When disaster strikes your home or business, one of the first people you'll meet is an insurance adjuster. But here’s something most people in Oregon and Washington don’t realize until it's too late: not all adjusters are on your side. Understanding who an adjuster really works for is the most critical piece of the claims puzzle.

This is where the term independent adjusting company often causes confusion. The name sounds impartial, but the reality is quite different.

Who's Who? The Three Types of Insurance Adjusters

After you file a claim, the person sent to evaluate the damage is called an adjuster. Their role is to investigate what happened, see what your policy covers, and ultimately decide how much money the insurance company should pay for the loss.

But it’s not that simple. The broader insurance industry has a few different players, and it's essential to know which team they play for. The entire system is split between those who represent the insurance company and the one person who can represent you.

To make this crystal clear, let's break down who you're likely to meet and where their loyalties lie.

Insurance Adjuster Comparison: Who Works for Whom?

This table cuts through the jargon and shows you exactly who's who in the claims process.

| Adjuster Type | Who They Work For | Whose Interests They Represent |

|---|---|---|

| Staff Adjuster | A single insurance company (e.g., State Farm, Farmers) | The insurance company |

| Independent Adjuster | Multiple insurance companies (as a contractor) | The insurance company |

| Public Adjuster | You, the policyholder | You, the policyholder |

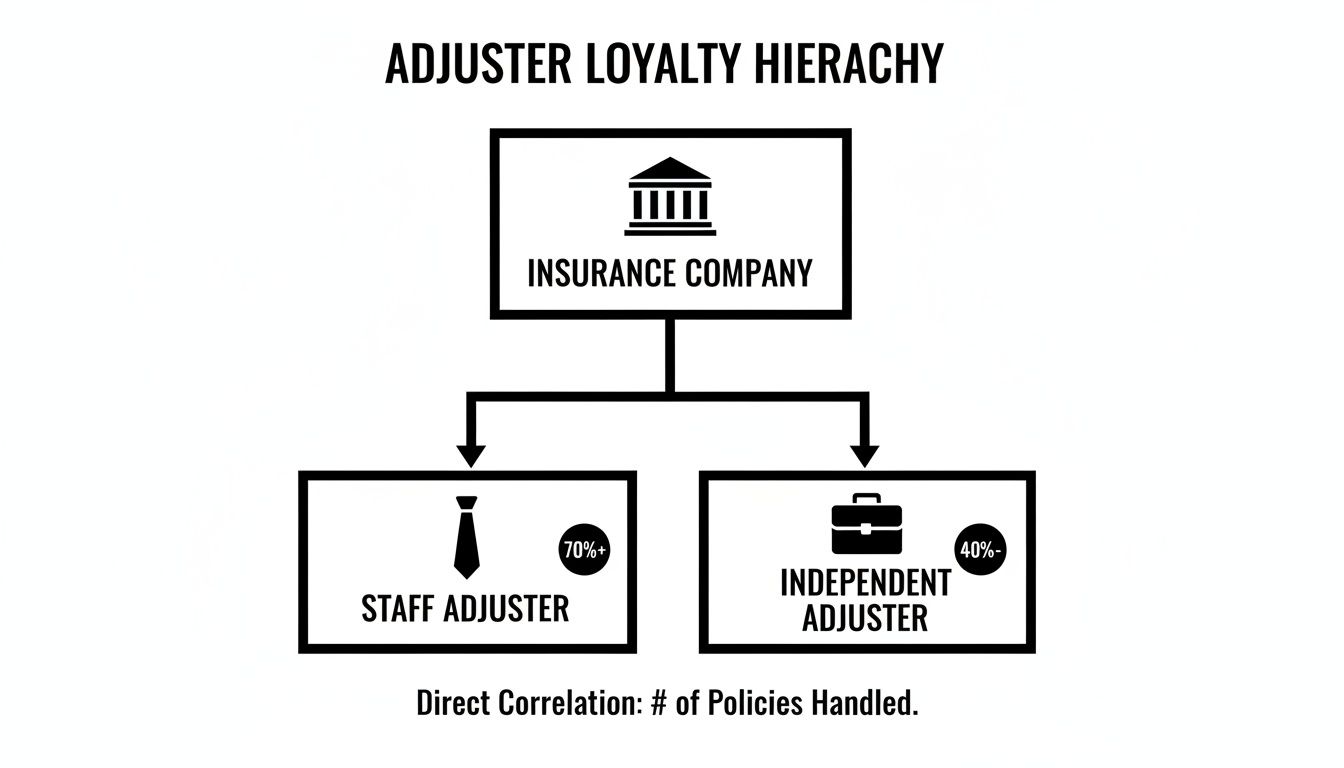

As you can see, two out of the three types of adjusters are paid by and work for the insurance carrier. Only one works for you.

The Two Adjuster Types Working for the Insurance Company

The overwhelming majority of adjusters you'll encounter are paid by your insurance carrier. Their job is to settle your claim fairly, yes, but always with an eye on protecting the insurer's financial interests.

Staff Adjusters: These are salaried employees who work directly for a single insurance company, like Allstate or Progressive. Handling claims is their full-time job. They have a desk at the company, get a W-2, and their allegiance is squarely with their employer.

Independent Adjusters: This is the one that trips people up. When a major event like a wildfire or ice storm hits, insurance companies get swamped with claims. To handle the surge, they hire an independent adjusting company on a contract basis. Though they are called "independent," they are paid by the insurance company to represent the insurance company's interests.

This diagram perfectly illustrates the chain of command. Both the staff and independent adjuster ultimately answer to the insurance carrier.

This creates an inherent conflict of interest. The person responsible for calculating your damage is employed by the same company that has to pay for it.

An adjuster's professional allegiance fundamentally dictates their approach to your claim. The person writing the check is the person they are ultimately working to satisfy. This is why it’s so important to know who is on your side.

This setup can put homeowners at a real disadvantage. We've seen situations where independent adjusting firms instruct their adjusters not to share repair estimates with the policyholder, leaving them in the dark about their own claim. It's a clear sign that you need your own expert in your corner.

The One Adjuster Working Exclusively for You

There is only one type of adjuster who is licensed by the state to work on your behalf, representing your interests alone.

- Public Adjusters: You hire a public adjuster directly to act as your dedicated advocate. We manage every detail of the claim for you—from documenting the full scope of the damage to negotiating with the insurer to ensure you get the maximum settlement you're entitled to. Our loyalty is 100% to you, the policyholder.

Think of it this way: the insurance company arrives with its team of experts (staff and independent adjusters) to protect its finances. Hiring a public adjuster is how you level the playing field by bringing your own expert to the fight.

You can explore the critical differences between a public adjuster vs insurance adjuster in our guide, but just remember this: it’s the single most important distinction when you're facing a major property loss.

Why You Need a Public Adjuster on Your Side

It's easy to get confused by the term "independent adjuster." While they aren't direct employees of an insurance company, they are independent contractors whose client is always the insurer. This sets up an inherent conflict of interest when it's your home, your business, and your financial future hanging in the balance.

To truly level the playing field, you need a different kind of expert in your corner: a public adjuster. A firm like NW Claims Management is licensed by the states of Oregon and Washington to work exclusively for you, the policyholder. Our only loyalty is to you and to securing the fair and full settlement you're entitled to. Think of us as your private advocate in a complex process that is otherwise dominated by the insurance company's team.

Your Exclusive Advocate in the Claims Process

Hiring a public adjuster is about so much more than just getting help with paperwork. It means bringing on a dedicated partner to manage the entire claims process from the moment disaster strikes until your final check is cut. This partnership lifts an enormous technical and emotional weight off your shoulders, freeing you to focus on what matters most—your family, your business, and your recovery.

We act as a powerful counterweight to the insurance company's vast resources. The first thing we do is a deep, forensic review of your insurance policy. It's common for us to find hidden or overlooked coverages that can dramatically increase your final settlement. Most people have no idea about the full extent of the benefits they've been paying for until an expert combs through the fine print.

From there, we get to work meticulously documenting every single detail of your loss. This isn't just a quick walkthrough.

- Structural Damage: We go far beyond a surface-level glance. Our team assesses everything from the foundation to the trusses, creating incredibly detailed, line-item repair estimates using the same software the insurance companies use.

- Personal Property: Compiling a complete inventory of every lost belonging is a heartbreaking and overwhelming task. We guide you through it, accurately pricing each item to make sure you are fully compensated for what you've lost.

- Business Interruption: For our commercial clients, we dive into the numbers to calculate lost income and extra expenses, building a rock-solid case to ensure the business can survive the downtime.

Navigating Regulations and Economic Pressures

A public adjuster’s deep understanding of state-specific insurance law is one of your biggest advantages. Both Oregon and Washington have a complex web of laws and administrative codes that dictate how insurance companies must handle claims. We use this knowledge to hold carriers accountable and push back against common tactics used to delay, deny, or underpay what you are owed.

This expertise has never been more critical. The claims adjusting industry is projected to become a $10.8 billion market, with revenues climbing as factors like inflation cause insurers to scrutinize every dollar. This economic pressure means carriers are looking harder than ever to minimize payouts, which makes having an expert advocate essential.

A public adjuster serves as your professional representative, ensuring that the valuation of your loss is based on the true cost of rebuilding your life, not the insurer’s desire to protect its bottom line.

This is precisely why our firm exists. We don't work for some "independent adjusting company" that serves dozens of different insurers; we work only for you. By using our specialized skills, we make sure the details of your claim are documented and presented so thoroughly that the insurance company simply cannot dispute them.

If you're facing a major property loss, learning about the benefits of hiring a public adjuster is the most important first step you can take toward a fair recovery. We bring the expertise and advocacy you need to turn a stressful, one-sided ordeal into a balanced negotiation where your rights are fiercely protected.

The Public Adjusting Process From Start to Finish

Hiring a public adjuster can feel like a big decision, so it’s natural to wonder what happens next. It’s not about starting a fight with your insurance company. It’s about leveling the playing field with professional documentation and expert advocacy so you can get a fair outcome.

We take the burden of managing the claim off your shoulders, freeing you up to focus on getting your life back on track. Here’s a clear, step-by-step look at how we’ll guide your claim from our first conversation to the final check.

Step 1: Initial Claim Evaluation and Policy Review

It all starts with a free, no-pressure consultation. We’ll sit down with you to listen to your story, get a handle on the damage, and look at what the insurance company has offered so far, if anything. This is where you’ll immediately see the difference between us and an independent adjusting company sent by your insurer.

More importantly, we dive deep into your insurance policy. This document is a complicated legal contract, and most people have no idea what’s actually in it. We pore over the fine print—the endorsements, exclusions, and special provisions—to map out every possible source of coverage you're entitled to. Nothing gets left on the table.

Step 2: On-Site Forensic Inspection

Once you give us the green light to represent you, we get to work with a meticulous, on-site inspection. This isn't the quick walkthrough the carrier's adjuster might have done. Our job is to uncover and document the full extent of the damage, especially the problems that are easy to miss or that only show up later.

This deep dive includes:

- Structural Analysis: We check everything from the foundation to the rafters. We’re looking for issues that aren't immediately obvious, like hidden smoke damage inside walls or how water saturation may have weakened the structure.

- Contents Inventory: This is often the hardest part for homeowners. We help you create a detailed list of every single item that was damaged or destroyed. It’s an emotional process, but cataloging and valuing your personal property is absolutely critical for a fair settlement.

- Evidence Collection: We bring the right tools for the job. Thermal cameras, moisture meters, and high-resolution photography help us build an undeniable record of the loss. This evidence becomes the bedrock of your entire claim.

Step 3: Building and Submitting Your Claim

With all the evidence in hand, we assemble a detailed and comprehensive claim package. This isn’t just a number we pull out of thin air; it's a powerful, documented argument for what you are rightfully owed. Using the same industry-standard software the insurance companies use, we create a professional, line-by-line estimate for repairs.

A public adjuster’s claim submission is a comprehensive proof of loss, complete with photographic evidence, detailed estimates, and expert reports. It leaves no room for the insurer to arbitrarily lower the value of your claim.

We then formally submit this package to the insurance company's adjuster, whether they're a staff employee or from an independent adjusting company. A professional submission like this sends a clear signal: this claim will be settled based on facts and policy obligations, not guesswork. You can learn more about the nuts and bolts in our guide to the property damage claim process.

Step 4: Expert Negotiation and Settlement

This is where having an advocate in your corner really pays off. We handle all communications with the insurance company, shielding you from the stress of constant phone calls and requests for information. We meet directly with their representatives to negotiate, using the mountain of evidence we’ve compiled.

Because our arguments are grounded in hard data and an expert understanding of Oregon and Washington insurance law, we can effectively push back against attempts to delay, deny, or underpay your claim. Our only goal is to secure the maximum settlement allowed under your policy.

Once we reach an agreement, we go over the final offer with you to make sure it covers everything. Our success is tied directly to yours—we only get paid when you do. With your approval, the insurer issues the settlement checks, and you finally have the funds needed to rebuild.

Understanding the Cost and Maximizing Your Investment

Let's get right to it. One of the first questions on every homeowner's mind is, "What does it cost to hire a public adjuster?" It’s a crucial question, and the answer highlights a core difference between a public adjuster who works for you and the adjusters sent by your insurance company.

We work on a contingency-fee model, which is the fairest, most client-focused way to handle things.

Simply put, we only get paid a small, agreed-upon percentage of the insurance settlement after we’ve successfully recovered the money for you. There are no upfront fees, no surprise hourly bills, and zero hidden costs. If we don’t get you a settlement, you don’t owe us a dime. This model ensures our goals are perfectly aligned with yours—our success is tied directly to your success, so we’re motivated to fight for every dollar you’re entitled to.

From Cost to Investment: A Real-World ROI Example

It helps to stop thinking of our fee as a "cost" and start seeing it for what it truly is: an investment in expertise. This is an investment that almost always pays for itself, often leaving you with far more money to rebuild your life than you would have had on your own.

Let’s walk through a realistic scenario.

Imagine a fire causes major damage to your home. Your insurance company’s adjuster comes out, assesses the situation, and offers you a settlement of $150,000. It sounds like a lot of money, but you have a sinking feeling it won't be nearly enough to make things right.

This is when you call NW Claims Management for a free consultation. We dig in, poring over every detail of the damage and your policy. We discover the true cost to repair your home and replace everything you lost is closer to $250,000. The insurer’s initial offer was $100,000 short.

We take the lead from there. We build an undeniable, evidence-based claim and negotiate on your behalf, ultimately securing a final settlement of $250,000.

Even after accounting for a standard public adjuster fee, the policyholder walks away with significantly more funds than the insurer's initial offer. This isn't just a bigger check; it's the difference between a partial fix and a complete recovery.

This example shows the powerful return on investment (ROI) that expert representation delivers. You didn’t "spend" money on a fee; you invested in the knowledge needed to unlock the full value of the policy you’ve been paying for. To see the numbers in more detail, check out our full breakdown of what a public adjuster costs.

Why Expert Guidance Matters More Than Ever

Having an expert on your side is becoming essential in today's increasingly complex insurance world. The market is dominated by independent agents who write 61.5% of all property and casualty insurance policies. These agencies saw a record 10.7% organic growth in 2025, according to the 2025 Best Practices Study.

This rapid growth means policies are constantly changing and becoming more complicated, making it nearly impossible for the average homeowner to keep up. With an expert from NW Claims Management in your corner, you have someone who can decipher the fine print and ensure the payout you receive truly reflects the coverage you paid for.

How to Spot Red Flags When Choosing an Adjuster

After a fire, flood, or any other property disaster, you’re in a vulnerable position. The decision of who to hire to manage your insurance claim is one of the most critical financial choices you’ll make. A great public adjuster can be your lifeline, but a bad one can turn a disaster into a nightmare. Knowing the warning signs is your best defense.

The most obvious red flag is a hard sell. If someone shows up on your doorstep uninvited right after a loss, pressures you to sign a contract immediately, or uses scare tactics, show them the door. A true professional understands you need time and space to think clearly. They'll offer guidance, not pressure.

Another huge warning sign is a promise of a specific settlement amount. Think about it—how could anyone guarantee a result before they've even dug into the details of your damage and combed through your policy? Ethical adjusters don't make promises they can't keep. It's not just unprofessional; it's a breach of industry ethics.

Verifying Legitimacy and Experience

Before you sign anything, your first move should always be to check their credentials. Any legitimate public adjuster must be licensed by the state to represent you. For claims here in the Pacific Northwest, that means they need a valid public adjuster license from either the Oregon Division of Financial Regulation or the Washington State Office of the Insurance Commissioner.

Don't just take their word for it. Ask for their license number and verify it yourself on the state’s website. If they get defensive or can’t provide it, that’s not just a red flag—it means they’re likely operating illegally.

Beyond the license, look for signs of a stable, professional operation. Does the independent adjusting company have a real office, or do they seem to work out of their truck? A firm with roots in the community, a physical address, and a history of positive client reviews is always a safer bet than a "storm chaser" who might disappear once the work is done.

The Problem of Inexperienced Adjusters

The insurance claims world is under a lot of strain right now. The profession is actually projected to shrink by 5% between 2024 and 2034. In response, many of the large adjusting firms that work for insurance companies are throwing new, inexperienced adjusters at a high volume of claims, especially after a catastrophe. This industry trend, as you can discover more about this industry trend, often leads to a "race to the bottom" where the quality of the investigation suffers.

This is exactly why having a dedicated public adjusting firm on your side is so important. We work only for you, the policyholder. Your claim gets the detailed, expert attention it deserves, instead of being just another file in a mountain-high stack.

A public adjuster's value is measured by their expertise, strategy, and unwavering loyalty to their client. Be cautious of any firm that seems more focused on volume than on your specific outcome.

Poor communication is another classic sign of trouble ahead. If you’re having trouble getting ahold of the adjuster, they aren't giving you clear updates, or they can't explain what they're doing and why, it’s a good sign your claim isn’t their priority. A good public adjuster acts as your partner, keeping you in the loop every step of the way.

It’s also important to remember who you're up against. The insurance company's adjuster is trained to protect their employer's bottom line. Be on the lookout for the common insurance adjuster tricks they use to minimize payouts—a skilled public adjuster will know how to counter these tactics.

Vetting Your Public Adjuster Checklist

Before bringing a public adjuster onto your team, it's crucial to do your homework. A few pointed questions can reveal a lot about their experience, professionalism, and whether they're the right fit for your claim.

The table below provides a simple checklist to guide you through the vetting process. Use these questions to ensure you're hiring a licensed, reputable, and experienced advocate.

| Verification Step | What to Look For | Why It Matters |

|---|---|---|

| License & Insurance | A valid state-issued public adjuster license number and proof of E&O insurance. | An unlicensed adjuster is illegal and offers no protection. Insurance protects you if they make a critical error. |

| Relevant Experience | A track record of handling claims similar to yours (e.g., fire, water damage, commercial). | Every type of loss has unique complexities. You want an expert in your specific type of damage. |

| Client References | Willingness to provide names and numbers of recent, local clients. | Past performance is the best predictor of future results. Speaking to a real client is invaluable. |

| Contract Review | A clear, easy-to-understand contract with a transparent fee structure (typically a percentage of the settlement). | You must understand exactly what you’re signing, how the adjuster gets paid, and what your obligations are. |

| Communication Plan | A clear answer on who your main contact will be and how often you can expect updates. | Good communication prevents misunderstandings and ensures you're never left in the dark about your own claim. |

Taking the time to run through these checks provides peace of mind. An honest, experienced public adjuster will not only welcome these questions but will also have confident, clear answers ready for you. Their responses will tell you everything you need to know about their ability to fight for your recovery.

Common Questions About Public Adjusting Companies

When your property is hit with a disaster, your head is spinning with a million questions. On top of figuring out repairs, you’re probably wondering if hiring a public adjuster is the right move. It’s a big decision, and you deserve clear answers.

Let’s walk through the questions we hear most often from homeowners and business owners in Oregon and Washington. Our goal is to give you the information you need to take back control of your claim.

Can I Hire a Public Adjuster if My Claim Is Already Started?

That's a situation we see all the time. The short answer is yes, absolutely. Many of our clients come to us weeks or even months into their claim, usually because they’re frustrated with delays or have received a settlement offer that just doesn’t add up.

You have the right to bring in a public adjuster at any point before you sign a final settlement release. It doesn't matter if you just filed or feel like you've hit a complete brick wall with your insurer.

Once we’re on board, our first move is a full-scale audit of your claim. We dig into every piece of correspondence, scrutinize the insurance company's damage reports, and review your policy line by line. From that point on, we handle all the negotiations to get your claim back on track and fight for the settlement you’re truly owed.

Will My Insurance Company Drop Me for Hiring a Public Adjuster?

This is a huge fear for many policyholders, but the answer is a firm no. It is completely illegal for your insurance provider to drop your policy, jack up your rates, or penalize you in any way for hiring a licensed public adjuster.

Hiring a public adjuster is a protected right for policyholders. Think of it this way: you wouldn't be punished by the court for hiring a lawyer to represent you. In the same way, you can't be punished for bringing in a professional advocate to manage your insurance claim.

Your insurance company knows we will hold them accountable to the terms of the policy they wrote. While this means they can't get away with underpaying your claim, they cannot legally retaliate against you for seeking expert help.

Any insurer who tries to do so is acting in bad faith, which opens them up to serious legal trouble and financial penalties.

What Types of Claims Do You Handle?

We specialize in major property damage claims for homes, businesses, and even nonprofit organizations throughout Oregon and Washington. Our team is built to handle the complex, high-stakes situations where a mistake can cost you dearly.

We manage everything from catastrophic events to more common property disasters, including:

- Fire and Smoke Damage: Whether it’s a kitchen fire or a total loss, we document the full scope of damage from flames, invasive smoke, and corrosive soot.

- Water and Flood Damage: We handle the chaos that comes from burst pipes, failed appliances, storm flooding, and other major water intrusions.

- Storm and Wind Damage: This covers everything from trees falling on a roof to severe winds that tear away siding—events all too common in the Pacific Northwest.

- Vandalism and Theft: We help property owners meticulously document and recover the costs of malicious damage or significant theft.

- Building Collapse: For the most severe structural failures, we manage the incredibly complex claims process from start to finish.

If your property has suffered serious damage and the claim feels like too much to handle, chances are we have the expertise to help.

Is My Claim Big Enough for a Public Adjuster?

That's a really smart question. Generally, if the damage is complex or the repair costs are high enough to cause you real financial pain, a public adjuster is a wise move.

It’s not about a "magic number." It’s about the details. Insurers often underpay claims by thousands—sometimes tens of thousands—of dollars simply by overlooking hidden damage or pricing repairs with low-quality materials. Any claim involving structural work, widespread smoke damage, or significant water intrusion almost always benefits from a professional eye.

We will only take on your case if we are confident that our involvement can add significant value to your final settlement, even after our fee is accounted for.

That’s why we always start with a free, no-obligation claim review. We’ll give you an honest take on your situation. If we think you've got it handled and can manage the claim effectively on your own, we'll tell you that. Our job starts with giving you good advice.

When you're facing a complicated insurance claim, you don't have to go it alone. The expert team at NW Claims Management is here to fight for you. If you need a powerful advocate in your corner, contact us today for a free evaluation of your claim.