The average insurance payout for hail damage roof claims usually falls between $8,000 and $15,000, with many claims clustering around $12,000. That sounds useful until you realize it’s only a starting point, because your actual check depends on your policy, your deductible, your roof’s age, and how well the damage is documented.

If you’re reading this after a hailstorm, you’re probably doing what most homeowners do. You’re looking at dents, scattered granules, maybe a stain on a ceiling, and trying to answer one stressful question: what is insurance going to pay?

That question matters even more in Oregon and Washington, where hail events are rising 15% according to the NOAA data cited in JTech Construction’s hail payout analysis. A lot of homeowners here still assume hail is mostly a Midwest or Colorado problem. Then a storm hits, the carrier schedules an inspection, and the first estimate doesn’t come close to what the roof contractor says it will take to restore the property correctly.

The hard part is that insurance math looks simple from the outside. It isn’t. A claim can start with a damaged roof and end with a very different outcome depending on whether the insurer classifies the loss as repairable, applies depreciation aggressively, or says part of the damage is cosmetic. If you want a fair settlement, you need to understand why the number moves.

Why the Average Hail Payout Is Just a Starting Point

Averages calm people down, but they can also mislead them.

When homeowners hear that the average hail payout is somewhere in the $8,000 to $15,000 range, they often assume their claim should land in that band. Sometimes it does. Sometimes it doesn’t come close. The number is broad because roof claims are built from separate moving parts, not from one national standard.

What changes the number

Start with the obvious. A small patch repair is not the same claim as a full tear-off and replacement. The roof material matters. The roof age matters. Your deductible matters. The valuation method in your policy matters even more.

A homeowner with a newer roof and strong replacement coverage can have a very different claim outcome than a homeowner with an older roof under an actual cash value settlement. Both can have hail damage. Both can file valid claims. The payout can still look completely different.

The average is useful for orientation. It’s not useful for negotiation.

That’s why broad guides help only to a point. If you want a good plain-language overview before you dig into your own policy, A Homeowner's Guide to Roof Insurance Claims is a practical place to get familiar with the process and vocabulary.

The real question to ask

Don’t ask, “What does hail damage usually pay?”

Ask these instead:

- What does my policy pay for. New replacement cost, or a depreciated value based on age and condition?

- How large is my deductible. Some homeowners are surprised to learn their out-of-pocket share is bigger than expected.

- Is the damage functional or cosmetic. That distinction drives a lot of disputes.

- Is the insurer pricing for a repair or a replacement. That one decision can change the claim dramatically.

If you’re in Oregon or Washington, the smartest move after a storm is to stop chasing the national average and start building your own claim file. The fair payout is the one supported by your policy language, the actual condition of your roof, and defensible documentation of the storm damage.

Replacement Cost Value vs Actual Cash Value

Replacement Cost Value and Actual Cash Value answer one basic question: does your policy pay for a new roof of like kind and quality, or does it pay a reduced amount based on age and wear?

How these two valuations change the claim

With RCV, the policy is built to cover the cost to replace the damaged roof, subject to the deductible and any policy conditions. With ACV, the carrier subtracts depreciation before paying, so the starting check is lower because the roof is treated as an aging asset.

That distinction drives real money.

A hail claim on a newer roof with RCV can support a full replacement path if the damage and policy language line up. The same storm on an older roof with ACV can produce a much smaller payment, even when the shingles are plainly damaged. Homeowners in Oregon and Washington run into this more often than they expect, especially on older composition roofs where carriers focus hard on age, prior wear, and maintenance history.

Why older roofs create bigger disputes

Older roofs usually bring more arguments over depreciation, repairability, and remaining life. Carriers often point to granule loss, prior patching, brittle shingles, or uneven weathering to justify reducing the value of the claim. From the homeowner’s side, the roof may have been keeping water out just fine until the hail hit.

That is where the numbers start to feel disconnected from reality.

The settlement is not just about storm damage. It is also about how the policy values a roof that was already partway through its service life. In practice, that means two neighbors can have the same date of loss, similar hail impacts, and very different checks because one policy pays replacement cost and the other applies depreciation first.

Recoverable depreciation causes a lot of confusion

Even under an RCV policy, the insurer often splits payment into stages. The first payment may be based on the actual cash value, with the withheld depreciation paid later after the work is completed and documented.

Homeowners often mistake that first check for the final offer.

I see this all the time. The carrier explains the estimate quickly, the homeowner hears one dollar figure, and nobody clearly separates deductible, depreciation, and unpaid line items. Reviewing the home insurance claim process helps make sense of that sequence before you accept the insurer’s version of what the claim is worth.

Where to confirm which one you have

The most reliable answer is in the policy documents. Read the declarations page, the loss settlement section, and any roof or cosmetic damage endorsements together. Those pages usually tell you whether the roof is settled at replacement cost, actual cash value, or under a limitation that only applies to certain roof surfaces or older materials.

An agent’s verbal summary from years ago is a weak substitute for the contract that controls the claim today.

If you remember one point from this section, remember this. Before arguing over contractor estimates or line-item pricing, confirm whether your roof is being valued as RCV or ACV. That single policy term often explains why the payout is either enough to complete the job or nowhere close.

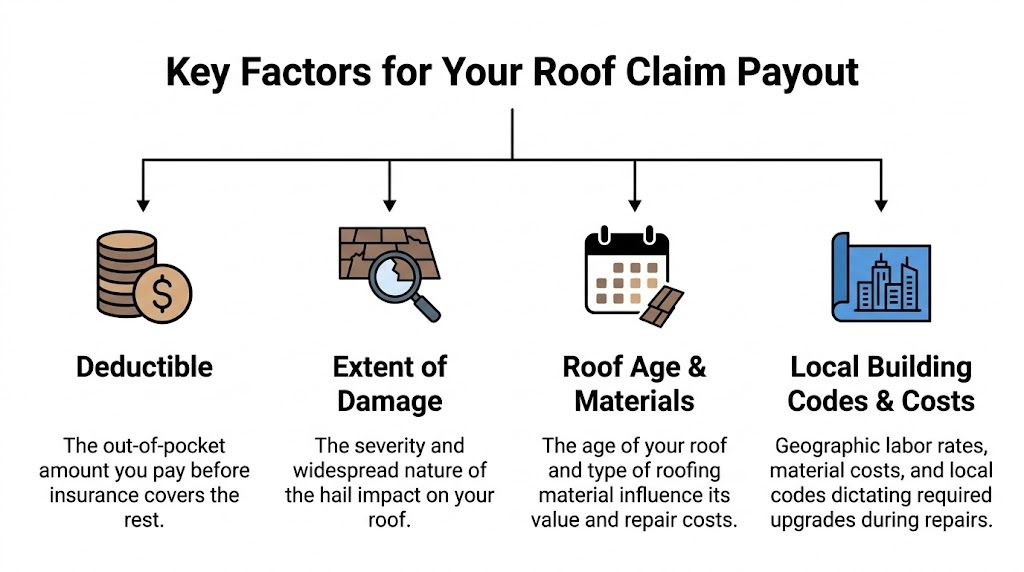

Key Factors That Determine Your Roof Claim Payout

After policy type, the main fight is over scope.

Two homeowners can have the same storm, the same shingle, and very different checks because the carrier changes one of four things: how much damage it agrees to include, what price it assigns to the work, what it deducts, and what policy limitations it applies. That is why an average payout number only gives you a rough frame. It does not tell you how your claim was calculated.

Deductible and depreciation holdbacks

The gross estimate is not the check amount.

What reaches the homeowner is reduced by the deductible first. Then, depending on the policy and the insurer’s estimate, part of the claim may be withheld until the work is completed and documented. I regularly see homeowners treat that first payment as the settlement, when it is only one stage of the claim.

That distinction matters more in Oregon and Washington than many people expect because roof work here often includes line items the first estimate misses. If the carrier under-scopes the job and also withholds depreciation, the cash shortfall hits twice.

Extent and pattern of damage

Insurers do not pay for a storm in the abstract. They pay for documented damage to specific building components.

A few marked shingles in one test square usually produce a repair discussion. Consistent impact damage across multiple slopes, damaged ridge, vents, flashing, gutters, and soft metals can support a much larger scope. The pattern matters because it helps answer the question carriers always ask. Is this a repairable spot loss, or a roof system problem tied to one storm event?

That is also why close inspection matters. Functional hail damage is often missed in quick field visits, especially on older asphalt roofs where adjusters blur together hail, age, foot traffic, and heat-related wear.

Roof age, material, and matching issues

Roofing material changes the claim math fast.

Asphalt shingles can bruise, lose granules, or fracture in ways that shorten service life even when the damage is not dramatic from the ground. Metal roofing may avoid puncture but still trigger disputes over whether dents affect function, finish, or market value. Older roofs create another problem. Carriers often point to wear and tear because it gives them a path to reduce scope or avoid replacement.

In the Pacific Northwest, matching can become just as important as age. If discontinued shingles, weathered color fade, or partial-slope repairs leave a patchwork result, the dispute is no longer just about damage. It becomes a question of whether the insurer’s proposed repair returns the roof to a reasonably uniform condition under the policy and state rules.

Local pricing, steep roofs, and code upgrades

Many approved claims still come up short.

Roof pricing in Oregon and Washington is shaped by local labor availability, disposal costs, underlayment requirements, steep-pitch safety setup, high-wind details in some areas, and municipal code triggers. If the estimate leaves out starter, ridge cap, flashing replacement, detach and reset items, permit costs, or code-required upgrades, the settlement can look acceptable on paper and still fail in practice.

A detailed property damage assessment for the full roof system often exposes those missing line items before the homeowner signs a contractor agreement based on an underfunded claim.

Documentation quality

Good documentation changes the dynamic.

Clear photos, test squares, elevation notes, date-of-loss support, contractor findings, and a line-by-line estimate give you a much stronger position than a general statement that the roof was hit hard. Carriers are far more likely to limit a payout when the file is thin or when the evidence does not connect the storm to the full scope being claimed.

That is the part many homeowners never see. The payout is not driven by damage alone. It is driven by what can be proven, priced, and defended.

Sample Hail Damage Payouts in Oregon and Washington

The easiest way to understand the average insurance payout for hail damage roof claims is to walk through two realistic scenarios. These aren’t case studies. They’re examples built from the verified cost and payout ranges above so you can see how the math changes.

One homeowner can have valid damage and still end up with less money because of policy type and roof age. Another can have a more favorable policy and a cleaner path to replacement.

Scenario comparison

Repair costs for asphalt shingles average $4.50 to $7 per square foot, while full replacements for a standard home can range from $4,000 to $16,000 depending on size and materials, and State Farm hail claims averaged $12,000 in 2020 and 2021 according to Cape Analytics’ hail risk review.

| Line Item | Scenario A: Portland (15-yr-old Asphalt, ACV Policy) | Scenario B: Bend (5-yr-old Metal, RCV Policy) |

|---|---|---|

| Roof type | Older asphalt shingle roof | Newer metal roof |

| Policy type | ACV | RCV |

| Damage conclusion | Widespread impact leads to replacement discussion | Hail impact requires larger scope review |

| Replacement cost benchmark | Full replacement falls within the $4,000 to $16,000 standard-home range | Full replacement also falls within the $4,000 to $16,000 standard-home range, depending on size and materials |

| Depreciation treatment | ACV reduces payment before the check is issued | Initial payment may be reduced by recoverable depreciation, with later release after work completion |

| Deductible effect | Deductible still applies and reduces net funds to owner | Deductible still applies and reduces net funds to owner |

| Likely homeowner reaction | “Why is the payment so far below replacement price?” | “Why didn’t they send the whole amount upfront?” |

What these two examples show

The Portland homeowner’s frustration usually comes from depreciation. An older roof under ACV can produce a settlement that feels disconnected from today’s replacement cost, even if the insurer says it followed the policy correctly.

The Bend homeowner’s confusion is different. The insurer may agree on replacement cost in principle but still withhold part of the money until the roof is replaced and invoices are submitted. The claim isn’t necessarily underpaid yet. It may be incomplete.

Two roof claims can start with similar storm damage and end with different checks for one reason alone. Policy structure.

Where homeowners misread the numbers

The most common mistake is comparing an insurer’s net payment to a contractor’s gross replacement proposal as if they should match on the first check. They usually won’t.

The second mistake is treating the insurer’s scope as complete without checking whether all damaged components were included. On hail claims, the missing money is often sitting in omitted line items, depreciation treatment, or a repair-versus-replace decision that was never challenged properly.

How to File Your Hail Damage Claim for Best Results

The early steps matter more than most homeowners realize. A weak start creates problems that are hard to unwind later.

If your roof may have hail damage, think like you’re preserving evidence, not just reporting an inconvenience.

What to do first

Document before cleanup

Take clear photos and video of the roof from the ground if that’s the safe option. Capture downspouts, gutters, soft metals, screens, siding, deck furniture, and any interior staining. Those supporting impacts help establish the storm story.Prevent further damage without starting permanent repairs

If water is entering the home, take reasonable steps to reduce additional damage. Temporary mitigation is smart. Permanent replacement before the insurer inspects can create an avoidable fight over evidence.Review your policy before the first long call with the carrier

Check the deductible, roof settlement language, and any endorsements that mention cosmetic damage, ACV, or special wind and hail terms.

What to say when you call

Keep the first report simple and factual.

- State the event clearly. Report the date of the storm if known and describe the visible issues.

- Avoid guessing about cause beyond what you observed. Don’t speculate about old damage, maintenance history, or whether “it’s probably minor.”

- Ask what the carrier needs. Get the claim number, next steps, inspection timeline, and document submission method.

You’ll usually do better by being precise than by saying too much.

Build a clean claim file

A strong hail claim file usually includes:

- Photos and video taken as soon as conditions are safe

- Notes on timing of the storm and when damage was discovered

- Contractor or roofing inspection findings if you’ve obtained them

- Interior evidence such as leaks, staining, or insulation issues

- A communication log with dates, names, and summaries

If you want a practical walkthrough of the reporting side, this guide on how to file a property damage claim is a helpful checklist.

The first inspection doesn’t decide what happened to your roof. The evidence does.

What usually hurts a claim

Waiting too long. Throwing away damaged materials without documentation. Letting the insurer inspect without having your own records organized. Agreeing too quickly that visible dents are “just cosmetic” before anyone has evaluated whether the roof’s function was affected.

The goal isn’t to turn your kitchen table into a war room. It’s to make sure the carrier’s file starts with the right facts instead of assumptions that are hard to reverse.

Countering Common Insurer Tactics That Reduce Payouts

Insurance companies don’t need to deny every claim to save money. They often reduce claim cost by narrowing scope, expanding depreciation, or framing damage in the least expensive category available.

That’s what homeowners need to watch.

Tactic one, repair the smallest area possible

A carrier may write for a partial repair where the roof system, material match, or damage spread points toward replacement. That doesn’t always mean bad faith. Sometimes it means the inspection was incomplete.

Homeowners should ask to see exactly how the insurer determined the damaged area and why adjoining components were excluded.

Tactic two, call it cosmetic

This comes up often with metal roofing and with visible impact marks that the carrier says don’t impair performance. Sometimes that position is valid. Sometimes it ignores real functional concerns.

The dispute usually turns on evidence. Close inspection, test areas, manufacturer guidance, and a careful review of slope-by-slope conditions matter more than broad statements from either side.

Tactic three, bury the reduction inside the estimate

The painful part isn’t always the denial. It’s the estimate that looks official but leaves out necessary work.

The gap between average insurance payouts of $12,000 to $17,000 and roof replacement costs of $8,500 to $24,000 can leave homeowners with $7,000+ out of pocket after deductible, according to Payne Law’s hail claim article. That gap often appears because the claim was undervalued, not because the roof somehow got cheaper to replace.

Tactic four, assume the policyholder won’t challenge line items

That assumption is sometimes correct.

A careful line-by-line review often reveals omissions in tear-off, accessories, flashing, waste, code items, detached structures, gutters, or interior follow-on damage. Technology is making this easier to spot. For example, AI can help identify missed items in estimate review, which is useful context for homeowners trying to understand how much can be overlooked in a scope.

If you want a clearer sense of the patterns adjusters use to trim claims, this overview of insurance adjuster tricks is worth reading.

A low offer isn’t always the final word. Sometimes it’s the opening position.

The answer is not outrage. It’s documentation, scope review, policy analysis, and persistent negotiation grounded in the claim file.

Take Control of Your Hail Damage Claim

By the time a homeowner searches for the average insurance payout for hail damage roof claims, the actual problem usually isn’t curiosity. It’s uncertainty.

You want to know whether the insurer’s number is fair. You want to know whether you’re supposed to absorb the gap. You want to know if the roof qualifies for replacement or if you’re being pushed into a patch that won’t solve the problem.

What matters most

The national average gives you context. It does not tell you what your roof claim is worth.

Your outcome depends on four things more than anything else:

- Your policy valuation method. RCV and ACV can produce very different claim results.

- Your deductible and payment structure. Initial checks often look smaller because of deductions and holdbacks.

- The quality of the damage documentation. Strong evidence changes negotiations.

- The accuracy of the insurer’s scope. Missing line items and narrow repair decisions reduce payouts fast.

The practical mindset

Treat the claim like a financial document backed by physical evidence. That’s what it is.

Read the estimate. Read the policy language that applies to roof settlement. Compare the insurer’s scope to what the property needs. If the numbers don’t make sense, don’t assume the carrier is automatically right just because the form looks polished.

For many homeowners, bringing in professional representation is what changes the claim from confusing to manageable. If you’re weighing that step, this explanation of the benefits of hiring a public adjuster lays out where that help fits.

A fair settlement doesn’t come from the average. It comes from proving the actual loss, applying the right policy terms, and refusing to let shortcuts define the value of your claim.

If you’re in Oregon or Washington and need help sorting out a hail damage roof claim, NW Claims Management can evaluate the loss, review the policy, and help you pursue the full settlement your coverage allows. When the insurer’s estimate doesn’t match the actual scope of damage, having an advocate on your side can make the process clearer, faster, and far less stressful.