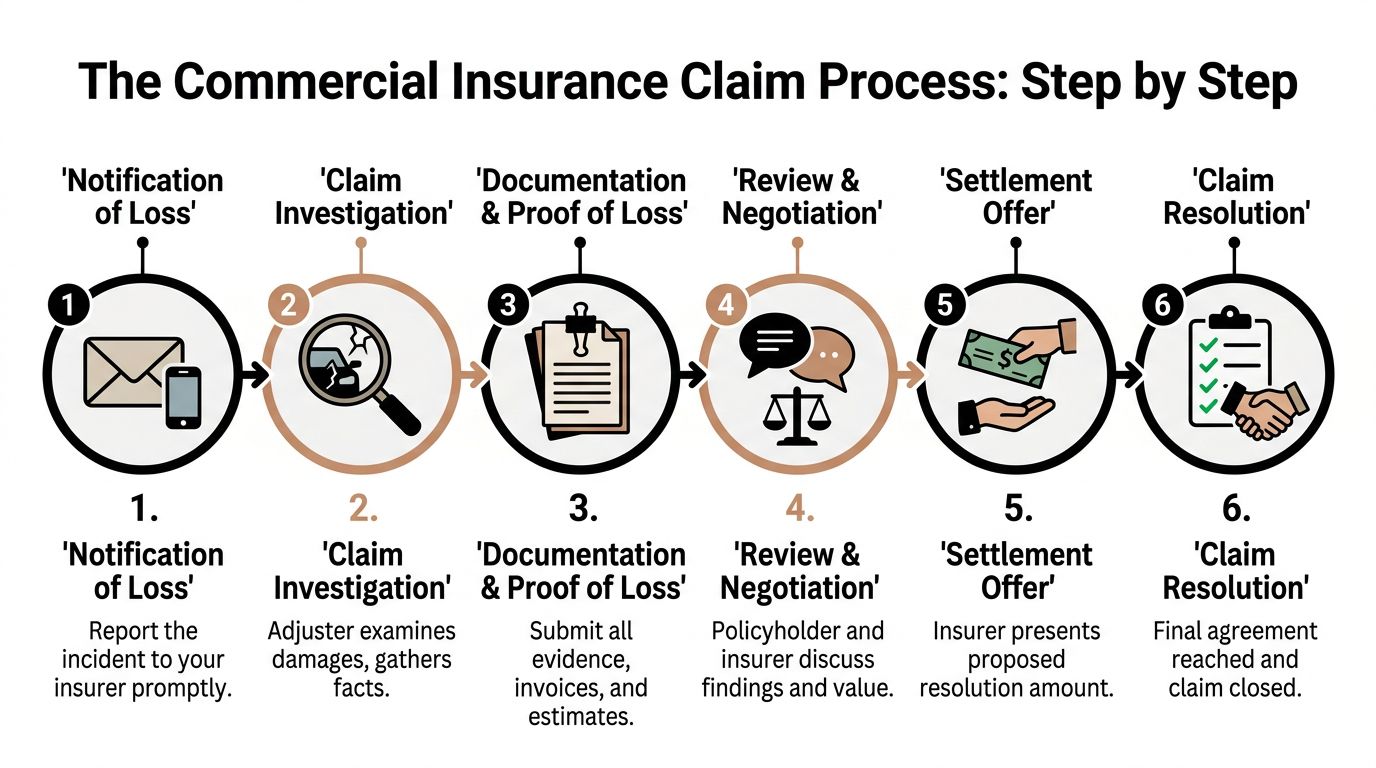

The Claim Process Step by Step

Claims feel messy because several tracks move at once. Emergency work starts. Inspections get scheduled. emails pile up. Meanwhile, your business still has to function.

Break the claim into six stages and you'll make better decisions.

Step 1 reporting and mitigation

Report the loss promptly, but keep the report factual and narrow. State what happened, when it was discovered, and what emergency steps you took. Don't speculate about hidden causes or offer a rough damage number unless you know it.

At the same time, protect the property. Dry-out, tarping, temporary power measures, security, and emergency cleanup may all be necessary. The key is separating emergency stabilization from full reconstruction commitments. If you need restoration support, understand what a commercial property restoration process should include before you sign broad work authorizations.

Step 2 inspection and causation

This stage drives the whole file. The insurer's investigation is not just about what got damaged. It's about why.

The adjuster is legally assigned to determine the proximate cause of the loss, which controls coverage, and then calculate the loss amount based on repair cost, estimates, and depreciation, as outlined in the commercial property insurance claim process document from UNESCAP.

That means your site inspection matters. Be present. Walk the adjuster through every affected area. Point out less obvious damage such as wet insulation, damaged wiring, warped doors, smoke migration, HVAC contamination, and interruption to tenant or customer areas.

Step 3 documentation and proof of loss

Now the claim gets built on paper.

You may be asked for estimates, invoices, photographs, maintenance records, contracts, leases, inventory records, payroll data, sales records, and a formal proof of loss. In fire and major property claims, detailed repair estimates often need to separate like-kind replacement from elective improvements. That's where owners get tripped up. They mix code-required work, upgrades they want, and covered restoration into one package.

Keep those categories separate. If you don't, the insurer will use the confusion against the whole submission.

Your file should tell a simple story. Covered event, resulting damage, necessary repair scope, documented financial impact.

Step 4 insurer valuation

At this stage, many business owners lose patience and accept shortcuts.

The carrier creates its scope and pricing. Sometimes that estimate is decent. Sometimes it misses line items, undermeasures, applies heavy depreciation, omits overhead and profit where justified, or treats legitimate replacement items as repairable. For business income, the insurer may narrow the restoration period or challenge causation for lost revenue.

A quick comparison helps:

| Issue | Insurer view | Policyholder concern |

|---|---|---|

| Scope | Limit repairs to visible damage | Include concealed and consequential damage |

| Pricing | Use insurer estimating assumptions | Test pricing against actual local bids |

| Depreciation | Apply reductions broadly | Challenge unsupported depreciation |

| Downtime | Shorten restoration timeline | Match timeline to real operational recovery |

Step 5 negotiation

Negotiation starts when you can show why the insurer's position is incomplete.

That means you need contractor estimates that describe the work, photographs tied to locations, equipment evaluations, inventory support, and clean business income calculations. Complaining isn't negotiation. Documentation is negotiation.

Use written rebuttals. If the adjuster's estimate is missing drywall behind millwork, code-required electrical work, or tenant improvement components that must be removed and reset, show exactly where and why.

Step 6 settlement and release

Before you accept payment, confirm what the payment covers. Is it building only? Does it include contents? Is business income still open? Are depreciation holdbacks recoverable after work is completed? Does cashing the check close any part of the file?

Those details matter more than the first number on the check.

A partial payment can help your cash flow. It can also create confusion if you assume the claim is fully valued when it isn't. Read every letter carefully before treating a payment as final.

Common Claim Pitfalls and How to Avoid Them

Most underpaid claims don't collapse because of one dramatic denial. They get trimmed, delayed, narrowed, and negotiated down until the owner is too tired to keep pushing.

That's why you need to recognize the usual tactics early.

Pitfall one accepting the first offer

A first offer is often a positioning move.

According to the Minnesota House document on claim settlement disputes, approximately 65% of commercial property claims receive initial settlement offers that are 30 to 50% below the actual loss value. The same source says a 2025 study found that businesses hiring independent adjusters secured settlements 22% higher than those who self-negotiated.

Whether you call that shocking or predictable, the practical takeaway is the same. Don't treat the first number as the actual number.

Ask for the full estimate. Review line items. Compare measurements. Check whether demolition, debris handling, code items, professional fees, and reset work were omitted.

Pitfall two letting delay drain your leverage

Delay helps the side with better cash reserves. That's usually not the business owner.

Insurers may ask for repeated document submissions, change adjusters mid-file, wait on consultants, or keep parts of the claim under review while your operation burns through cash. Some delays are legitimate. Many are part of claim friction.

Your response should be disciplined:

- Confirm every request in writing: Summarize calls by email.

- Set response dates: Ask when coverage, scope, and payment decisions will be issued.

- Track every submission: Keep a dated production log.

- Separate open issues: Don't let a dispute over one item freeze the whole claim.

If a carrier asks for the same records twice, send them again, note the prior submission date, and ask what unresolved question those records are supposed to answer.

Pitfall three surrendering the policy language fight

A lot of owners give up the moment the insurer cites an exclusion. That's a mistake.

Policy language is often where commercial claims are won or lost. Terms interact. Endorsements modify base forms. Definitions matter. A denial letter may sound final while resting on a narrow reading of a provision that can be challenged by context, competing terms, or the actual facts of loss.

Use this framework when policy language becomes the battleground:

| Insurer position | Your counter-move |

|---|---|

| Exclusion cited broadly | Ask how the carrier reconciles that exclusion with grant-of-coverage language and endorsements |

| Cause disputed | Gather expert opinions, photos, maintenance records, and timeline evidence |

| Part of the loss denied | Split covered and disputed components instead of abandoning the whole claim |

| Low valuation framed as final | Demand itemized support and rebut line by line |

What to do instead

Push for specifics. Ask where the policy says the carrier can take the position it's taking. Ask which facts support its conclusion. Ask what evidence would change that decision.

That's how professionals handle a commercial insurance claim. You don't need to be hostile. You need to be precise.

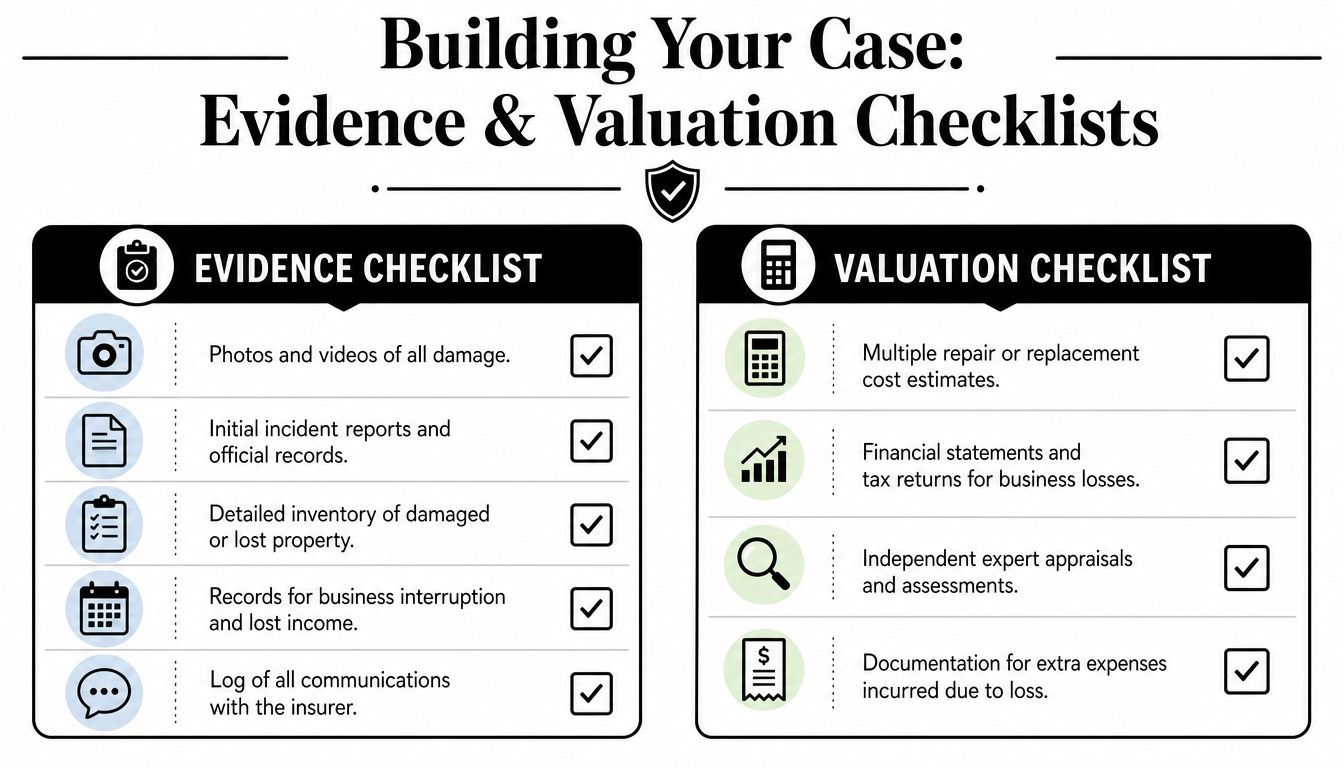

Building Your Case Evidence and Valuation Checklists

Strong claims are built, not hoped into existence.

The first mandated step in a commercial claim is to stabilize the incident and protect evidence, including systems, logs, emails, and financial impact details, because those records form the basis of the insurer's required claim package, as noted in Vouch's business insurance claims guidance.

Evidence checklist

Start with proof of what happened and what changed after the loss.

- Scene images: Take wide shots, room shots, and close-ups before demolition or heavy cleanup.

- Material retention: Keep samples of damaged flooring, roofing, equipment parts, packaging, or burned contents when practical.

- Incident records: Save alarm reports, fire reports, leak discovery logs, security reports, and maintenance tickets.

- Communication archive: Preserve emails, texts, meeting notes, tenant notices, and customer notifications tied to the event.

- Operational timeline: Record when damage was discovered, when the business paused, and when each area became unusable.

- Vendor paperwork: Store emergency mitigation contracts, drying logs, moisture maps, and daily site reports.

If the loss affected technology, don't overlook system evidence. Server logs, vendor alerts, surveillance exports, and access control history can help prove timing and extent.

Valuation checklist

Evidence proves the event. Valuation proves the money.

For most businesses, the file's strength or weakness is decided at this stage. Your numbers need support that an outsider can follow without guessing.

- Repair scope estimates: Get detailed estimates that describe demolition, repair, replacement, finish levels, and specialty trades.

- Contents inventory: List damaged furniture, equipment, stock, tools, supplies, and tenant improvements with model or purchase detail when available.

- Income loss support: Pull monthly financial statements, sales records, payroll reports, contracts, bookings, and seasonal comparison data.

- Extra expense records: Track temporary relocation, rental equipment, expedited shipping, overtime, and workaround costs.

- Expert opinions: Use engineers, electricians, hygienists, contractors, equipment vendors, or accountants where the claim turns technical.

- Depreciation challenges: Request support when the insurer applies depreciation aggressively or inconsistently.

For business income and extra expense issues, forensic accounting often decides the outcome. A service like forensic accounting for insurance claims can help translate downtime into a documented loss model the carrier has to address.

A messy file invites assumptions. A documented file forces decisions.

One file one chronology

Don't scatter documents across inboxes, text threads, and vendor portals. Build one claim file with folders for coverage letters, estimates, photos, invoices, business records, and correspondence. Add a running chronology with dates, who said what, and what remains open.

That chronology becomes powerful when the carrier changes positions or delays a response. It also helps your contractor, accountant, or adjuster step in without losing weeks reconstructing the history.

Timelines Deadlines and When to Hire an Expert

Claims stall for two reasons. The file is incomplete, or the issues are contested. In both cases, time starts working against the policyholder.

That matters even more when the dispute isn't about obvious physical damage but about what the policy means.

Policy disputes are where owners get outmatched

According to Atlas Insurance on denied commercial claims, up to 72% of commercial claim denials are rooted in disputes over policy language interpretation, and only 18% of these denials are successfully appealed.

Those numbers tell a blunt story. Business owners often lose not because the loss isn't real, but because they don't know how to frame the argument. They don't know which endorsement modifies which exclusion. They don't know how to challenge the carrier's reading of proximate cause, covered peril, vacancy, protective safeguards, or ensuing loss language.

If your claim has moved into that territory, this is no longer a basic paperwork issue.

When hiring an expert makes sense

You don't need outside help for every file. You do need it when the consequences of getting the claim wrong are serious.

Hire a public adjuster when one or more of these conditions exist:

- Major structural damage: Fire, water, storm, collapse, contamination, or complex equipment loss.

- Business interruption exposure: Revenue loss, tenant loss, event cancellations, or operational slowdown.

- Coverage friction: Reservation of rights letters, partial denials, exclusion disputes, or repeated document requests without clear decisions.

- Valuation conflict: Scope gaps, heavy depreciation, low pricing, or low first offers.

- Multi-party complexity: Landlord and tenant issues, nonprofit board oversight, lender involvement, or municipal reporting requirements.

In Oregon and Washington, it also matters that you work with someone properly licensed for public adjusting in the state where the claim is being handled. That's not a technicality. Licensing exists because adjusters handling claims for policyholders take on regulated duties.

What a public adjuster actually does

A good public adjuster doesn't just argue. They assemble.

They review the policy, inspect the loss, document the scope, gather bids, organize the proof package, rebut the insurer's estimate, and negotiate payment categories. Some firms also coordinate with accountants, engineers, and restoration vendors so the claim has technical support where needed.

If you're weighing timing, use a clear threshold: hire help when the claim is large enough, technical enough, or disputed enough that a mistake will cost more than the professional fee. If you want a practical benchmark for that decision, review guidance on when to hire a public adjuster.

This is the one place I'll name a firm directly. NW Claims Management is a licensed public adjusting firm serving Oregon and Washington that handles commercial, nonprofit, and property damage claims on behalf of policyholders, not insurers. That's the relevant distinction.

If the insurer has already framed the story of your loss and you're reacting instead of leading, you've waited too long.

Oregon and Washington owners should move early

For businesses in Portland, Seattle, Tacoma, Vancouver, Eugene, Salem, Spokane, and surrounding areas, geography changes the causes of loss but not the claim dynamic. Water, wind, fire, freeze events, and vandalism all create the same pressure points: site stabilization, causation analysis, valuation disputes, and lost operations.

The earlier you bring in expertise, the easier it is to preserve evidence, direct the investigation, and avoid statements or contracts that box you in later.

Sample Case Outcomes Real World Results

The pressure on commercial claims isn't easing. In 2024, global insured catastrophe losses hit $140 billion, the third-highest total since 1980, according to Talli's catastrophe loss statistics. That matters to business owners because more severe events mean more claim volume, more adjuster workload, and more opportunities for your file to be pushed through a formula instead of evaluated carefully.

Here are three situations that mirror what I see in the field. These are illustrative examples, not attributed case studies.

Restaurant fire with partial shutdown

A restaurant has a kitchen fire. The visible burn area is limited, so the insurer initially focuses on direct fire damage near the cooking line. The owner is relieved because the building didn't burn to the ground.

The problem appears later. Smoke traveled through the dining area and HVAC system. Electrical components near the suppression event are compromised. Portions of the ceiling, insulation, finishes, and ductwork need more than spot cleaning. The business also loses revenue because reopening in phases doesn't restore normal table volume.

The turning point in a claim like this is scope discipline. Someone has to separate emergency cleanup from full remediation, document smoke migration, support equipment evaluations, and build a business income presentation tied to the actual interruption period. Without that, the insurer keeps the file narrow.

Retail store flood with inventory dispute

A retailer takes on water after a severe weather event. Floors, base cabinets, display fixtures, and low-level stock are affected. The carrier agrees there is covered damage but questions the extent of contents loss and tries to limit replacement on items it believes can be cleaned or discounted for sale.

That dispute often becomes a documentation problem, not a moral one. The business needs inventory records, item descriptions, purchase history, photographs by location, and a rational salvage analysis. If the owner says "everything on the lower shelves is ruined," the insurer will push back. If the owner can show exactly what was exposed, for how long, and why the merchandise lost saleable condition, the negotiation changes.

Nonprofit building vandalism with delayed operations

A nonprofit office suffers vandalism, glass breakage, interior water damage, and damage to entry systems. The building owner repairs the obvious issues quickly, but the nonprofit also incurs staff disruption, temporary security costs, technology problems, and donor-facing event complications.

These claims get underestimated because organizations often focus on mission continuity instead of claim structure. They pay vendors, patch the building, move meetings, and only later realize the file should have included broader operational costs and a better-documented narrative of disruption.

The businesses that recover best are not the ones with the easiest losses. They're the ones that document early, separate categories of damage, and challenge incomplete valuations.

The pattern in all three examples is the same. The first version of the claim is rarely the final, accurate version. Commercial losses become fair settlements only when someone is actively proving the full story.

Frequently Asked Questions About Commercial Claims

Can I start repairs before the claim is settled

Yes, but separate emergency mitigation from full permanent repair.

You should take reasonable steps to prevent further damage and protect the property. Waiting can make things worse and create another fight over avoidable damage. But before major rebuild work begins, document thoroughly, preserve samples when practical, and make sure the insurer has had a fair chance to inspect.

If you're moving fast, keep a tight paper trail with photos, daily logs, invoices, and contractor explanations for why immediate work was necessary.

What if the damage is close to my deductible

Don't assume a claim isn't worth filing just because the visible damage looks close to the deductible.

Commercial losses often expand after investigation. Hidden moisture, electrical impact, code-related work, cleanup costs, and operational effects can change the picture. Review the full exposure before making that call. The issue isn't whether the first walk-through looks modest. The issue is the documented total covered loss.

How long does an insurance company have to respond in Oregon or Washington

The exact answer depends on the claim facts, the policy, and applicable state rules. Don't rely on casual timelines from a call center.

What matters in practice is this: demand written acknowledgment, ask for written status updates, and keep a dated log of every submission and response. If the carrier is vague, ask what specific information is still needed to make a decision. If the answer stays fuzzy, the file may need outside pressure.

Will filing a commercial insurance claim increase my premium

It can affect underwriting at renewal, but that shouldn't drive your decision after a legitimate covered loss.

The bigger mistake is underreporting or mishandling a serious claim because you're worried about future pricing. Your first job is to protect the business today. Worry about renewal strategy after you've secured the benefits the policy was purchased to provide.

Should I use the insurer's contractor

Maybe, but don't assume you must.

Preferred vendors can be efficient. They can also create confusion about who the contractor is really listening to when scope or price becomes disputed. If you use any contractor, make sure you control the contract, understand the scope, and keep the right to challenge the insurer's valuation.

What if the insurer denies only part of my claim

Don't treat a partial denial like the end of the file.

A commercial insurance claim can contain covered and disputed components at the same time. Keep pushing the supported parts toward payment while you contest the denied portion. Owners often lose money because they assume one disputed item contaminates the whole claim. It doesn't have to.

Do I need a lawyer or a public adjuster

They do different jobs.

A public adjuster handles claim preparation, valuation, documentation, and negotiation. A lawyer is usually the better fit when the dispute has become legal, bad-faith focused, or headed toward litigation. Many business owners start with a public adjuster because the problem is still a claim problem, not yet a lawsuit problem.

What should I do today if my claim already feels off track

Do these five things immediately:

- Request the full claim file correspondence and estimate package.

- Create a chronology of every call, email, inspection, and payment.

- List every unresolved issue by category, such as building, contents, income, and extra expense.

- Gather missing support documents and label them clearly.

- Get professional review if the claim involves major money, denial language, or a low offer.

If your commercial insurance claim in Oregon or Washington is stalled, underpaid, or too complex to manage while running a business, NW Claims Management can review the loss, explain the policy issues, document damages, and negotiate on the policyholder's behalf. A clear claim strategy early usually costs less than cleaning up a weak file later.