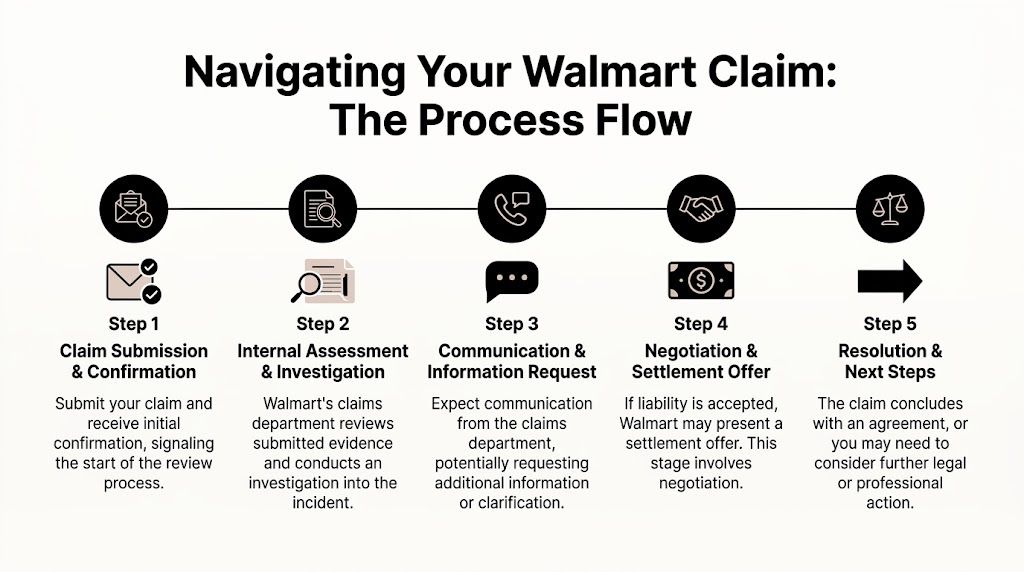

You’re probably reading this after a bad hour. Maybe you slipped on a wet aisle, your car was hit in a Walmart parking lot, or store activity damaged property you now have to repair. You reported it. Someone took notes. Then the uncertainty started.

Individuals often assume they’re dealing with store customer service. They aren’t. A claim against Walmart quickly becomes a documentation fight, a communication test, and a negotiation with a highly structured claims operation. If you live in Oregon or Washington, that matters even more because property owners here often try to be reasonable first, and large claims departments are built to take advantage of that instinct.

A fair result usually doesn’t come from being loud. It comes from being organized, careful, and hard to corner.

Understanding Your Opponent The Walmart Claims Department

A lot of claimants first notice the problem at the store level. A manager is polite. An incident report gets started. It feels routine. Then the file leaves the store and enters a different system.

Walmart handles a huge volume of liability matters. According to Miller & Zois on Walmart injury settlements, lawsuits are filed against Walmart nearly 20 times daily, totaling close to 5,000 each year. To manage that volume, Walmart created Claims Management, Inc. (CMI), which functions as its own internal adjuster. The same source explains that Walmart’s self-insured model lets it process, value, and settle claims internally, and that liability costs later surged enough to produce a surprise expense of about $400 million above expectations in one fiscal second quarter.

That tells you something important. The walmart claims department isn’t an afterthought. It is a system built for scale.

Why that changes how you should act

When a company sees claims in that volume, every early conversation matters. Every photo matters. Every offhand comment matters. What feels like a simple reimbursement request to you may be treated as a file that needs to be contained, categorized, and valued with Walmart’s broader cost controls in mind.

For Oregon and Washington property owners, that means you should think like a record keeper, not just an injured customer or frustrated shopper.

- Treat the first report as evidence creation: If the store generates an incident report, make sure your description is factual and concise.

- Assume the next contact is strategic: Once CMI is involved, the focus shifts from customer service to liability management.

- Expect the file to be segmented: Property damage, bodily injury, witness statements, and supporting records may all be handled with different levels of urgency.

Practical rule: Don’t mistake a smooth intake process for claim acceptance.

There’s also a security angle many claimants overlook. If your incident involved poor parking lot visibility, access control gaps, or weak on-site deterrence, it helps to understand how retail risk prevention is supposed to work. This complete guide to retail security services gives useful context for evaluating whether a store environment was being managed responsibly.

The mindset that works

People hurt their claims when they approach Walmart casually. They assume good faith, fill gaps from memory, and speak before they’ve organized facts. A better approach is slower and cleaner. Document first. Speak second. Submit only what supports your account.

If you’re trying to recognize pressure tactics early, this breakdown of insurance adjuster tricks is worth reading before you return a call.

Your First Hour After an Incident Essential Evidence Gathering

The strongest evidence often exists before anyone from claims calls you. That first hour matters because scenes change fast. Spills get cleaned. carts move. employees rotate. footage gets harder to identify unless the timeline is clear.

What to capture before you leave

Use your phone and be methodical. Don’t just take one close-up photo of the hazard. Build a sequence.

- Start wide: Photograph the whole area so the hazard is tied to the aisle, entrance, checkout lane, curb, or parking row.

- Move closer: Capture the specific condition. Water, debris, broken pavement, loose merchandise, a damaged cart, or impact to your vehicle.

- Look for warnings: Take photos that show whether cones, wet-floor signs, barricades, or caution tape were present or absent.

- Record timing: Screenshot the current time on your phone and keep receipts, transaction logs, or parking timestamps.

If you were physically hurt, photograph visible injuries as they develop. Bruising and swelling often look different later than they do immediately after an incident.

Names beat memories

You don’t need a formal witness statement in the parking lot. You do need names and contact details.

Collect these if you can:

- Witness contact information: Name, phone, and a short note on what they saw.

- Employee identifiers: First name, badge name, department, or any description that helps locate them later.

- Manager involvement: Ask who took the report and write down when that happened.

Write down exact phrases you heard. If an employee says, “That spill was already there,” or “We called someone to clean it,” preserve the wording as closely as you can.

Report it, but keep your wording tight

You should report the incident to store management so a record exists. Keep your language factual. State what happened, where it happened, and what damage or symptoms you noticed. Don’t guess about cause if you don’t know it yet, and don’t soften the event by saying you’re “probably fine” when you’re still in shock.

A simple version is enough:

I slipped near the refrigerated aisle at about this time. The floor was wet. I’m reporting the incident and want a copy or reference number for the store report.

If the damage is to property rather than your body, use the same discipline. Identify the object, the location, and the visible damage.

Preserve what Walmart may not hand over easily

Surveillance footage can become a major issue later. Your job in the first hour is to make it easier to locate.

Create a note with:

| Item | What to record |

|---|---|

| Exact location | Aisle number, entrance area, register, parking row, cart bay |

| Time window | Approximate minute the incident occurred |

| Nearby landmarks | Endcap display, pharmacy, service desk, garden center |

| Employees present | Names or descriptions |

If the loss involves building materials, fixtures, contents, or another property component, a professional property damage assessment helps translate raw evidence into a supportable claim file later.

Initiating Contact With Walmart Claims

Once you’ve stabilized the situation and gathered your initial evidence, the next step is formal notice. At this stage, many valid claims often weaken, not because the underlying event changed, but because the first conversation handed over too much.

Your goal is simple. Report the claim without giving Walmart language it can use against you later.

What to have ready before you call

Don’t contact the walmart claims department from memory alone. Put the essentials in front of you first.

Have these ready:

- Incident basics: Date, time, location, and store identification if you have it

- Damage summary: Injury, vehicle damage, personal property damage, or another loss category

- Your supporting file: Photos, witness names, store report details, receipts, and timeline notes

- A written script: Short enough that you won’t drift into speculation

A clean opening usually sounds like this:

I’m calling to report an incident at a Walmart location. It occurred on [date] at approximately [time]. I’m providing notice of the claim and can supply supporting documentation.

That’s enough to start.

What not to say

Don’t volunteer conclusions. Don’t fill silence. Don’t explain what you “might have done differently.” Claims staff are trained listeners.

According to The Injury Lawyers on Walmart slip and fall settlements, CMI trains representatives to seek recorded statements that can draw out admissions of fault, such as a claimant saying they were “rushing.” The same source says this tactic can support comparative negligence arguments that reduce awards by 5-50%, and advises against giving a recorded statement without legal counsel.

That means casual wording matters.

Avoid statements like these:

- “I wasn’t really paying attention.”

- “I’m sure it was partly my fault.”

- “I think I’m okay.”

- “I don’t need much.”

Each one can shrink the claim before it’s even documented.

How to decline a recorded statement

This is the most important communication choice in the early phase. You can cooperate without agreeing to a recorded interview.

Use plain language:

- Polite version: I’m willing to provide factual information in writing, but I’m not giving a recorded statement at this time.

- If they push: I’m preserving the accuracy of the claim and will respond after I’ve reviewed my documentation.

- If they imply it’s required: Please note my claim has been reported. I’ll provide supporting materials through the proper channel.

You do not need to sound defensive. You need to sound controlled.

Keep notes on every interaction. Record the date, the representative’s name, what was requested, and what you provided. A phone log becomes useful when the file later shifts in tone or someone claims you failed to cooperate.

If you need a practical framework for formal notice, this guide on how to file a property damage claim lays out the kind of structure that keeps early reporting from turning into an avoidable mistake.

Building Your Bulletproof Claim Package

A claim gets stronger when it stops looking like a complaint and starts reading like a file that can survive scrutiny. That’s the standard you want. Organized, complete, and easy to verify.

Why completeness matters

Incomplete submissions invite delay. Disorganized submissions invite denial. For reimbursement matters, Riverbend Consulting’s analysis of Walmart reimbursement appeals states that up to 60% of initial claims can be denied due to discrepancies or incomplete submissions, and that a thorough evidence package can reverse 75-90% of denials when handled correctly.

Even if your situation isn’t a vendor reimbursement file, the lesson still applies. Claims handlers exploit gaps.

What belongs in the package

Think in categories, not piles. Every document should answer one of four questions: what happened, where it happened, what it caused, and what it cost.

Incident proof

This section anchors the event itself.

Include:

- Store incident report details: Report number, manager name, date, and location

- Scene photos and video: Wide shots first, then close-ups

- Witness list: Names, numbers, and short summaries

- Timeline memo: A one-page chronology written by you while memory is fresh

Damage proof

This section shows the consequence.

For injury claims, that may include treatment records, bills, prescriptions, and work absence records. For property losses, it may include repair invoices, replacement quotes, receipts, photographs of damaged items, and documentation showing condition before the incident if you have it.

Ownership and value proof

Many people falter at this stage. If Walmart damages your phone, glasses, car panel, merchandise, or other personal property, don’t just state the item existed. Prove it.

Useful records include:

| Category | Strong supporting records |

|---|---|

| Vehicle damage | Repair estimate, photos, registration, prior condition photos if available |

| Personal property | Purchase receipt, card statement, model information, serial number photos |

| Business property | Inventory record, vendor invoice, replacement quote, internal asset list |

Demand support

You don’t need a dramatic letter. You need a coherent one.

Claim file standard: If a stranger opened your packet, they should understand the loss without calling you for basic clarification.

Your written submission should identify the incident, summarize the damage, list enclosed records, and state what reimbursement or compensation you’re requesting. Keep the tone professional. Don’t overargue liability in the first package if the documents already show it.

What doesn’t work

These mistakes weaken otherwise good claims:

- Mixed files: Sending photos in one email, receipts by text, and medical records later without labels

- Unlabeled attachments: File names like “IMG_4472” instead of “Aisle_Floor_Condition_1”

- Inflated asks: Claiming unsupported amounts damages credibility

- Gaps in chronology: Missing treatment, repair, or reporting dates invite questions

If you want a stronger framework for organizing values and proof, this resource on how to maximize insurance claim payout is useful because it focuses on documentation discipline, not bluster.

Navigating The Process What to Expect After You File

After submission, the file usually enters a quieter phase. That silence causes a lot of claimants to panic and start talking too much. Resist that urge. Once the walmart claims department has your materials, it begins assessing what it can verify, what it can challenge, and what pressure points exist in your situation.

The shift many claimants notice

Early communication can feel reassuring. A representative sounds sympathetic, asks for documents, and gives the impression that progress is being made. Then the tone changes.

As described by Kaplun Marx on CMI and Walmart slip and fall claims, claimants frequently report that CMI representatives seem caring at first, then become hostile or unresponsive after gathering records. That source describes a “free look” strategy, where the representative collects information to build a defensive file before communication slows or stalls.

That pattern matters because it keeps people chasing approval instead of evaluating the file realistically.

What the process usually feels like

The formal stages are simple on paper. The lived experience is less tidy.

| Stage | What you may see | What to do |

|---|---|---|

| Acknowledgment | Claim number, intake questions, request for basic records | Confirm details in writing |

| Review | Follow-up requests, long pauses, repeated clarification questions | Respond with labeled documents only |

| Evaluation | Liability appears uncertain, damages get questioned | Point back to records, not emotion |

| Negotiation | Low initial offer or partial denial | Counter with organized support |

| Resolution | Settlement, denial, or need for escalation | Decide based on file strength |

Tactics that wear people down

Not every frustrating moment is malicious. Some are just bureaucracy. But large claims systems also know delay creates advantage.

Common pressure points include:

- Repeated requests for the same records: This tests whether your file tracking is weak.

- Narrow questions about prior condition: These can be used to separate the incident from the damage.

- Fragmented communication: One person handles intake, another reviews documents, another makes an offer.

- Silence after cooperation: This often pushes claimants to soften their position just to restart dialogue.

Don’t measure progress by friendliness. Measure it by what has been confirmed in writing.

How to stay in control

The best response is procedural, not emotional.

Set a communication routine. Reply in writing whenever possible. Number your attachments. Keep one master chronology. If they ask for something you already sent, resend it with the original date noted.

Use short follow-ups such as:

Attached again is the document package previously provided on [date], including the incident timeline, photographs, and repair estimate. Please confirm receipt and advise what remains outstanding.

That tone does two things. It keeps the record clean, and it signals that you’re managing the file carefully.

When to Escalate and Hire Professional Help

Some claims can be handled directly if the loss is modest, liability is clear, and the paperwork is straightforward. Others change shape quickly. The moment the file becomes technical, adversarial, or inconsistently handled, self-representation starts costing you your advantage.

The red flags that should change your plan

Escalation makes sense when the claim stops being a simple exchange of proof and turns into a controlled contest over value, responsibility, or access to evidence.

Consider professional help if you’re seeing any of these:

- A quick low offer: Fast money often appears before the full scope of damage is documented.

- A denial that leans on weak reasoning: If the explanation ignores your core evidence, the file may need a firmer response.

- Resistance around records or footage: If relevant evidence is hard to pin down, timing becomes critical.

- Serious injury or complex property damage: The more moving parts, the less room there is for improvised claim handling.

- Communication that changes after you become more careful: That usually means the easy concessions have ended.

Why oversight matters with a company this large

Big corporate systems make mistakes. They also cross lines. In February 2026, Walmart agreed to a $100 million judgment to settle charges brought by the FTC and 11 states over deceptive practices tied to its Spark Driver program, according to the FTC’s announcement of the Walmart judgment. That doesn’t mean your individual claim will involve the same facts. It does show that Walmart’s operational systems are not beyond scrutiny and that meaningful oversight can matter.

For claimants, the lesson is practical. Size does not equal accuracy.

When the file becomes uneven, professional representation changes the conversation from informal asking to documented advocacy.

Oregon and Washington claimants have an added reason to act early

Property owners in Oregon and Washington often deal with layered losses. Structural damage, water intrusion, business interruption concerns, volunteer-run nonprofit facilities, or disputed repair scope can all complicate a file. If Walmart’s role in the loss intersects with your own carrier, a contractor, or municipal reporting, delay gets expensive.

Professional help becomes especially useful when:

- You need a damages model, not just a receipt stack

- You’re trying to preserve a claim while also restoring a property

- The other side is narrowing the claim to only part of the loss

- You need communications centralized so nothing contradictory goes out

If you’re weighing whether the matter has crossed that line, this article on when to hire a public adjuster is a good decision guide because it focuses on trigger points, not pressure tactics.

Frequently Asked Questions About Walmart Claims

What if my car was damaged by a shopping cart in the parking lot

Report it to store management immediately and document the exact parking location, nearby cart return area, weather, and visible damage. Take wide and close photos. If anyone saw the cart roll or saw an employee handling carts nearby, get their contact information. Keep your statement factual and avoid guessing about fault until you’ve preserved the scene.

Is a defective product claim different from an in-store injury claim

Yes. A product claim usually raises different proof issues than a premises claim. Keep the product, packaging, receipt, model information, and photos of the failure. Don’t alter or discard the item. For an in-store injury, the condition of the location is often central. For a product claim, the item itself may become the key evidence.

What if Walmart asks for records I already sent

Resend them in one organized package and reference the earlier transmission date. Don’t argue first. Create a clean paper trail showing cooperation and consistency. If repeated requests continue without meaningful progress, that’s often a sign the file needs firmer management.

Are there differences for Oregon and Washington residents

Yes, mainly in how related insurance, property restoration, and documentation issues can unfold around the claim. The safest approach in either state is the same: preserve evidence immediately, communicate in writing when possible, and don’t let repair urgency erase the proof of what happened.

Can I handle a smaller claim myself

Sometimes, yes. If liability is clear, the damage is limited, and the documentation is strong, a direct claim may be efficient. If the facts are disputed, the value is substantial, or the communication turns evasive, handling it alone becomes less efficient and more risky.

If you’re in Oregon or Washington and a Walmart-related loss has turned into a documentation battle, NW Claims Management can help you evaluate the claim, organize the evidence, and decide whether it makes sense to push forward on your own or bring in professional representation. The firm works exclusively for policyholders, not insurers, and offers practical guidance for residential, commercial, and nonprofit property owners trying to secure a fair outcome.