An employee twists a knee lifting inventory, or a driver gets hurt on a delivery run, and your day changes fast. You’re no longer just running payroll, serving customers, or keeping crews scheduled. You’re dealing with medical care, state rules, insurance communication, wage replacement questions, and a worker who may be anxious about pain, income, and job security.

That’s where workers compensation claims management stops being a paperwork task and becomes an operating discipline.

Handled poorly, a claim drifts. People stop communicating. Work status gets missed. The adjuster makes decisions with incomplete facts. The employee feels ignored. Costs rise at the same time trust falls. Handled well, the process does two things at once. It protects the employer from unnecessary expense, and it gives the injured worker a fair, steady path back to stability.

That balance matters in Oregon and Washington. Both states expect employers to take reporting, documentation, and return-to-work obligations seriously. But beyond compliance, there’s a business reality. A claim affects staffing, morale, overtime, productivity, and future insurance costs. It also affects whether your employee feels like the company stood by them when something went wrong.

Many owners make the same mistake at the start. They assume the carrier will handle everything correctly, so they step back too far. That’s often when confusion starts, and it’s one reason business owners end up learning about insurance adjuster tricks only after a claim has already become harder to control.

Good claims management isn’t hard because it’s mysterious. It’s hard because it requires quick action, disciplined follow-up, and empathy at the same time. If you can do those three things consistently, you’ll make better decisions for your company and for the injured employee depending on you.

Introduction Beyond the Paperwork

The first hours after an injury usually feel messy. A supervisor is trying to figure out what happened. The employee may need medical care. Someone in payroll is wondering whether time loss applies. The owner is asking whether this is a minor incident or the start of a major claim.

That uncertainty is normal. What matters is what you do next.

The real job after an injury

A workers compensation claim creates two separate responsibilities that have to run together.

One is financial control. You need accurate reporting, prompt investigation, clean documentation, and a plan for modified duty if restrictions come back. If you don’t manage those pieces, the file gets more expensive than it should.

The other is human support. The injured worker needs clarity. They need to know who to call, what happens next, whether their wages are protected, and whether they still have a place in the organization. Silence from the employer often gets interpreted as indifference.

Practical rule: The claim usually gets harder, not easier, when the employee feels abandoned.

Why owners get pulled in even if they don’t want to

You can delegate tasks. You can’t delegate accountability.

The insurer has its role. The adjuster has a role. The treating provider has a role. But the employer still controls critical facts, workplace context, wage information, job duties, and modified work options. Without that input, even a capable adjuster is operating with gaps.

That’s why strong workers compensation claims management isn’t passive. It’s coordinated. The employer stays involved without micromanaging the file.

What good handling looks like

At a practical level, a well-managed claim usually includes:

- Fast reporting: The claim gets reported quickly, with enough detail to be useful.

- Consistent contact: The employee hears from the employer early and regularly.

- Work status tracking: Restrictions, appointments, and next steps don’t disappear into voicemail.

- Claim oversight: Someone checks that the claim is moving and that decisions make sense.

- Return-to-work planning: Light duty isn’t treated as an afterthought.

If you build those habits, you’ll avoid a lot of preventable trouble before it starts.

Understanding the Players and Key Terms

Confusion usually starts with language. Owners hear terms like indemnity, reserves, compensability, or MMI and assume the carrier is speaking a different dialect. The easiest fix is to treat a claim like a project team. Each person has a function, and each term tells you what part of the project is being discussed.

A claim can be small, or it can become very costly. Analysis of over 150,000 claims found that 83% were medical-only, while the average cost for all lost-time claims was $44,179, and severe injuries such as amputations averaged over $120,000 per claim according to this workers' compensation claims analysis. That’s why knowing who does what is not academic. It affects money quickly.

Who is on the claim team

| Role | Primary Responsibility |

|---|---|

| Employer | Report the injury, provide job and wage information, document facts, maintain contact, and explore modified duty |

| Injured employee | Report the injury, follow medical advice, attend treatment, communicate work status, and cooperate with the process |

| Insurance carrier or state fund administrator | Administer the claim, evaluate coverage and compensability, issue benefits when owed, and manage claim handling |

| Claims adjuster | Investigate facts, gather records, coordinate benefits, evaluate exposure, set reserves, and move the file toward resolution |

| Medical provider | Diagnose injury, treat the worker, issue restrictions, and document functional ability |

| Employer advocate or counsel when needed | Review strategy, challenge weak handling, and help the employer stay aligned with its rights and obligations |

Key terms in plain English

Medical-only and lost-time claims

A medical-only claim is what it sounds like. The claim pays for treatment, but the worker doesn’t miss enough time from work to trigger wage replacement under the claim structure.

A lost-time claim involves time away from work and usually much more complexity. Once wages, restrictions, disability questions, and return-to-work barriers get involved, the file takes on a different shape.

Indemnity benefits

Indemnity benefits are wage-replacement benefits. If the worker cannot perform their job because of the injury, indemnity becomes one of the main cost drivers in the claim.

This is why employers who can offer legitimate modified duty often put themselves in a better position. They’re not trying to force someone back. They’re trying to reduce unnecessary lost time while keeping the employee connected to work.

Incurred losses

Incurred losses are the total financial exposure the claim carries at a given point. That usually means what has already been paid, plus what the adjuster has reserved for future payments.

Think of incurred losses as the claim’s running price tag, not just the bill received so far.

Compensability

Compensability is the basic legal question. Is this claim covered under workers compensation based on the facts, the employment relationship, and the jurisdiction’s rules?

Employers should provide facts. They should not guess, exaggerate, or try to force a conclusion.

Maximum Medical Improvement

At some point, the treating providers may conclude the worker has reached Maximum Medical Improvement (MMI). In practical terms, that means the condition has improved as much as expected with treatment, even if the worker still has some limitations or symptoms.

That term matters because it often affects work restrictions, permanent impairment discussions, and settlement posture.

When an owner understands the vocabulary, conversations with the adjuster get shorter, clearer, and more productive.

Where employers lose leverage

Owners tend to lose advantage in three places:

- They stop asking questions once the claim is opened.

- They assume reserves are automatically correct and never review the file’s direction.

- They treat the employee relationship as separate from the claim, when it is central to how the claim develops.

If you know the players and the terms, you’re no longer reacting blindly. You can participate with purpose.

For a broader perspective on the difference between advocates working for policyholders and those working for insurers, this overview of public adjuster vs insurance adjuster is useful background, even though workers comp has its own rules and structure.

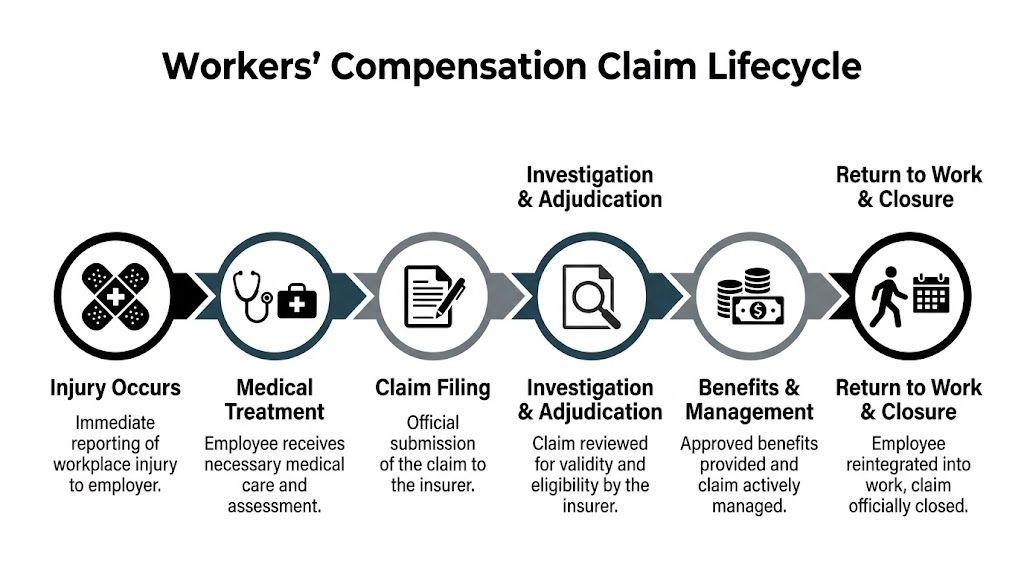

The Claim Lifecycle From Injury to Closure

Most claims follow a recognizable path. The details vary, but the stages don’t. If you know the sequence, you can usually tell whether the file is progressing or stalling.

Stage one after the injury

The employer’s first priority is immediate care and scene response. Make sure the worker gets appropriate medical attention. Secure the area if there’s a continuing hazard. Identify witnesses while events are still fresh.

Then document the basic facts. What was the employee doing? Where did it happen? Who saw it? Was equipment involved? Was there a prior complaint or similar incident?

The goal is not to build a courtroom file on day one. The goal is to preserve facts before memory gets fuzzy.

Medical treatment and work status

After initial treatment, the next operational question is work status.

Can the employee return to regular duty? Modified duty? No work for now? That information drives scheduling, wage exposure, and planning. It also shapes the employee’s confidence in the process. If nobody asks for restrictions or follows up, the worker often ends up sitting at home longer than necessary.

Filing the claim

The claim needs to be reported accurately and quickly. That includes the injury description, body part, date, time, witnesses, employer contact, and wage information where required.

This step sounds basic, but poor reporting causes real damage. If the injury description is vague, if dates are wrong, or if the employer leaves out prior context, the adjuster starts the file with a blurry picture.

Investigation and adjudication

Once the claim is reported, the adjuster investigates.

That may include statements, medical records, employment information, and jurisdictional review. If the claim is straightforward, this stage may move cleanly. If there are inconsistencies, prior conditions, late reporting, or factual disputes, the file can slow down quickly.

This is also where the employer’s responsiveness matters. The adjuster can’t evaluate what the employer never provides.

A claim investigation works best when the employer gives facts quickly and avoids editorializing. Clear facts are more useful than emotional opinions.

Active management while the claim is open

Once accepted or actively processed, the claim enters the part many employers under-manage.

Medical care continues. Work restrictions may change. Time-loss issues may develop. The adjuster may set reserves and revise them as more information comes in. The employer should stay in contact with the worker and keep checking whether productive modified duty is available.

This stage benefits from a simple rhythm:

- Check current restrictions: Don’t rely on an old note.

- Confirm the next appointment: Open claims drift when nobody knows what’s scheduled.

- Review whether modified duty fits current limitations: A stale job offer doesn’t help.

- Flag inconsistencies early: If work status and treatment don’t line up, raise the question promptly.

Return to work

The cleanest claims usually involve a structured return-to-work path.

That doesn’t always mean full duty right away. Sometimes it means temporary administrative tasks, adjusted schedules, lighter lifting, or alternate assignments that respect medical restrictions. The best return-to-work offers are specific. They describe duties, hours, supervisor, and physical expectations clearly enough for the provider and worker to evaluate.

Compassion matters here. Modified duty should not be punitive or fake. If the employee feels the company is inventing meaningless work just to cut benefits, the relationship worsens fast.

Closure

Claims close when treatment ends, wage issues resolve, and the file no longer requires active benefits or dispute handling. Some claims close cleanly. Others stay open because of ongoing treatment, impairment issues, litigation, or unresolved work capacity questions.

Before the file closes, the employer should check a few things:

| Closure checkpoint | Why it matters |

|---|---|

| Current work status is documented | Avoids confusion about whether the employee can work |

| Final restrictions are clear | Helps with placement and future supervision |

| Claim notes and internal files are complete | Useful if the claim reopens or questions arise later |

| Safety lessons are captured | Prevents repeat injuries from the same condition |

If the claim takes a turn toward denial, dispute, or inconsistent handling, it helps to understand the practical issues involved in how to fight insurance claim denial, especially when facts and documentation support a stronger position than the initial response suggests.

Best Practices for Proactive Claims Management

Reactive employers spend more. They usually don’t mean to. They just wait too long to report, communicate too little, and treat return-to-work planning as something to think about later. By then, the file already has momentum in the wrong direction.

Proactive handling gives you a better chance to control cost without treating the employee like a problem to manage.

Industry guidance is clear on one point. Reporting quickly matters. Claims reported within 24 hours achieve 15% to 25% higher return-to-work ratios and lower overall expenses according to this discussion of lag time and workers comp interventions. That isn’t just an administrative win. It changes medical direction, communication, and the worker’s experience from the start.

Start with reporting discipline

If your supervisors are still deciding whether an injury is “serious enough” to report, your process is weak.

The better standard is simple. If an employee says they were hurt at work, treat it as reportable internally right away and let the proper claims process sort out the rest. Delays create factual gaps, late medical direction, and distrust.

A strong reporting process includes:

- Named responsibility: One person reports the claim, and one backup is assigned.

- A standard form: Supervisors shouldn’t build narratives from memory.

- Witness capture: Get names and brief statements while details are fresh.

- Same-day escalation: Don’t let incidents sit until the next payroll cycle.

Communicate like the employee matters

The employer’s tone after an injury affects the claim more than most owners realize.

An injured worker usually wants four questions answered quickly. Are you okay. What happens now. Who is handling this. Is my job still there if I follow the rules. If nobody answers those questions, attorneys and frustration often fill the silence.

That doesn’t mean calling every day. It means being consistent and useful.

“We’re going to stay in touch, make sure the paperwork gets handled, and talk through work options when your doctor gives restrictions.”

That kind of message lowers anxiety without making promises you can’t keep.

Build return-to-work before you need it

The worst time to design modified duty is after someone gets hurt.

Employers who handle claims well usually have a short list of temporary tasks already identified. That list may include inventory reconciliation, vehicle inspections, training support, clerical work, jobsite documentation, quality control checks, or other restricted-duty assignments that still provide value.

A return-to-work program works better when it does three things:

| Program element | What works |

|---|---|

| Written duties | Specific tasks tied to actual restrictions |

| Provider communication | Clear description of physical demands |

| Internal supervision | A manager who knows the assignment is temporary and purposeful |

If your business has winter exposure, delivery exposure, or outdoor work, planning ahead matters even more. Seasonal incidents can create preventable claims, and a plain-language resource on a slip and fall on ice at work can help employers think through how these accidents develop and how liability and injury issues can get complicated fast.

Pay close attention to first-year employees

New employees get hurt more often than many employers expect. A Travelers study found that 35% of all workplace injuries occur during an employee’s first year on the job, leading to over 6 million missed workdays annually and accounting for 32% of total workers’ compensation claim costs, as summarized in this review of workers comp safety and data analysis considerations.

That should change how you onboard.

Don’t treat first-week safety training as a stack of signatures. New workers need repetition, observation, and correction in the actual work environment. In Oregon and Washington businesses, that often means showing the route, the equipment, the lifting standard, the weather exposure, the housekeeping expectations, and the reporting path for near misses and injuries.

What active employers do differently

They don’t just file and hope. They stay in the file enough to keep it moving.

In practical terms, that means:

- They review restrictions promptly

- They follow up after medical appointments

- They challenge unclear next steps

- They coordinate with payroll and operations

- They make early decisions instead of late excuses

What doesn’t work is a passive posture where the employer assumes the adjuster will notice every issue, solve every communication problem, and create every return-to-work opportunity. The carrier can administer a claim. The employer still shapes the outcome.

If a claim starts pulling you into a broader dispute with an insurer over how a matter is being handled, it helps to understand the practical side of negotiating with insurance company representatives so you don’t lose your advantage through delay, poor documentation, or loose communication.

Measuring What Matters With KPIs and Technology

Many employers say they want better claim outcomes, but they don’t track the signals that show whether the program is improving. Good workers compensation claims management gets sharper when you measure it.

The most useful approach is not a giant dashboard full of vanity metrics. It’s a short scorecard tied to specific operating decisions.

The KPI most owners overlook

Start with incurred losses.

In workers compensation, incurred losses represent paid amounts plus future reserves. Rigorous tracking and accurate data entry within 72 hours can keep costs from spiraling, and the top 15% of claims often drive 85% of total expenses according to this discussion of workers comp claim handling best practices.

That matters because many employers focus only on what has already been paid. The larger issue is often sitting in reserves.

A practical scorecard

Track a small set of metrics that your team can review monthly.

Lag time

This is the number of days between injury and claim reporting.

If lag time stretches, your process is weak at the supervisory level. That usually points to training, escalation, or accountability problems.

Return-to-work rate

This shows how often injured employees return to some form of work when medically appropriate.

A weak rate often means the employer has no real modified-duty inventory or fails to communicate with providers and workers effectively.

Open claim count

This is simple but useful. How many claims remain open, and for how long?

A growing pile of aging claims often signals stalled treatment, weak follow-up, or unresolved disputes.

Average cost per claim

This helps identify whether your claims are becoming more severe, more prolonged, or less controlled.

You don’t need elaborate analytics to use this. You need clean claim categories and consistent internal review.

Use technology for triage, not abdication

Claims software, RMIS platforms, carrier portals, spreadsheets, and calendar reminders all have a place. The right tool is the one your team will use every week.

Technology helps when it does one of these jobs well:

- Flags stale claims: No recent appointment, no updated work status, no next action.

- Tracks restrictions: So modified work offers match the current medical note.

- Supports dashboards: So ownership can see trend direction without waiting for renewal season.

- Improves file accuracy: Better coding and cleaner records help prevent reserve and handling errors.

Some organizations also use AI-driven triage and claim monitoring. That can be useful, especially on complex files. The benefit is not that software “solves” claims. The benefit is that it spots developing trouble sooner.

Good technology shortens reaction time. It does not replace judgment.

What to review in a monthly claim meeting

A monthly review should be short and direct. It should not become an abstract finance exercise.

Use questions like these:

| Monthly review question | Business reason |

|---|---|

| Which claims are aging without a clear next step | Stalled files usually get more expensive |

| Which employees have restrictions we can accommodate | Reduces avoidable lost time |

| Which reserves look out of line with current facts | Prevents distorted loss picture |

| Where did reporting break down | Fixes process, not just individual claims |

A lean KPI process gives owners something better than guesswork. It gives them a way to see whether claim handling is disciplined, whether employee support is consistent, and where preventable cost is entering the system.

Oregon and Washington State Compliance You Must Know

Oregon and Washington employers need more than general workers comp advice. They need a process that fits state rules, state forms, and state agency expectations. The exact handling details depend on your industry, your carrier arrangement, and the facts of the claim, but some practical obligations are constant.

Oregon basics that deserve attention

In Oregon, injury reporting and documentation need to happen quickly and cleanly. Employers should be familiar with the 801 Form process and make sure supervisors know how incidents get escalated internally the same day they’re reported.

A practical Oregon checklist looks like this:

- Immediate injury response: Get care first, then preserve facts.

- Internal notice path: Supervisors should know who receives injury reports and who submits required documentation.

- Accurate wage and job information: Missing or sloppy payroll data can complicate time-loss handling.

- Modified-duty planning: If restrictions are issued, the employer should review whether temporary work is available and document the offer clearly.

- Record retention: Keep your incident notes, witness details, and communication log organized in one place.

Oregon employers also need to resist the temptation to treat minor injuries casually. A claim that looks small on day one can become more serious if care, work status, or reporting gets mishandled.

Washington rules often create process mistakes

Washington employers need a similarly disciplined process, but the administrative flow can feel different depending on whether the claim sits with the state system or another arrangement.

For many employers, the key issue is not legal complexity. It’s execution. Washington claims often get harder when:

- Medical restrictions aren’t reviewed quickly

- The employer delays communication after the first report

- Job offers are vague or undocumented

- No one tracks whether a worker could participate in a Stay at Work style return-to-work approach

What both states reward

Oregon and Washington both favor employers who do the basics well.

Document facts early

Don’t rely on memory three weeks later. Names, times, tasks, equipment, and initial symptoms should be written down while they’re still clear.

Match job offers to restrictions

A vague promise of “light duty” isn’t enough. The work has to be described in a way the provider and employee can evaluate.

Keep communication respectful

Injured workers are more likely to stay engaged when they understand the process and feel they’re being treated fairly.

In both states, a compliant claim is usually a well-organized claim. Deadlines, forms, and work-status records matter because they shape everything that follows.

A practical compliance habit

Assign one internal owner for claims coordination, even if several people contribute information.

That person doesn’t need to be a lawyer. They need authority to gather facts, submit documents, communicate with the adjuster, track restrictions, and make sure Oregon or Washington deadlines don’t get lost between departments. One accountable coordinator prevents a lot of avoidable confusion.

Common Pitfalls and When to Engage an Expert

A lot of employers still assume this: once the claim is reported, the carrier will handle it correctly from there.

Sometimes that works. Sometimes it doesn’t.

The blind spot is not just adjuster performance. It’s employer disengagement. A common problem is failing to hold the adjuster accountable through active claim reviews, timelines, and oversight of questionable treatment approvals, which can inflate claim costs, as noted in this discussion of how employers can minimize workers comp claim pitfalls.

The mistakes that keep showing up

Most costly errors are not dramatic. They’re ordinary lapses repeated over time.

Poor employee communication

The worker hears from the company once, right after the injury, then nothing. That vacuum creates frustration and suspicion.

Weak investigation

Nobody gathers witness accounts, checks equipment facts, or pins down what happened while memories are fresh. Later, the employer is stuck arguing from incomplete notes.

Passive return-to-work handling

The employer says they support modified duty, but no one identifies tasks, sends a written offer, or follows up after restrictions change.

No reserve or file oversight

The adjuster’s decisions may be reasonable, but no one from the employer side asks whether the file direction still matches the facts.

Red flags that mean you should get help

Some claims are bigger than an in-house coordinator or busy owner should manage alone.

Consider outside expertise when you see any of these conditions:

- Attorney involvement: The file has become adversarial.

- Severe injury: Brain, spinal, amputation, multi-body-part, or other high-exposure claims need closer strategy.

- Disputed treatment or causation: The medical picture is no longer straightforward.

- Long duration without progress: The employee is not moving through care or return-to-work in a stable way.

- Questionable handling decisions: Approvals, denials, reserves, or communication patterns don’t line up with the facts.

- Oregon or Washington compliance concerns: You’re worried that documentation, deadlines, or work offers may be off track.

What an expert should do for you

An outside expert should bring order, not noise.

They should review the file, identify what is driving cost, spot procedural or strategic errors, clarify next actions, and help you communicate in a way that protects both the business and the injured worker. If all they do is criticize the adjuster without building a plan, they aren’t adding much value.

The right time to bring in help is before the claim becomes unmanageable, not after everyone is arguing.

If you’re weighing that decision, this guide on when to hire a public adjuster is worth reading for the broader principle involved. You don’t need outside representation on every claim, but you do need to recognize when the stakes, complexity, or resistance justify another set of experienced eyes.

If you’re in Oregon or Washington and you’re dealing with a difficult claim, confusing insurer communication, or a broader insurance dispute affecting your property or operations, NW Claims Management offers policyholder-side advocacy built around documentation, negotiation, and practical guidance. For owners, nonprofits, municipalities, and commercial policyholders who need clarity and strong representation, that kind of support can make a complicated claim far more manageable.