A storm tears through your property. Or a pipe fails inside a wall. Or a fire leaves part of the structure standing, but no one agrees on whether the framing is still safe. You file the insurance claim expecting help. Instead, you get a familiar answer: the carrier says the damage is limited, old, excluded, or not caused the way you described.

That’s the moment many property owners in Oregon and Washington realize the dispute isn’t only about cost. It’s about cause.

When cause is disputed, the forensic engineer job becomes very important. A forensic engineer is the professional who investigates how and why a building element, system, or component failed. For a homeowner, business owner, school, church, or nonprofit, that work can mean the difference between a partial payment and a fully supported claim.

Your Guide to the Forensic Engineering Profession

If you’ve never dealt with one before, think of a forensic engineer as a structural detective. Their job is to examine damage, test assumptions, and identify the most defensible explanation for what happened.

That matters because insurance claims often turn on small technical questions. Did wind lift the roofing system first, allowing water in afterward? Did impact damage open the building envelope? Did heat weaken structural members beyond safe reuse? Those aren’t guesswork questions.

The forensic engineer job is also becoming more visible as property losses grow more complex. The global forensic engineering services market was valued at USD 5.1 billion in 2023 and is projected to reach USD 8.1 billion by 2032, with a CAGR of over 5%. North America held over 30% of the global market in 2023, driven in part by complex projects and the need for forensic analysis in insurance claims processes, according to Global Market Insights.

For policyholders, that trend means one simple thing. More claims now require technical proof, not just photos and repair estimates.

If you’re also trying to understand how much coverage may be available before pushing a disputed claim further, it helps to review how insurance policy limits work. Many people focus on damage first and policy structure second, when both matter.

Practical rule: If the insurer is debating why the damage happened, you may need an engineer before you need another contractor bid.

For people considering the profession, the forensic engineer job is demanding, technical, and high trust. For policyholders, it’s often the expert role that turns confusion into evidence.

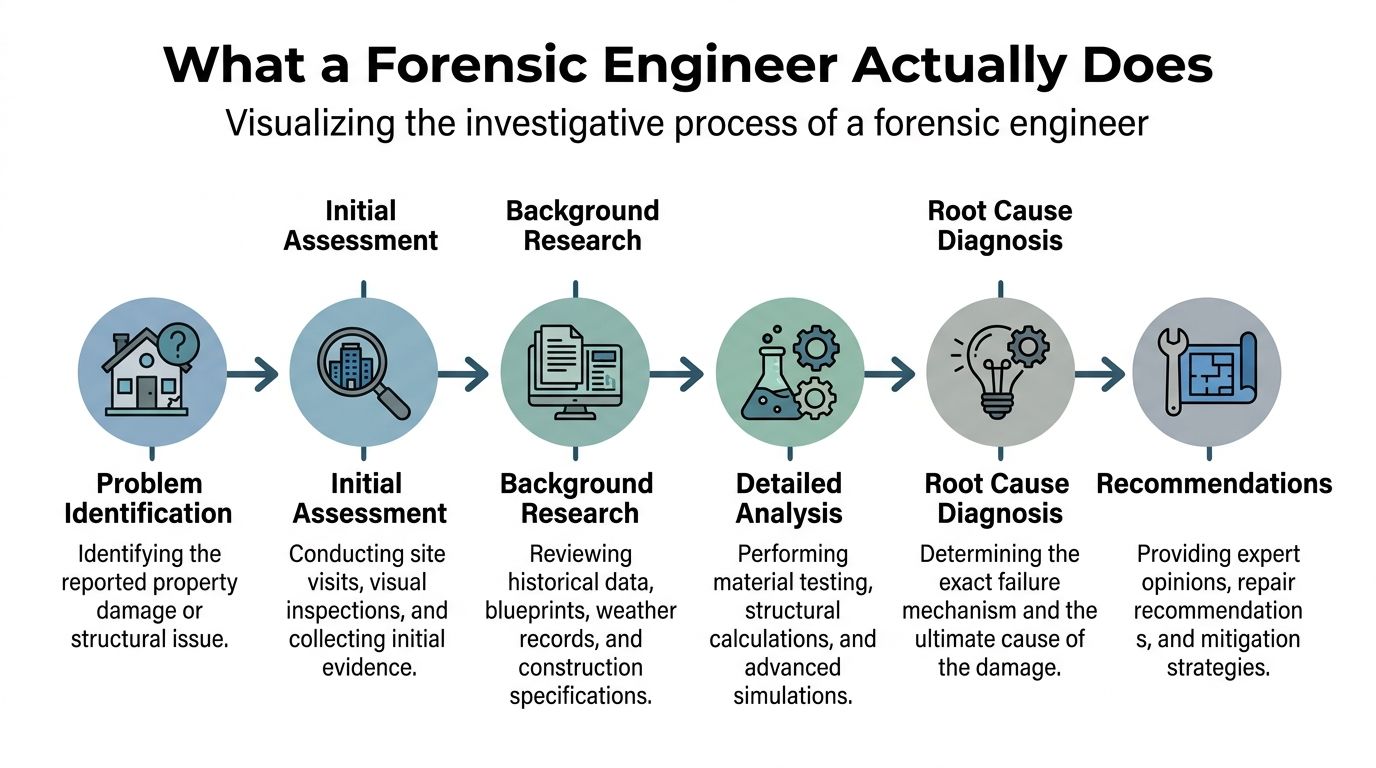

What a Forensic Engineer Actually Does

A lot of people hear “forensic” and think crime lab. In property claims, the work is different. A forensic engineer investigates failure. That could mean a cracked foundation, a collapsed roof section, a burned truss system, warped steel, broken mechanical equipment, or a wall assembly that let water travel where it shouldn’t.

A useful comparison is medicine. A contractor often identifies what needs repair. A forensic engineer identifies why the failure happened.

They start at the scene

The first part of the forensic engineer job is field investigation. The engineer visits the property, observes damage patterns, photographs conditions, measures displacement or deflection, and collects physical clues.

They’re not just looking at what’s broken. They’re asking:

- Where did the failure begin

- What path did the damage follow

- Which materials failed first

- What signs point to sudden damage versus long-term deterioration

- What evidence could disappear if the site is altered too soon

This is one reason policyholders shouldn’t rush demolition before the claim issues are clear. Once key evidence is removed, some causation arguments become harder to prove.

If you’re trying to understand how damage documentation fits into the broader claims process, this overview of property damage assessment helps connect the engineering findings to claim valuation.

They gather the building’s history

A good engineer doesn’t rely on a quick visual impression. They compare what they see on site with records such as plans, repair invoices, prior claim history, product information, site conditions, and event timing.

For a storm claim, they may compare the pattern of uplift, water entry, and component failure. For a plumbing loss, they may study where the break occurred and whether the break looks sudden, pressure-related, freeze-related, or tied to wear.

Sometimes the most important clue is sequence. If the roof assembly failed first and interior water damage followed, that tells a different story than interior moisture from a long-standing leak.

They use technical tools to test causation

The work becomes more scientific than commonly anticipated. Forensic engineers use Finite Element Analysis (FEA) to model how structures or components behave under stress, and fracture mechanics to study how cracks initiate and propagate. That allows them to reconstruct failure events and support causation analysis in property claims, as described by McDowell Owens.

In plain language, they don’t just say, “This looks storm-related.” They can test whether the forces involved are consistent with the observed damage.

A few examples:

| Damage issue | What the engineer may analyze | Why it matters in a claim |

|---|---|---|

| Roof failure | Load path, uplift behavior, fastener patterns | Helps show whether wind initiated the damage |

| Cracking | Crack width, direction, propagation, stress concentration | Helps separate sudden movement from older settlement issues |

| Fire damage | Heat effects on steel, concrete, wood, and connections | Helps determine whether members can remain or must be replaced |

| Equipment failure | Fracture surfaces, installation conditions, operating stress | Helps identify defect, misuse, or event-driven failure |

A homeowner usually sees the end result. The forensic engineer job is to reconstruct the chain of events behind it.

They document findings in a way that holds up

A strong engineer’s report needs to be understandable to non-engineers and defensible under scrutiny. That’s why their work often includes annotated photos, testing results, calculations, diagrams, and a written explanation of how the conclusion was reached.

The best forensic reports don’t hide behind jargon. They connect physical evidence to a conclusion step by step.

In some cases, engineers also review digital evidence gathered during inspections. If drones were used to document roofs, elevations, or inaccessible areas, it can help to understand how onboard systems preserve data. This explainer on a drone flight recorder is useful background if aerial site documentation becomes part of your claim record.

They answer the question everyone argues about

In an insurance dispute, everyone tends to circle the same issue. Was this covered damage or not?

The forensic engineer job exists to answer that question with evidence. Not with emotion. Not with suspicion. Not with a rough guess at the kitchen table.

When the analysis is done correctly, the engineer’s work gives your side something far more powerful than a complaint. It gives you a technical basis for challenging an incomplete claim decision.

The Path to Becoming a Forensic Engineer

Most property owners assume a forensic engineer is just an engineer who changed specialties. That’s partly true, but it leaves out how much experience usually sits behind the title.

This is not an entry-level role. The professional standard typically requires an active Professional Engineering license, often called a P.E., along with 5 to 10 years of design experience. The work also follows a three-part scientific process: field investigation, laboratory analysis, and preparation of a report that must be “clear, concise, cohesive, accurate, and defensible,” according to GeoTech Engineering.

Why licensure matters

A P.E. license tells you the engineer has met professional standards that go beyond general technical familiarity. In a claim dispute, that matters because opinions may be challenged by carriers, opposing experts, mediators, or lawyers.

For a policyholder, the practical takeaway is simple. If someone is being hired to explain structural causation, hidden failure, or repair necessity, credentials aren’t a formality. They’re part of what makes the opinion credible.

Experience comes before specialization

Most forensic engineers first spend years in another engineering lane. Common backgrounds include civil, structural, mechanical, electrical, or materials-related work.

That experience matters because failure analysis depends on knowing how things are supposed to perform before you can explain why they didn’t.

A seasoned forensic engineer has usually spent years with details like:

- Structural systems: How beams, columns, diaphragms, and connections transfer load

- Building envelopes: How roofing, flashing, cladding, and waterproofing should keep water out

- Mechanical components: How equipment is installed and how it fails under abnormal stress

- Construction practice: What workmanship issues look like compared with sudden event damage

Writing is part of the job

People often picture site inspections and testing, but one of the hardest parts of the forensic engineer job is writing the final opinion clearly enough that non-engineers can follow it.

That report may be read by an adjuster, attorney, contractor, property owner, mediator, or judge. If the logic is sloppy, the technical skill won’t carry the day.

What homeowners often miss: A forensic engineer isn’t just trained to inspect damage. They’re trained to explain damage in a way that can survive dispute.

What this means for policyholders

When you hire a qualified forensic engineer, you’re not hiring someone fresh out of school to take a look around. You’re hiring a licensed professional whose work is expected to withstand serious challenge.

That’s why a careful engineer may seem methodical, cautious, or slower than you’d like at first. They’re building an opinion they can defend.

For worried owners, that’s good news. The higher the standard for the professional, the harder it is for an unsupported insurance position to stand if the evidence points somewhere else.

A Forensic Engineer Job in Oregon and Washington

In Oregon and Washington, the forensic engineer job has a very practical regional focus. Property losses here often involve weather exposure, moisture intrusion, fire damage, slope or foundation concerns, and structural questions tied to aging buildings, newer complex assemblies, or hard-to-access roof systems.

For people entering the field, the work can come through consulting firms, architectural and engineering companies, government-related roles, and specialized investigation practices. For property owners, that means the expertise isn’t abstract. Forensic engineering is a recognized profession in the Pacific Northwest.

What the employment picture suggests

Exact Oregon and Washington figures are limited, but related national benchmarks show why this profession keeps drawing attention. The U.S. Bureau of Labor Statistics says forensic science technician roles are projected to grow 13% from 2024 to 2034, while the average for all occupations is 3%. The same BLS source notes about 2,900 annual openings in that related category and places the median annual wage at $67,440 for forensic science technicians as of May 2024. Broader proxy data cited alongside that source also notes 19,450 forensic engineers employed nationally, with a median of $75,260 annually or $36.18 per hour. Key employers include local governments, state governments, and architectural or engineering firms, according to the BLS occupational outlook page.

That national picture helps explain why Oregon and Washington property owners can usually find engineers with claim-related experience, even if the local niche is smaller than in some larger metro markets.

Where forensic engineers work in the region

The work environment is more varied than people expect. A forensic engineer might inspect a coastal building after wind-driven rain damage one day and review a fire-damaged commercial structure inland the next.

Common regional settings include:

- Residential claims: Roof failures, framing movement, hidden water paths, fire-related structural questions

- Commercial losses: Multi-unit buildings, warehouses, retail centers, offices, and mixed-use structures

- Public and nonprofit property: Schools, churches, municipal buildings, and community facilities

- Consulting assignments: Cause-and-origin evaluations, repair scope support, and dispute analysis

Salary and specialization

Compensation can vary widely by market and specialization. Nationally, the benchmark above gives a median figure, but specialized urban markets can run much higher. In the verified data, New York examples reached $118,000 to $140,446, which shows how much compensation can rise where demand and specialization are intense.

That doesn’t mean Oregon and Washington will mirror those exact figures. It does mean the forensic engineer job rewards advanced expertise, especially when the engineer can handle complex building failures, communicate clearly, and produce defensible reports.

Why this matters to local property owners

When a homeowner or business owner hears “engineer,” they often think of new construction. In claims, the engineer’s role is different. They help answer whether the observed damage is tied to a covered event, whether the structure remains sound, and what repairs are required.

In Oregon and Washington, where claims often involve layered water intrusion, storm exposure, smoke or heat effects, and disputed structural impacts, that’s not a luxury opinion. It can be the opinion that moves the file.

A local policyholder doesn’t need to become an engineer. But it helps to understand that the forensic engineer job in this region sits at the intersection of technical building knowledge and real-world claim conflict.

Why Your Insurance Claim Might Need a Forensic Engineer

Insurance companies rarely frame a dispute the same way a property owner does. You see a damaged building and an urgent need to recover. The carrier often starts with a narrower question: can part of this damage be explained away?

That’s where the partnership between a public adjuster and a forensic engineer becomes so valuable. It’s also the part most articles skip. Many discussions of the forensic engineer job focus on work for insurers or attorneys, but they often miss how engineers can provide independent assessments for policyholders, especially after fires, floods, and storms, as noted in this discussion of the content gap around forensic engineer roles and insurance claims.

Where insurers often push back

In a complex loss, the insurer may not deny the whole claim outright. More often, it narrows the accepted cause or limits the scope of repair.

That can sound like:

- Pre-existing condition: The carrier argues the crack, movement, staining, or deterioration was already there

- Wear and tear: The insurer says the damage came from aging, maintenance issues, or gradual decline

- Excluded peril: The file is steered toward earth movement, faulty workmanship, long-term seepage, or another exclusion

- Limited repair scope: The insurer accepts some damage but says structural replacement or invasive repair isn’t necessary

Those positions can be hard to challenge with photos alone. A soaked ceiling tells you something happened. It doesn’t always prove why.

A forensic engineer changes the argument

Once an independent engineer is involved, the discussion shifts from opinion to mechanism. The report may identify the sequence of failure, the load path, the crack progression, the heat effect, or the water entry route.

That matters because claims aren’t won by saying, “I know this house.” They’re won by showing, “Here is the evidence, and here is why the evidence supports covered causation.”

Consider a few common examples.

Storm loss

A carrier may say water entered because the roof was already worn. An engineer may find that wind damaged the roofing system first, creating an opening that let water in.

Fire loss

The insurer may focus on visible charring and propose limited repair. An engineer may determine that heat exposure compromised structural members or connections beyond safe reuse.

Plumbing or water loss

The carrier may characterize the condition as long-term leakage. An engineer may identify a sudden failure mode in a component or show that the pattern of damage is inconsistent with slow, historic seepage.

When causation is the dispute, a good engineering report often matters more than another estimate.

Why public adjusters and engineers work so well together

A public adjuster and forensic engineer do different jobs. That’s exactly why the partnership is powerful.

Here’s the distinction:

| Role | Primary focus | Output |

|---|---|---|

| Public adjuster | Policy interpretation, loss documentation, valuation, negotiation | Claim strategy and settlement presentation |

| Forensic engineer | Cause analysis, structural findings, technical documentation | Defensible causation and repair-support opinion |

The public adjuster builds the claim. The engineer supports the parts that require technical proof.

This is especially important when you’re comparing your own representation against the carrier’s team. If you want a clearer picture of that imbalance, this explanation of public adjuster vs insurance adjuster is worth reviewing.

Why this matters in Oregon and Washington

Pacific Northwest claims often involve moisture, layered building assemblies, roof systems, hidden decay questions, smoke movement, and storm-related openings that aren’t obvious at first glance.

That creates room for disagreement.

A worried owner may hear, “We’ll pay for some interior drying, but not the roof system.” Or, “We’ll patch that area, but there’s no proof the framing was affected.” An engineer can test those assumptions.

Sometimes the value of the forensic engineer job isn’t dramatic courtroom testimony. Sometimes it’s much simpler. It’s a careful report that prevents the insurer from shrinking a serious structural issue into a cosmetic repair.

One practical note for water losses

If your claim involves water damage, it helps to combine legal, technical, and emergency-response thinking early. This guide to essential water damage insurance claim tips is a useful companion resource because it covers practical claim handling issues that often arise before the technical dispute is fully developed.

When you should think about bringing one in

You should start considering a forensic engineer when any of these are true:

- Cause is disputed: The insurer questions whether the reported event caused the damage

- Hidden structural issues are possible: The visible damage may be only part of the loss

- Repair scope is being minimized: The carrier accepts minor repairs but resists deeper investigation

- The property is high value or mission critical: Commercial, nonprofit, municipal, or multi-unit losses often need stronger technical support

- Multiple perils overlap: Fire and water, wind and moisture, impact and movement, or failure and resulting damage

A lot of policyholders wait too long because they don’t want to seem aggressive. But asking for evidence isn’t aggression. It’s how complex claims are properly handled.

How to Hire a Forensic Engineer for Your Property Claim

Most property owners don’t need a list of random engineers. They need the right engineer for the dispute they have.

A fire-damaged building may require a different background than a foundation movement claim or a failed mechanical system. That’s why many owners engage a forensic engineer through an experienced claims professional who understands the loss, the policy issues, and the type of expert needed.

Start with fit, not just availability

If you’re hiring for a property claim, ask whether the engineer regularly handles insurance-related causation questions. A strong design engineer isn’t automatically the right forensic witness.

The best candidates usually match the actual dispute.

For example:

- Structural damage issues: Look for civil or structural expertise

- Mechanical equipment failures: Seek a mechanical background

- Electrical fire or system failure questions: Look for electrical specialization

- Water intrusion and envelope disputes: Ask about roofing, cladding, flashing, and building enclosure analysis

If you’re unsure when to bring a broader claim professional into the process, this article on when to hire a public adjuster can help you time the decision better.

What to verify before you hire

This part is straightforward. Don’t skip it.

Credentials checklist

- Active P.E. license: Confirm the engineer is properly licensed for the relevant jurisdiction

- Relevant discipline: Civil, structural, mechanical, electrical, or another field tied to the actual damage

- Claim-related experience: Not just design work, but investigation and report writing tied to failures

- Testimony comfort: If the claim escalates, the engineer should be able to defend the opinion

- Clear communication: Technical skill matters, but the ability to explain findings matters too

Questions worth asking in the first conversation

A short interview can reveal a lot. You don’t need to sound like an expert. You just need to listen for clarity.

Try questions like these:

- Have you handled claims involving this kind of damage before

- What evidence would you want preserved before repairs begin

- Will your report explain causation in plain language

- Do you expect destructive testing or laboratory analysis may be needed

- What assumptions would make your conclusion weaker or stronger

- Have you worked in disputes where the insurer blamed wear, age, or faulty construction

- What deliverables will I receive at the end of the engagement

The best answers are specific. If the engineer only speaks in broad generalities, keep looking.

A good forensic engineer should be able to explain the likely investigation path before the site visit starts.

What the final work product should include

Policyholders often assume they’re paying for a walkthrough. They’re paying for an opinion built on method.

A useful report often includes:

| Report element | Why it matters |

|---|---|

| Site observations | Creates the factual record of physical conditions |

| Photos and marked exhibits | Helps non-engineers follow the findings |

| Document review summary | Shows what information was considered |

| Analysis and reasoning | Connects evidence to conclusion |

| Causation opinion | Addresses the central dispute in the claim |

| Repair or structural implications | Supports scope discussions and next steps |

Depending on the case, the engineer may also recommend more invasive evaluation, temporary stabilization, or specialist follow-up.

How costs and process usually feel from the owner’s side

Property owners often get nervous at this point. They worry they’ll spend money on an expert and still be ignored.

That concern is understandable. But the better way to think about the forensic engineer job in a claim is this: you’re paying for clarity where ambiguity benefits the insurer.

The process usually works best when:

- Evidence is preserved early

- The engineer is briefed on the exact dispute

- The public adjuster or owner provides organized records

- Repairs don’t erase key conditions before inspection

- The report is integrated into a broader claim strategy

Red flags to avoid

Not every engineer is a fit for every loss. Be cautious if you hear any of the following:

- “I can tell just by looking.” Complex causation usually needs more than a glance.

- “I don’t really write formal reports.” In claims, the report is often the whole point.

- “Licensure doesn’t matter much here.” It does.

- “I mainly do general contracting now.” That may be useful experience, but it’s not the same role.

- “I’ve never dealt with insurer pushback.” Then they may not understand how carefully the opinion must be framed.

Keep the goal in view

You are not hiring a forensic engineer to make the claim more complicated. You are hiring one to reduce uncertainty in the one area that tends to decide difficult losses: causation.

For homeowners, that can protect against a lowball scope. For commercial and nonprofit owners, it can protect operational continuity, budgets, and long-term repair quality.

The right engineer won’t promise a result. That would be a bad sign. They will promise a disciplined investigation and a defensible opinion. In a serious claim, that’s what you need.

Secure Your Claim with Expert Engineering Insight

The forensic engineer job sits in two worlds at once. It’s a demanding profession for highly trained engineers, and it’s also one of the most useful services a policyholder can bring into a difficult property claim.

For Oregon and Washington owners, that matters more than many people realize. These claims often turn on hidden conditions, disputed causation, and repair scopes that look smaller on paper than they do in real life. A forensic engineer helps replace uncertainty with evidence.

That’s especially powerful when the engineer’s findings are paired with strong claim advocacy. The engineer explains what happened to the property. The claim representative uses that explanation to push back when the carrier minimizes the loss.

If you feel stuck because the insurer’s version of events doesn’t match what happened at your property, don’t assume their first position is final. It may be the first position taken before the full evidence is developed. Knowing the common insurance adjuster tricks can also help you recognize when a claim is being framed too narrowly.

You do not have to accept a causation dispute as an unsolvable stalemate. In many cases, it’s a technical problem that needs a technical answer.

When the damage is serious and the explanation is contested, expert engineering insight can level the playing field.

If your Oregon or Washington property claim involves disputed structural damage, hidden failure, fire, water, or storm loss, NW Claims Management can help you understand your options and coordinate the right claim strategy. Their team represents policyholders, not insurers, and can help determine when independent expert support, including forensic engineering, may strengthen your path to a fair settlement.