The storm has passed, the fire is out, or the water has finally stopped moving through your building. You report the loss, expecting your insurance company to take over. Then a letter, email, or call comes from a company you don't recognize.

That throws people off immediately. It should.

If you're a homeowner, business owner, church, school, or nonprofit in Oregon or Washington, you need to know who just entered your claim and whose interests they serve. A lot of policyholders assume any company touching the claim must be there to help them recover. That's not a safe assumption.

Third party administrator companies can move paperwork, coordinate inspections, and manage claim flow. They can also add distance between you and the insurer that owes under the policy. That distinction matters most when the loss is serious and every delay, omission, or low estimate affects your rebuild.

A New Name in Your Mailbox Understanding the Rise of TPAs

A Portland homeowner has smoke damage in every room after a kitchen fire. A church in Vancouver has roof and water damage after a wind event. A small business in Eugene finds broken windows, soaked inventory, and a shutdown that starts bleeding cash the same day.

They file a claim with the insurer. Then the next communication comes from a company with a different name.

That moment creates confusion for a reason. You bought a policy from one company, but now another company is asking for documents, scheduling inspections, and controlling the pace of communication. Many policyholders think a mistake has been made. Typically, this is not the case.

Third party administrator companies are now a major part of insurance operations. The global insurance third-party administrator market was valued at $324.9 billion in 2022 and is projected to reach $795.1 billion by 2032, growing at a 9.6% CAGR. By 2026, the market is projected to reach $446.76 billion, according to Allied Market Research's insurance third-party administrator market analysis.

That growth tells you something important. Insurers increasingly outsource administrative work instead of handling every part of the claim with in-house staff.

Why you're seeing TPAs more often

Insurance companies use TPAs because they want scale, process control, and staffing flexibility. After wildfires, windstorms, freezes, and water losses, claim volume spikes. Outsourcing helps insurers absorb that surge.

For policyholders, that means:

- More handoffs: The person who answers the phone may not work for the insurer whose name is on the policy.

- More process: You may have to repeat facts, resend files, or work through layers before anyone makes a decision.

- Less clarity: It's easy to lose track of who has authority and who is just relaying instructions.

Practical rule: The moment a new company appears in your claim, ask who hired them, what authority they have, and whether they can approve scope, payment, and coverage positions.

That's where many people get trapped. They treat the TPA like a neutral claims guide when it's really part of the insurer's operating chain. If you're already seeing delays, partial information, or shifting explanations, review common insurance adjuster tricks early before the claim gets further away from the damage.

What Exactly Is a Third Party Administrator Company

A third party administrator company, or TPA, is an outside company hired to handle insurance-related administrative work for someone else. In property claims, that usually means the insurer hires the TPA.

The cleanest way to understand it is this. A TPA is like a property management company for an insurance company's paperwork and claim workflow. The owner still owns the building. The manager handles the day-to-day operations. In the same way, the insurer still issued the policy and still carries the financial obligation under that policy, but the TPA may handle much of the communication and claim administration.

What a TPA does

A TPA often steps into functions such as:

- Claim intake: Receiving the first notice of loss and opening the file.

- Document handling: Collecting estimates, invoices, photos, repair proposals, and proofs of loss.

- Communication management: Sending requests, status updates, reservation letters, and scheduling notices.

- Process coordination: Moving the file between field adjusters, reviewers, examiners, vendors, and internal decision-makers.

In some files, the TPA feels like the claim office. That's why policyholders often assume the TPA is the insurer. It isn't.

What a TPA doesn't do

A TPA is not the company that sold you the insurance policy. It usually doesn't underwrite the risk. It usually doesn't step into your shoes as an advocate. And it isn't there to maximize your recovery.

That's the critical point.

The TPA may be polite, organized, and responsive. None of that changes the basic alignment. It works on behalf of the party that hired it.

If you remember only one thing, remember this. A TPA administers your claim. It does not represent your interests.

That sounds harsh, but it keeps people from making a costly mistake. Too many policyholders overshare, accept narrow scopes too early, or assume the TPA will point out every benefit available under the policy. That's not a safe expectation.

Why insurers like the model

Insurers use TPAs because outsourcing lets them spread administrative work across outside specialists. That can be useful when claims volume rises or when the insurer wants a standardized process across multiple regions and claim types.

For you, though, the practical question isn't whether the model helps the insurer. The practical question is whether the model helps your claim.

If the answer is yes, you want clear communication, prompt inspections, complete scopes, and written explanations. If the answer is no, you need to stop assuming the process will correct itself.

Common TPA Services Affecting Your Property Claim

Not every TPA does the same work, but several service areas frequently appear. In property damage claims, those services affect how fast your file moves, what documents get emphasized, and how settlement discussions take shape.

Industry estimates suggest that TPA firms administer benefits for about 55% of all U.S. workers with non-federal health or pension benefits, and the U.S. TPA and claims adjusters market reached $335.8 billion in 2026, according to the SPBA overview of the size and role of TPAs in the marketplace. That same broad market includes major claims operators handling property, casualty, and workers' compensation.

Claims administration

This is the service property owners feel most directly.

A TPA handling claims administration may receive the first loss notice, assign a field adjuster, gather records, review estimates, request supporting proof, and relay settlement positions. If your home in Salem suffers major water damage after a pipe burst, the TPA may become the hub for nearly every document in the file.

That matters because claims administration shapes the record. The file usually reflects what gets documented, what gets priced, what gets challenged, and what gets left out.

Watch for these pressure points:

- Scope control: If the TPA narrows the damage scope early, later repair costs often become harder to recover.

- Documentation demands: Repeated requests can be legitimate, but they can also slow momentum when your property needs immediate work.

- Status bottlenecks: If one outside administrator controls updates, simple questions can take too long to answer.

A strong record starts with your own evidence. Before debris is cleared or contents are discarded, tools like a Home Inventory App for Insurance can help organize photos, room-by-room records, and ownership details that support valuation.

For serious structural losses, a detailed property damage assessment is often the difference between a rough estimate and a defensible claim file.

Workers' compensation overlap

Business owners often miss this until someone gets hurt during cleanup or restoration.

A TPA may also handle workers' compensation administration connected to your operations. If a maintenance employee slips during post-storm mitigation at your Tacoma warehouse, or a staff member is injured while moving wet inventory in a nonprofit facility, the same broader TPA ecosystem can touch both the property side and the injury side.

That overlap creates practical problems:

| Issue | Why it matters |

|---|---|

| Separate claim tracks | Property and injury files may move on different timelines |

| Different document requests | You may have to produce records for more than one administrator |

| Conflicting priorities | Fast cleanup decisions can collide with injury investigation needs |

Benefits administration for self-insured organizations

This service matters most to municipalities, school systems, large nonprofits, and self-insured entities. A TPA may handle employee benefit administration while also being part of the broader claims process after a property event disrupts operations.

For example, a nonprofit community center in Washington might be managing property repairs, temporary relocation, employee continuity, and claim communications at the same time. When a TPA sits in multiple administrative lanes, the organization needs tight internal control over records, authority, and deadlines.

The core lesson is simple. Third party administrator companies don't just "process paperwork." They shape the pace, completeness, and structure of claim handling in ways that directly affect your recovery.

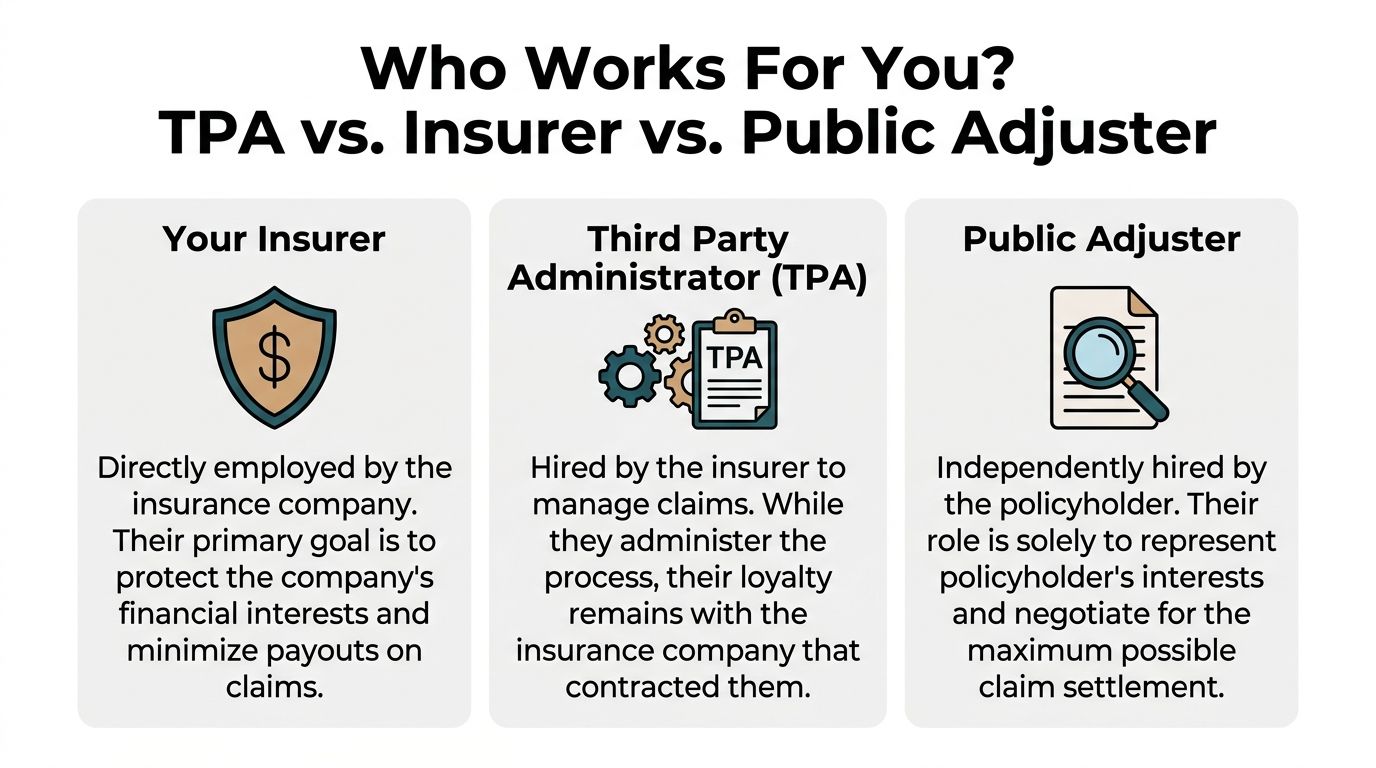

TPA vs Insurer vs Public Adjuster Who Works for You

This is often not explained clearly enough.

Titles confuse policyholders. "Adjuster," "administrator," "examiner," "consultant," "specialist." Those labels sound official, but they don't answer the only question that matters when money is on the line.

Who works for you?

Here is the short answer.

- The insurance company adjuster works for the insurance company.

- The third party administrator works for the insurance company that hired it.

- The public adjuster works for the policyholder.

That doesn't mean every insurer adjuster or TPA handler is dishonest. It means their duty runs in one direction, and it isn't toward increasing your settlement.

Allegiance: A Key Difference

In self-funded benefit plans, employers often struggle to monitor TPA spending because TPAs classify reimbursement methods and discounts as proprietary. That transparency problem matters because 63% of U.S. covered employees are in self-insured plans reliant on TPAs, according to Georgetown's analysis of third-party administrators in self-funded health insurance. The property world has its own version of that same problem. Policyholders often can't fully see how decisions are being framed, escalated, or constrained behind the scenes.

If you're dealing with a fire, flood, or storm loss, that lack of visibility can hurt you fast. You may hear that a payment decision is "under review" without knowing who is reviewing it, what standards they're using, or whether key damage items were omitted from the scope.

Side-by-side comparison

| Attribute | Third Party Administrator (TPA) | Insurance Company Adjuster | Public Adjuster |

|---|---|---|---|

| Who hires them | The insurer or plan sponsor | The insurer | The policyholder |

| Primary role | Administers claim process and related tasks | Investigates and adjusts the claim for the insurer | Represents the policyholder in the claim |

| Whose interests they protect | The party that contracted them | The insurance company | The insured property owner |

| Access to your claim file | Often substantial, but based on insurer authority | Direct through insurer systems | Built through documentation, advocacy, and negotiation |

| What you should expect | Process management, requests, coordination | Coverage review, scope decisions, settlement positions | Claim preparation, valuation, negotiation support |

| Best question to ask | "What authority do you have on my file?" | "What is your basis for this decision?" | "How will you document and present my loss?" |

Why this matters in water and storm claims

Water claims expose the difference fast. Coverage depends on cause, timing, exclusions, mitigation, and damage classification. If you're trying to sort out whether a specific loss may fall under your policy, practical background reading on water damage covered by homeowners insurance can help you frame the right questions before you accept a quick answer from the claim side.

The same issue comes up in storm losses with roof, siding, interior water, and business interruption questions layered together. A TPA may keep the file moving, but it won't build your claim for you.

Ask every claim contact one direct question: "Are you representing my interests, or the insurer's interests?" The answer may be polite, but it won't be ambiguous.

If you want a sharper breakdown of that divide, compare the roles in this guide to public adjuster vs insurance adjuster. The names sound similar. Their obligations are not.

The Pros and Cons of a TPA Handling Your Claim

Insurers often present TPAs as a practical solution. Sometimes they are. But you shouldn't grade the arrangement by whether it helps the insurer's workflow. You should grade it by whether it helps you recover fully and on time.

The upside

The best argument for a TPA is efficiency.

A capable administrator can keep documents organized, route tasks quickly, line up inspections, and prevent a claim from sitting untouched. If the file is straightforward and the damage is well documented, an organized TPA may help maintain momentum.

Possible benefits include:

- Clear intake procedures: You know where to send estimates, invoices, photos, and forms.

- Centralized communication: One hub can be easier than chasing multiple departments.

- Operational consistency: A process-driven handler may reduce random delays on routine items.

That said, policyholders hear "efficient" and assume "fair." Those aren't the same thing.

The downside

The downside is where most serious property claims run into trouble.

A TPA can create another layer between you and the insurer's actual decision-makers. That means slower answers, repeated requests, and more opportunities for pieces of your loss to disappear into administrative gaps.

Common problems include:

- Communication drift: You ask a direct question and get a process update instead of an answer.

- Incomplete scope review: The file moves forward before all damage is properly documented.

- Speed over accuracy: The claim closes faster, but not necessarily correctly.

- Conflicted incentives: The TPA's business relationship is with the insurer, not with you.

- Bureaucratic fatigue: Policyholders get worn down and accept less just to move on.

A fast underpaid claim is still an underpaid claim.

That's the trap. Many people focus on turnaround time because they're under pressure to rebuild, reopen, or relocate. Insurers know that. TPAs know that. If speed becomes the headline, accuracy can become the casualty.

Red flags you shouldn't ignore

When a TPA is hurting your file, the signs are usually visible:

- The contact person changes repeatedly. Nobody owns the claim long enough to answer hard questions.

- Requests multiply without explanation. You keep sending material but don't see meaningful progress.

- Verbal statements don't turn into written positions. That's a problem.

- The scope feels thin. Obvious damage, code issues, contents, or business losses are missing.

- You feel rushed to accept. Pressure often shows up before the claim has been fully valued.

If you're weighing representation, cost matters too. A lot of policyholders delay help because they assume they can't afford it, but the fee structure is often more straightforward than people expect. Learn the basics before you decide by reviewing public adjuster cost.

My opinion is simple. TPAs are fine for administration. They are not a substitute for policyholder advocacy.

A Checklist for Choosing a Third Party Administrator

Most homeowners won't choose the TPA on a personal property claim. Commercial owners, municipalities, schools, and nonprofits often do. If your organization is self-insured or plays a direct role in selecting claims administration partners, don't treat that decision like routine vendor procurement.

Choose the wrong TPA and you buy yourself confusion. Choose the right one and you at least keep your systems, reporting, and claim controls intact.

Start with measurable handling standards

Top-performing TPAs achieve claims turnaround times of 3 to 5 business days for 90% of clean claims, while laggards can take 10+ days. High-renewal TPAs also maintain accuracy rates above 97% and strong cybersecurity such as SOC 2 Type II compliance, according to ACS Benefit Services on key TPA performance indicators.

Those numbers come from a benefits context, but the decision principle applies broadly. Don't hire a TPA based on slide decks and sales language. Hire based on standards you can audit.

Your screening checklist

Use this list before signing anything.

Licensing and regulatory standing

Confirm the company is properly licensed where required and can operate cleanly in Oregon, Washington, or any state tied to your claim footprint.Claim authority in writing

Ask exactly what authority the TPA has. Can it approve payments, deny portions of claims, assign vendors, or only administer workflow?Technology you can use

If the platform is clunky, your team will suffer. You want document tracking, status visibility, audit trails, and secure file exchange.Cybersecurity controls

Ask about SOC 2 Type II and how claim data is stored, accessed, and retained. Sensitive property records, financials, and internal reports shouldn't float around by email without safeguards.Reporting transparency

Require regular claim reports that show status, reserves if applicable, open issues, aging, and pending decisions. If a TPA says key methods are proprietary, push harder.Dispute escalation path

Find out who resolves conflicts when scope, timing, or payment disagreements arise. Vague escalation paths become expensive later.

Questions that expose weak vendors

A strong TPA should answer these without dodging:

| Question | What a good answer sounds like |

|---|---|

| How do you track file aging? | Specific status categories and reporting cadence |

| Who can see our claim data? | Role-based access with documented controls |

| How do you handle large-loss surge volume? | Clear staffing and escalation plan |

| What happens when we dispute a claim decision? | Named escalation process, not generalities |

Ask this early: "What will we be able to see without asking for permission each time?"

That question gets to the heart of the relationship. If your organization bears the financial risk, you need direct visibility. Not curated visibility. Not delayed visibility. Direct visibility.

One more hard recommendation

Don't choose solely on price.

A cheap TPA can cost far more than it saves if claim handling is sloppy, communication breaks down, or oversight is weak. Administrative savings disappear fast when losses are under-scoped, decisions are delayed, or your staff spends months chasing answers.

Your Rights Interacting with TPAs in Oregon and Washington

If your property is in Oregon or Washington, you are not stuck because a TPA is involved. You still have rights around fair claim handling, communication, and complaint processes. The exact legal details depend on the claim and policy, but the big mistake is assuming an outside administrator puts the claim beyond regulatory oversight.

It doesn't.

What you should insist on

Whether the file is handled directly by an insurer employee or by a TPA, you should expect:

- Timely communication: Not endless silence while your property sits damaged.

- Written explanations: Especially when the claim is delayed, limited, or disputed.

- A fair opportunity to provide support: Estimates, expert reports, invoices, inventories, photos, and repair documentation should be considered.

- Professional handling: You should not have to guess who is responsible for the next step.

In Oregon, the Division of Financial Regulation handles insurance consumer issues. In Washington, the Office of the Insurance Commissioner handles complaints and oversight. If a TPA is participating in improper claim handling on behalf of an insurer, those state channels matter.

The digital problem growing in the Northwest

The insurance TPA market is expanding as digitalization and product complexity increase, but that shift raises concerns for property owners. Recent reporting notes that the use of AI in claims assessment is growing after recent storms, and the impact on claim accuracy and client control remains an unaddressed issue, especially for property owners in Oregon and Washington, according to this market report discussing digitalization and TPA trends.

That issue is not theoretical.

If a roof claim, moisture mapping issue, or structural damage estimate gets filtered through automated tools before a human fully examines the loss, your claim can get framed too narrowly from the start. Once that happens, every later discussion starts from a bad foundation.

Practical steps when a TPA is mishandling your file

Take control early.

- Move key requests into writing. Email is better than phone calls for disputed issues.

- Ask for names and roles. Know whether you're speaking to a TPA representative, insurer adjuster, engineer, or vendor.

- Request the basis for decisions. If damage is excluded, limited, or delayed, ask for the policy basis and factual basis.

- Keep your own timeline. Log inspections, calls, promises, and missing follow-up.

- Escalate when necessary. If the file stalls or the explanation doesn't hold up, push the issue higher.

- Use formal complaint channels if needed. Oregon and Washington regulators exist for a reason.

When a claim handler won't state a position clearly in writing, this often signals a need to slow down and document everything.

If your claim has already slid into denial, partial denial, or endless delay, don't wait for the process to fix itself. Read how to fight insurance claim denial and start building your response with evidence, chronology, and policy language in mind.

Local policyholders need local discipline

Oregon and Washington losses often involve wind-driven rain, wildfire smoke, freezing events, roof failure, drainage problems, and cleanup timing disputes. Those files can turn technical fast.

A TPA may treat your claim like one more file in a regional queue. You can't afford to do the same. Your home, business, school, or nonprofit property is not a queue item. It's your asset, your operations, and sometimes your ability to stay open.

Frequently Asked Questions About Third Party Administrators

Can a TPA deny my property claim

A TPA may communicate a denial position or administer the process around a denial, but the key issue is authority. Ask who made the decision, on what policy basis, and whether the insurer adopted that decision. Don't accept a vague answer.

Do I have to deal with the TPA

If the insurer assigned a TPA, interaction during the claim process is typically required. That said, you do not have to treat every request as unquestionable. You can ask for written explanations, authority, deadlines, and decision bases.

Is a TPA the same as an insurance adjuster

No. A TPA is an outside administrator. An insurance adjuster may be an employee adjuster or an independent adjuster handling claim investigation and adjustment work. In practice, the distinction can blur for policyholders because both may contact you on the insurer's side of the claim.

Are third party administrator companies bad

Not automatically.

Some are organized and responsive. The problem isn't their existence. The problem is misunderstanding their role. If you think a TPA is there to advocate for you, you diminish your negotiating position.

Should homeowners worry when a TPA gets assigned

You should pay attention, not panic.

A TPA assignment means more process and another layer in the file. That's manageable if you keep records, insist on written communication, and don't let an incomplete damage scope harden into the insurer's final position.

What should business owners and nonprofits do differently

Treat the claim like a major financial event, not a routine repair matter. Separate emergency mitigation from final scope decisions, preserve all invoices, track operational disruption, and designate one internal contact to control communication.

When should I get outside help

Get outside help when the damage is serious, the scope is disputed, the claim is delayed, the offer feels thin, or the communication has become circular. Those are the moments when policyholders lose ground fastest.

What's the biggest mistake people make with TPAs

They relax because the process sounds professional.

Professional language doesn't equal aligned interests. Stay polite, stay organized, and verify everything that affects coverage, scope, timing, and payment.

If you're dealing with a fire, water, storm, vandalism, or other property loss in Oregon or Washington and the claim feels confusing, stalled, or undervalued, talk to NW Claims Management. They represent policyholders, not insurers, and help homeowners, businesses, municipalities, and nonprofits document damage, interpret policy language, and pursue a fair settlement.