When disaster strikes your home, the first person your insurance company sends out isn't there to write you a check on the spot. This person is a type of surveyor—though you’ll more commonly hear them called an adjuster.

These surveyors in insurance claims are the insurance company's official investigators. Their job is to figure out what happened, what it will cost to fix, and report back. The most important thing to remember is their loyalty is to the company that signs their paychecks, not to you.

What Is a Surveyor in an Insurance Claim?

Let's say a pipe bursts, flooding your finished basement. The water has wrecked the drywall, carpeting, and a good chunk of your furniture. After you file a claim, a person shows up with a camera, a measuring tape, and a clipboard. That’s the insurance surveyor (or adjuster). Their mission is to be the eyes and ears of the insurance company.

These professionals are central to the massive global insurance industry. To give you a sense of scale, the property and casualty insurance market is enormous. The United States alone represents 40.4% of this global market, a staggering figure that shows just how many claims rely on a surveyor’s assessment to determine the final payout. You can dig into the numbers yourself in the IAIS Global Insurance Market Report 2026.

The Surveyor's Core Responsibilities

So, what does an insurance surveyor actually do? Their work really boils down to three main jobs. Getting a handle on these will give you a much clearer picture of the claims process.

- Investigation: First, the surveyor needs to figure out the cause of the damage and check if it’s covered by your policy. They’ll inspect the property, take lots of photos, and make detailed notes on everything they observe.

- Evaluation: Next, they measure the full scope of the damage. This means calculating the square footage of affected areas, listing all the materials that need to be replaced, and creating an inventory of your damaged belongings. We cover this in-depth in our guide on the property damage assessment process.

- Valuation: Finally, the surveyor plugs all this information into specialized software to estimate the cost of repairs. This final number is what the insurance company will use to build its settlement offer to you.

Think of the claims process like a legal case. The insurance company has its own lawyer (the company or independent adjuster) looking out for its interests. Shouldn't you have one too? This is where a public adjuster comes in—they are the expert advocate working exclusively for you.

Whose Side Are They On?

The surveyor your insurer sends might be perfectly friendly and seem helpful. But it's absolutely critical to remember who they work for. Their legal and professional duty is to their employer—the insurance company. Their objective is to resolve the claim accurately, but also efficiently and in a way that protects the insurer's bottom line.

This doesn't make them bad people, but it does mean their perspective is fundamentally different from yours. An insurer's adjuster might unintentionally overlook hidden damage, base their estimate on cheaper materials, or interpret a gray area in your policy in the company's favor.

For homeowners in Oregon and Washington, understanding this distinction between company adjusters and public adjusters is the key. Recognizing this difference in allegiance is the first step toward protecting your own financial recovery after a loss.

The Three Types of Adjusters in Your Claim

After a fire, flood, or major storm damages your property, you'll start hearing the word "adjuster" a lot. But here’s something most homeowners don't know: there are three very different kinds of adjusters, and understanding who works for whom is one of the most important lessons you can learn.

Their loyalties are fundamentally different, and that difference can have a massive impact on the final amount of your settlement check. It’s crucial to know who is on your side and who is on the insurance company’s payroll.

The Company Adjuster

The first person you'll likely meet from the insurance company is the company adjuster. This individual is a direct employee of your insurer—they’re on the company payroll, get company benefits, and their professional loyalty is to their employer.

Their job is to investigate your claim and determine a settlement amount based on the insurance company's guidelines. While they need to be professional, their legal and financial obligation is to the insurer, not to you. They are tasked with settling your claim for the lowest amount their company considers fair under the policy.

The Independent Adjuster

Next, you might encounter an independent adjuster. The name itself can be incredibly misleading. They aren't truly "independent" in the way a homeowner might hope. Instead, they are third-party contractors hired by insurance companies when they need extra help.

Insurers often bring in independent adjusters for a few key reasons:

- During Catastrophes: After major events like wildfires in Oregon or Washington, insurers get overwhelmed with claims and hire independents to manage the surge.

- For Specialized Claims: If a claim is particularly complex, like a large commercial fire, an insurer might tap an independent with specific expertise.

- In Remote Areas: They're also used in locations where the insurance company doesn’t have its own staff adjusters nearby.

Even though they're a contractor, their allegiance is identical to a company adjuster's. The insurance company pays their invoices, so they are contractually bound to protect the insurer’s financial interests.

The Public Adjuster

Finally, there’s the public adjuster. This is the only type of adjuster who works directly and exclusively for you, the policyholder. A public adjuster is a state-licensed professional you hire to act as your personal advocate throughout the entire claims process.

A public adjuster’s sole fiduciary duty is to you. They level the playing field by managing every aspect of your claim, from documenting damage to negotiating with the insurer, all with the single goal of maximizing your financial recovery.

Their entire purpose is to prepare, present, and negotiate your claim to achieve the best possible outcome. They conduct their own detailed damage assessment, meticulously value your losses, and argue on your behalf using the specific language of your policy. We dig much deeper into this crucial relationship in our guide comparing a public adjuster vs an insurance adjuster.

To make this distinction as clear as possible, let's break down who works for whom.

Insurance Adjuster Comparison: Who Works for Whom?

This table cuts through the confusion, showing you exactly where each adjuster's loyalty lies.

| Adjuster Type | Who They Work For | Primary Goal | Who Pays Them |

|---|---|---|---|

| Company Adjuster | Your Insurance Company | Protect the insurer's interests and minimize payout. | The Insurance Company |

| Independent Adjuster | Your Insurance Company | Protect the insurer's interests and minimize payout. | The Insurance Company |

| Public Adjuster | You, The Policyholder | Protect your interests and maximize your payout. | You (via a small % of the settlement) |

As you can see, both company and independent adjusters are firmly on the insurance carrier's side of the table. Only a public adjuster is 100% in your corner, making them an indispensable partner for any homeowner in Oregon or Washington facing a significant or complex property damage claim.

How Technology Shapes Modern Claim Assessments

The image of an insurance adjuster with just a clipboard and a measuring tape is a thing of the past. Today, the best surveyors in insurance claims rely on sophisticated technology to uncover hidden damage, create incredibly detailed reports, and build an airtight, evidence-based case for your loss. It's not just about working faster; it's about being undeniably accurate.

For you as a homeowner, this is a huge advantage. When an adjuster uses these advanced tools, they create a factual record of your damage that is much harder for an insurance company to argue with or downplay. A claim built on hard data, not just a quick walkthrough, has a much stronger foundation for a full payout.

Seeing Through Walls and Above Roofs

Some of the worst damage after a disaster isn't what you can see at first glance. Modern technology gives a skilled surveyor the ability to find what the naked eye would miss, ensuring every last detail makes it into your claim.

Here are a few game-changing tools:

- Drones: For homes in Oregon and Washington with steep or tricky rooflines, drones are a lifesaver. They can safely capture high-resolution photos of wind, hail, or fire damage without putting an inspector in a dangerous situation, providing clear photographic evidence.

- Thermal Imaging Cameras: After a fire is put out or a pipe bursts, moisture gets trapped. It hides behind walls and seeps under floors. Thermal cameras are designed to spot these temperature differences, revealing hidden water pockets that will cause mold and rot if they aren't dealt with.

- 3D Scanning and Modeling: Tools like Matterport create a complete, interactive 3D "digital twin" of your damaged property. This gives you an exact, measurable record of the home's condition before any repairs start, heading off any arguments about the original layout or the full scope of damage.

A detailed, technology-driven assessment creates an objective truth. It moves the conversation from the insurer's opinion of the damage to the factual reality of what it will take to make you whole again. This is a critical step in a successful property damage claim process.

The Power of Data in Claim Estimates

It's not just the inspection gadgets that matter. The software used by expert surveyors is just as critical. Top-tier estimating platforms like Xactimate allow an adjuster to plug in precise measurements and material types, which then generates a line-by-line estimate based on current, local costs for labor and materials.

This data-first approach takes all the guesswork out of the equation. Instead of getting a vague lump sum, you receive a detailed breakdown that justifies every single dollar being requested. That level of detail is absolutely essential when it's time to negotiate with the insurance company.

This rise of insurance analytics is transforming the surveyor's job. It merges traditional, hands-on inspections with powerful data analysis to make claims more accurate than ever. The global insurance analytics market hit USD 15.75 billion in 2025 and is expected to skyrocket to USD 47.97 billion by 2033. Risk management—a core part of what surveyors do—is the biggest piece of this market, proving how vital analytics have become in property damage assessments. You can read the full research about the insurance analytics market to see more on this trend.

When a public adjuster from a firm like NW Claims Management puts these tools to work for you, they aren't just presenting an opinion. They are delivering a comprehensive, data-backed report that your insurance company has no choice but to take seriously. This is how technical expertise directly translates into a better financial outcome for your claim.

What to Expect During the Property Inspection

The day the insurance company’s surveyor shows up can be incredibly stressful. For most homeowners, it feels like a final exam where a stranger is about to decide your financial future. But it doesn't have to be that way. Knowing what to expect—and how to prepare—can turn you from a nervous bystander into a confident advocate for your own claim.

This visit is a make-or-break moment. The surveyor's report is the foundation for the insurance company's first settlement offer, so it’s absolutely critical that their assessment is accurate and complete. If you’re proactive, you can help steer the inspection and make sure they see the full extent of the damage, not just the obvious stuff.

Preparing for the Surveyor's Visit

A bit of prep work on your end can make a world of difference. Before the adjuster even rings your doorbell, you should already have your own evidence organized and ready to go. This way, you’re not just reacting to what they find; you're presenting a clear, documented picture of your loss from the very beginning.

Here’s what you should have in hand:

- Your Insurance Policy: Keep a copy of your full policy easily accessible. The adjuster will have their own, of course, but having yours ready shows them you’re an informed policyholder who means business.

- Your Own Photo and Video Log: Use your phone to document everything. Take wide shots of damaged rooms for context, then zoom in on specific items. When shooting video, talk through what you’re filming, explaining the damage you see.

- A Detailed List of Damaged Items: Don't rely on your memory in the heat of the moment. Walk through your property beforehand and create a comprehensive list of every single thing that was damaged or destroyed.

Think of it like you're building a case file for your own claim. The more organized and thorough you are, the more credible your position becomes. This simple prep work ensures you won't get caught off guard and forget to point out crucial damage.

During the Inspection Walkthrough

When the surveyor arrives, your job is to be a helpful, but watchful, guide. Walk with them through every inch of the property. With your notes and photos in hand, you can make sure they don't miss a thing. They’re seeing your home for the first time—you’re the one who knows exactly what you’ve lost.

Politely point out damage they might not spot right away, like soot that has settled inside kitchen cabinets, water stains hidden behind furniture, or flooring that has started to warp under a rug. You could say something like, "I want to make sure you see the smoke damage along the top of this wall. It’s a bit faint, but it actually runs the whole length of the room."

To get a truly accurate picture, many adjusters now use modern tools to find damage that’s invisible to the naked eye. This can include everything from aerial surveys to specialized remote-controlled equipment for inspecting hard-to-reach areas. You can find more details in this guide to using modern-day drone inspection services. These technologies provide hard evidence that can be essential for proving complex claims.

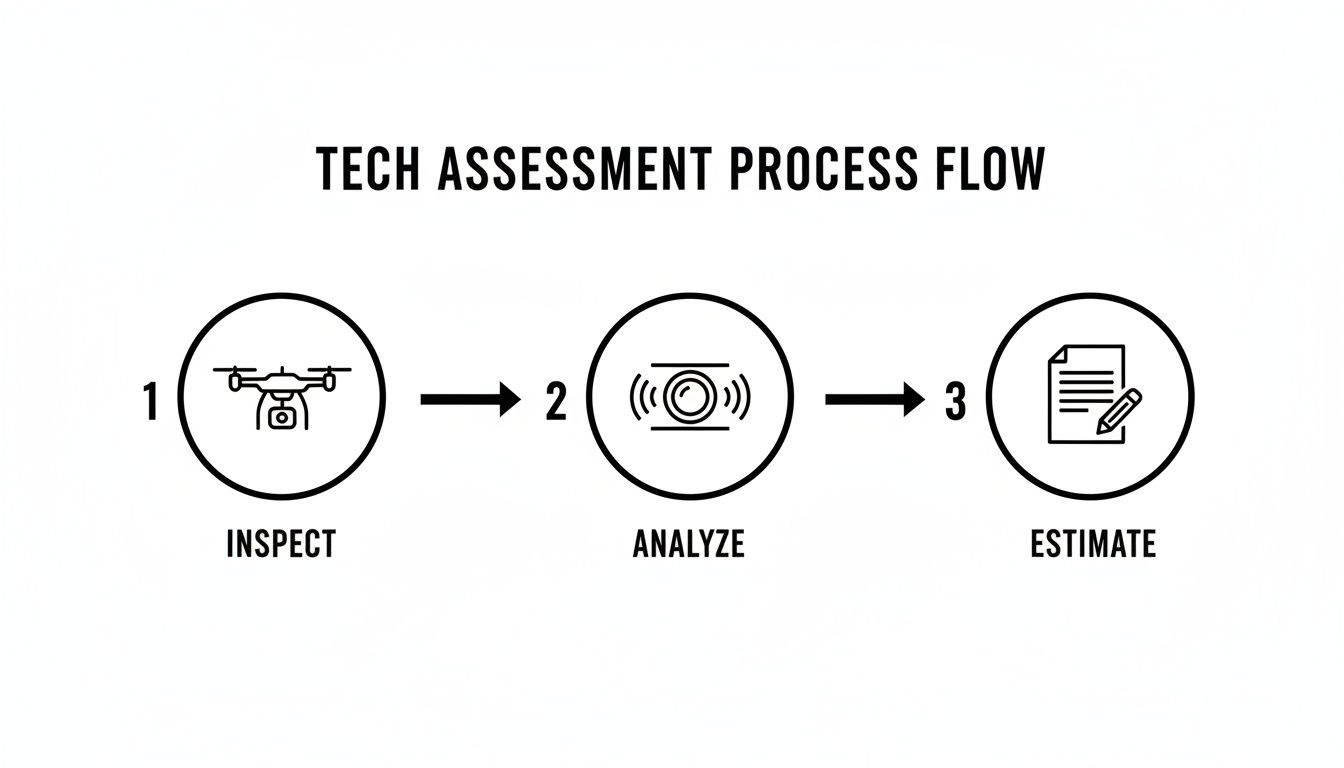

This next image breaks down the modern, tech-focused process that the best surveyors in insurance now follow.

It’s a clear, three-step workflow: using tools like drones to inspect the property, thermal cameras to analyze for hidden moisture or structural issues, and specialized software to estimate the true cost of the loss with precision.

After the Inspection

Once the walkthrough is done, the surveyor might ask you to sign some paperwork. Be very careful here. It is perfectly fine to say, “I’d like to review this with my public adjuster before signing anything.” Never sign a "full and final release" or any document you don't fully understand—you could unknowingly sign away your right to any further compensation.

After the visit, the surveyor will head back to their office to write up a report and create a scope of loss, which is their estimate for repairs. This can take days or even weeks. By preparing ahead of time and being an active participant, you’ve done everything you can to ensure their report is based on a complete and accurate picture of your damages, setting the stage for a fair negotiation.

When You Should Hire a Public Adjuster

Trying to manage a major property damage claim on your own can feel overwhelming. After a disaster like a fire or a serious flood, you’re already dealing with emotional stress and a tidal wave of urgent decisions. It's right then, when you're most vulnerable, that you have to figure out if you have the right team fighting for you.

Sure, the insurance company sent their own surveyor, but remember who they work for. Their job is to protect their employer’s bottom line. So, when does it make sense to bring in an expert who works only for you? There are a few key moments when hiring a public adjuster isn't just a smart choice—it's essential for your financial recovery.

The Claim is Large or Complicated

When the stakes are high, you need a pro in your corner. If your property has suffered catastrophic damage from a fire, a major storm, or widespread flooding, the claim will be incredibly complex. These situations are never simple, often involving structural failures, smoke and soot contamination, hidden water damage, and a mountain of lost personal belongings.

Think of a Seattle business owner trying to reopen after a fire; they're not just dealing with rebuilding costs but also complex business interruption losses. Or consider an Oregon family completely overwhelmed by paperwork after a flood destroyed their home. They need more than a simple repair estimate—they need a comprehensive strategy. In these high-value, messy claims, a public adjuster's expertise is absolutely critical to make sure nothing gets overlooked.

A public adjuster is your personal advocate. They use their deep knowledge of insurance policy language, damage valuation, and negotiation tactics to level the playing field. Their entire purpose is to build an undeniable case for the full and fair value of your loss, ensuring you have the money you need to truly rebuild.

The Insurer's Offer is Too Low

One of the most common red flags we see is when a homeowner gets a settlement offer that is just shockingly low. It’s a gut-punch. This often happens because the insurer's adjuster rushed their inspection, used low-cost materials in their estimate, or completely missed damage that wasn't immediately obvious.

Don't just accept it. A lowball offer is frequently a negotiating tactic, a test to see if you’ll take the quick money and disappear. A public adjuster will immediately step in, perform their own detailed inspection, and create a powerful, evidence-based counter-offer that compels the insurance company to come back to the table and negotiate fairly. You can learn more about the benefits of hiring a public adjuster when you're facing this exact situation.

Your Claim Has Been Denied

An outright claim denial feels like a final blow. But while the insurance company might want it to be their final word, you don't have to let it be. Insurers often deny claims by claiming the cause of damage isn't a covered peril or that you didn't meet some obscure policy condition.

A denial is a roadblock, not a dead end. A public adjuster knows how to find a way forward. They will meticulously review your policy against the insurer's denial letter, searching for errors and misinterpretations. More often than not, a professionally argued appeal—backed by new evidence and expert assessments—can get a denied claim reopened and paid.

The role of surveyors in insurance is becoming more crucial as global catastrophe losses climb. With insured losses from natural disasters soaring past $100 billion in the first half of 2025 alone—well beyond the 10-year average—insurers are under immense pressure to control payouts. This environment makes having an expert advocate in Oregon and Washington more valuable than ever. You can see more on this trend in Aon's Q3 2025 global report.

Common Questions About Public Adjusters

Dealing with a property damage claim can throw a lot of confusing terms your way, and "public adjuster" is often one of them. If you're wondering what they do and if you need one, you're not alone. Let's walk through some of the most common questions we hear from homeowners.

Getting clear answers is the only way to make a smart decision for your claim. It helps cut through the noise and gives you the confidence to take the right next step toward getting your life back to normal.

How Much Does a Public Adjuster Cost?

This is usually the first question on everyone's mind, and the answer is simple: there are no upfront fees. Public adjusters work on a contingency fee basis.

What does that mean? They get paid a small, agreed-upon percentage of the final settlement they secure for you. Their success is literally tied to yours. If they don't get you paid, they don't get paid. It's a risk-free way to put an expert in your corner. If you want to dive deeper into the numbers, we've created a complete guide on how much a public adjuster costs.

Can I Hire a Public Adjuster After My Claim Has Started?

Yes, absolutely. It's almost never too late to bring in a professional advocate. A good public adjuster can jump in and make a difference at nearly any point in the process.

Many homeowners hire a public adjuster:

- Right after the damage happens to make sure the claim starts off on the right foot.

- After getting a low settlement offer that feels completely inadequate.

- Even after the insurance company has denied the claim outright.

A skilled adjuster can reopen communication, find and submit evidence the insurance company missed, and challenge a wrongful denial. Their job is to fight for the fair payment you’re entitled to under your policy.

Will My Insurer Get Mad if I Hire a Public Adjuster?

It's a common worry, but hiring a public adjuster is a completely normal part of the insurance world. It’s your right as a policyholder, and insurance companies—along with their own surveyors in insurance—work with public adjusters every day. It's just business for them.

You might think it adds tension, but an experienced public adjuster often streamlines the process. They prepare organized, detailed, and evidence-backed arguments. This turns the claim into a fact-based negotiation instead of a frustrating back-and-forth, which can actually make things more efficient for everyone involved.

What Is the First Step to Get Help with My Claim?

The best first move is simply to ask for a no-obligation claim review. Reputable public adjusting firms will offer a free consultation to hear about your situation, look over your policy, and give you their honest opinion on the best path forward. This initial chat gives you professional insight from the very beginning, with zero strings attached.

Don't try to navigate the claims process on your own. The team at NW Claims Management is here to give you the expert support you need to secure a full and fair settlement. Contact us today for a free, no-obligation review of your claim.