The call comes fast. Your building just took a hit from fire, water, wind, or a burst pipe. Staff are asking whether payroll is safe. Tenants want answers. Customers are waiting. Then the insurance carrier starts calling, emailing, scheduling inspections, and asking for documents you haven't even had time to find.

That's where a lot of business owners make the same mistake. They assume the adjuster sent by the insurance company is there to help them recover. That adjuster may be professional and courteous, but their job is tied to the carrier's side of the claim, not your financial recovery.

If you're trying to keep a business alive while proving structural damage, inventory loss, equipment damage, and lost income, you need your own expert. In serious losses, that often means a commercial public adjuster. Think of them as the person who takes control of the claim, documents what the insurer will miss, and pushes the file forward while you deal with the actual disaster.

If fire is part of your loss, practical rebuilding guidance also matters. This overview of H-Towne fire claim assistance is useful because it shows the restoration side of the equation, not just the paperwork. And if you need a direct look at what a commercial claim involves from the policyholder side, review this breakdown of a commercial insurance claim process.

After Disaster Strikes Your Business

The first day after a commercial loss is chaos disguised as administration.

You're standing in a wet lobby, a smoke-damaged warehouse, or an office with tarps over the roof. Someone from the carrier asks for a statement. Another person asks for a repair estimate. A third wants proof of ownership for damaged contents. Meanwhile, your business isn't operating normally, and every hour of delay costs money.

That pressure leads owners to understate the claim without realizing it. They hand over a rough list instead of a full inventory. They focus on obvious building damage and ignore code upgrades, specialized equipment, extra expense, and the revenue hit from downtime. Then months later they find out the insurer has valued the claim around what was easy to see, not what it takes to recover.

A commercial loss has two tracks running at once. One is physical restoration. The other is claim strategy.

Most owners are prepared for the first one. Very few are prepared for the second.

When the insurer starts moving quickly, you need to slow down just enough to document the loss correctly. Fast reporting helps. Rushed valuation hurts.

A commercial public adjuster enters at that exact pressure point. They don't repair the property. They build, present, and negotiate the claim for the policyholder. That matters because the conflict of interest is real. Your carrier has experts. You should too.

Your Advocate in the Claims Process

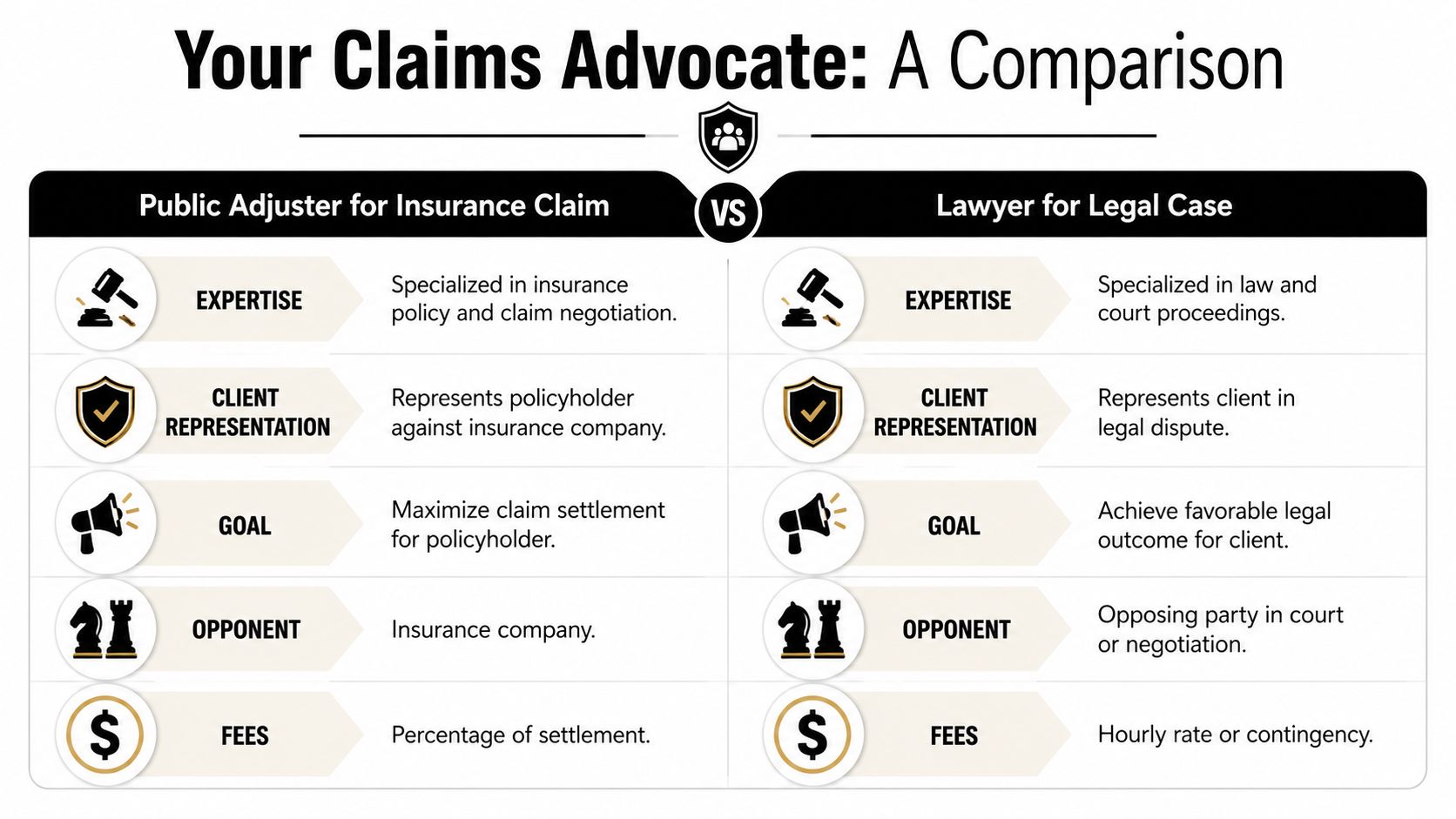

A commercial public adjuster is the only type of adjuster hired to represent you, the policyholder, rather than the insurance company. In most U.S. states, policyholders have the legal right to hire a Public Adjuster, and these professionals are the only consumer advocate legally authorized to represent the policyholder against the carrier. To become one, candidates must post a bond, pass a strict background check, and often complete an apprenticeship of up to one year, as explained in this overview of what a public adjuster is and how the profession is regulated.

That's the legal definition. Here's the practical one.

When your business claim gets complicated, a public adjuster is like a CPA walking into a tax audit with your books already organized. They know the policy language, they know what documentation matters, and they know how to push back when the other side narrows the claim.

Who works for whom

This is the confusion that trips people up. “Adjuster” sounds neutral. It isn't.

| Adjuster Type | Who They Represent | Primary Goal |

|---|---|---|

| Company Adjuster | Insurance carrier | Evaluate and settle the claim for the insurer |

| Independent Adjuster | Insurance carrier that hired them on contract | Handle the claim on the insurer's behalf |

| Public Adjuster | Policyholder | Document, present, and negotiate for the insured's recovery |

The company adjuster may be an employee. The independent adjuster may be an outside contractor. That difference matters to the insurer. It usually doesn't matter to you. In both cases, they're on the carrier's side of the file.

The public adjuster is different. They represent the insured. That's the whole point.

For a clearer side-by-side explanation, this page on a public adjuster vs insurance adjuster lays out the distinction in plain language.

What a commercial public adjuster actually does

On a real commercial loss, their work is not just “talking to insurance.” It usually includes:

- Policy analysis to identify what coverages may apply and where the pressure points will be.

- Damage documentation for building components, contents, stock, equipment, and specialty property.

- Claim preparation so the submission is organized, supported, and harder to dismiss.

- Communication management with the carrier, so you're not answering technical questions on the fly.

- Negotiation over scope, pricing, valuation, timelines, and business interruption issues.

Practical rule: If the loss is large enough that you'd need an accountant, contractor, equipment specialist, or lawyer to explain parts of it, it's large enough to consider a commercial public adjuster.

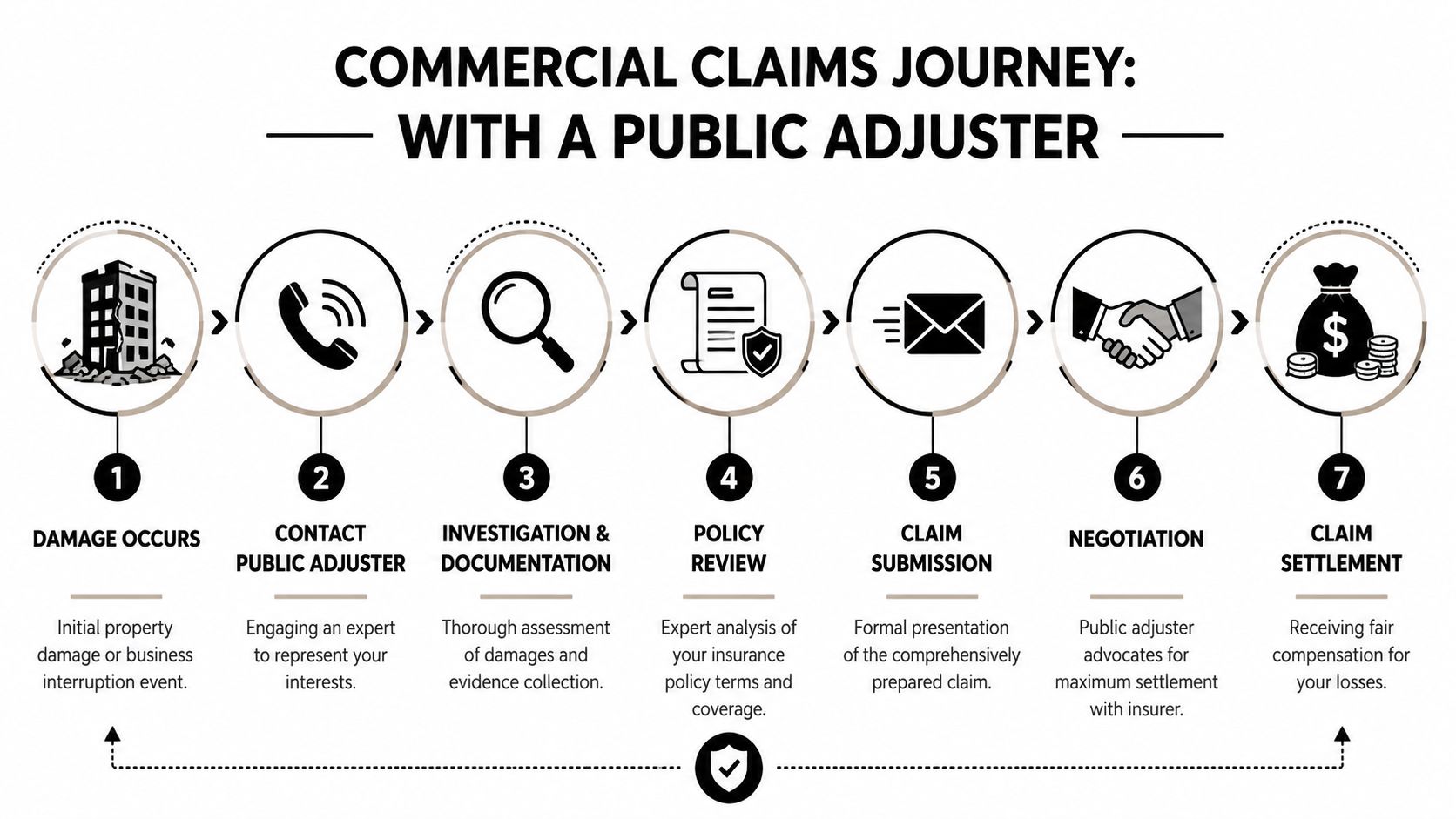

The Commercial Claims Process With an Adjuster

A strong commercial claim doesn't happen because someone “files paperwork.” It happens because someone builds the claim from the ground up.

That work is technical. A commercial public adjuster's workflow can include strategizing recovery goals, charting action courses, recreating building structures through 3D modeling, documenting detailed loss inventories, valuing machinery and equipment, and assessing business revenue interruption losses, as described in this explanation of the commercial public adjuster technical process.

It starts with policy review and site control

First, the adjuster reads the policy, not just the declarations page. Coverage questions hide in endorsements, exclusions, sublimits, and timing requirements. If nobody checks those early, the claim can drift in the wrong direction before it's even fully documented.

At the same time, they inspect the site with claim strategy in mind. Not just “what's damaged,” but “what must be proven.”

That means identifying building damage, affected operations, damaged stock, equipment, inaccessible areas, code issues, and emergency mitigation costs.

The file is built before it is argued

A carrier won't pay because you're frustrated. It pays based on documentation and policy application.

That's why a proper claim build-out usually includes:

A detailed damage inventory

Room by room, area by area, system by system. If contents are involved, the list must be specific enough to support value.Building reconstruction scope

Technical estimating is essential. Materials, finishes, demolition, code-related items, and hidden damage need support.Equipment and specialty property valuation

Machinery, tools, commercial kitchen systems, production lines, tenant improvements, and electronic systems all need their own analysis.Timeline evidence

When damage occurred, when mitigation started, what access was lost, and how long normal operations were interrupted.

The businesses with the strongest claims usually aren't the ones with the loudest complaints. They're the ones with the best records.

Business interruption changes everything

For many businesses, the hardest part of the claim isn't the building. It's the downtime.

A retail store may reopen partially but still lose sales. A manufacturer may have usable space but no working equipment. A restaurant may get repairs done yet remain limited by smoke contamination, permit delays, or supply issues tied to the loss. A public adjuster should help frame those losses as claim issues, not just business headaches.

Submission, negotiation, and closing the gap

Once the claim is assembled, the adjuster submits it in a form the insurer can evaluate. Then the actual work starts. Questions come back. Scope disagreements surface. Pricing gets challenged. Parts of the loss may be accepted quickly while others stall.

The adjuster keeps pressure on the file, responds with support, and negotiates toward final settlement. That doesn't make the process instant. Commercial claims can take time because the documentation burden is real. But a managed process is far better than a reactive one.

The Financial Benefits of Expert Representation

Business owners usually ask the blunt question first.

Is hiring a commercial public adjuster worth the fee?

My opinion is yes, when the claim is large, technical, or tied to operational shutdown. Not because every adjuster is perfect, and not because every claim needs one, but because serious commercial losses are easy to under-document and hard to fix later.

Better claim valuation

Insurers respond to organized scope, supported pricing, and policy-based arguments. They don't respond to “this feels too low.”

A commercial public adjuster can spot loss elements owners often miss, including hidden structural issues, damaged contents that weren't part of the first walkthrough, and claim components that require technical estimating rather than rough contractor numbers. On commercial files, that difference matters because once the carrier locks onto an incomplete scope, every later supplement becomes a fight.

A lot of that work depends on tools and expertise the average business owner doesn't use every day, including detailed estimating platforms, inventory development, and equipment valuation methods.

Time back for the owner

You don't need another job right now. But that's exactly what a commercial claim becomes if you manage it alone.

Every document request, inspection, pricing dispute, and follow-up call lands on your desk. While that's happening, you're also trying to relocate operations, retain customers, reassure staff, and make decisions about repairs. Handing the claim build and negotiation work to a professional gives you back the time to run the business.

If you're dealing with lost income as part of the file, this resource on a business interruption claim is worth reviewing because it focuses on the part of the claim owners struggle with most.

The business interruption piece is where many claims break down

This is the area I'd tell every owner not to underestimate.

A critical and often overlooked benefit of expert representation is the ability to quantify and negotiate business interruption losses, which can exceed the physical damage portion of the claim. Many BI claims are underpaid because the documentation fails to prove details like the period of restoration or actual loss sustained, as discussed in this guide on questions to ask before hiring a public adjuster for BI-related issues.

That means the issue isn't just whether your business lost money. The issue is whether the loss is documented in a way the policy recognizes.

If your revenue dropped after the loss, don't assume the carrier will calculate that fairly for you. Make them respond to a documented BI claim, not a rough estimate.

Rules and Fees in Oregon and Washington

If you're in Oregon or Washington, don't hire anyone until you confirm they're properly licensed for your state.

Public adjusting is a regulated profession. Nearly all U.S. states require licenses issued by the insurance commissioner, with only Arkansas, Alaska, South Dakota, and Alabama listed as exempt from licensing mandates in this discussion of the public adjusting licensing framework. Oregon and Washington are licensing states, which means a legitimate firm serving business owners there should be operating under those state rules.

That matters for one reason above all others. A regulated professional has legal obligations, licensing requirements, and contract standards they must follow. A random consultant or contractor promising to “handle the insurance side” does not fill the same role.

How the fee model works

Most commercial public adjusters work on contingency. Plain English: they don't get paid until you get paid.

Verified industry guidance says commercial public adjuster fees are typically contingency-based and average 10% to 15% of the final settlement, while many states regulate fees through caps or contract rules. Florida is one clear example. It caps public adjuster fees at 20% for standard losses and reduces that maximum to 10% for claims filed within the first year after a declared emergency, according to this explanation of public adjuster fee structures and state caps.

That Florida example matters even if your property is in Oregon or Washington. It shows the model is not a free-for-all. States regulate it.

What Oregon and Washington business owners should ask for

Don't overcomplicate this part. Ask for direct answers.

- License confirmation so you know the firm is authorized to act as a public adjuster in your state.

- A written contract that clearly explains the fee structure, services, and who does the work.

- An explanation of timing so you know when the fee applies and whether it applies to all claim proceeds or only certain portions.

- Clarity on partial payments because many owners hire help after the insurer has already paid something.

If you want a straightforward place to start, review what a licensed public adjuster does and compare that against any firm you're interviewing.

A good fee agreement should feel boring. Clear percentage, clear scope, clear signatures. If it feels slippery, walk away.

How to Select the Right Public Adjuster

Don't hire the first person who shows up with a clipboard.

After a large loss, business owners are vulnerable to confidence theater. Some people sound experienced because they talk fast, use claim jargon, and promise a big result. That's not the same thing as competent representation.

What to look for first

Start with fit, not personality.

A commercial claim is different from a residential one. If the adjuster mainly handles homes, they may not be ready for leased space issues, tenant improvements, stock valuation, equipment loss, or business interruption documentation.

Use this short screening list:

- Commercial experience with buildings and operations similar to yours.

- Oregon or Washington presence so they understand local practice, licensing, and claim logistics.

- Document-heavy discipline because commercial claims are won on proof, not charm.

- Clear communication so you know who will answer calls and who will prepare the actual claim.

- No guaranteed outcome language because no honest adjuster can promise a settlement amount before the work is done.

If you're deciding when outside representation makes sense, this page on when to hire a public adjuster can help frame the timing decision.

Questions every business owner should ask

Ask these in the first meeting and write down the answers.

What commercial claims like mine have you handled before?

You want similarity, not general confidence.Who will be my day-to-day contact?

Sometimes the person selling the job isn't the person managing it.How do you document business interruption losses?

If they get vague here, that's a problem.How do you handle partial payments already made by the insurer?

This can affect how fees are calculated.Are your fees negotiable on large commercial claims?

Ask directly. Don't dance around it.What outside experts do you work with when a claim needs them?

Commercial files often require coordination with accountants, contractors, engineers, or inventory specialists.

A critical question is whether fees are negotiable, especially on larger commercial claims, and how they're calculated if the insurer has already made a partial payment. Verified guidance also notes that fees can range from 5% to 40%, and that professional representation often increases total settlements by 20% to 50%, according to this article on questions to ask about public adjuster fees and value.

Red flags that should end the conversation

“We can guarantee what the insurance company will pay.”

That alone is enough to move on.

Also walk away if you see any of these:

- High-pressure signing tactics right after the loss.

- Vague contracts with unclear percentages or services.

- No commercial claim examples despite broad promises.

- Poor answers on BI claims because that's often where the money is.

- A focus on speed over accuracy when the file clearly needs detailed documentation.

Take Control of Your Claim Recovery

A major commercial loss can make even experienced owners feel cornered. The building is damaged, the business is disrupted, and the carrier controls information, process, and tempo unless you push back with your own structure.

That's why the right move is usually not “wait and see.” It's getting the claim reviewed early, documenting it correctly, and deciding whether the file is too technical to manage alone.

A commercial public adjuster brings order to a process that punishes incomplete records and rewards precision. They read the policy, build the evidence, deal with the insurer, and put numbers behind losses that owners often know are real but can't easily prove in claim-ready form. For Oregon and Washington businesses, licensing and contract clarity should be paramount. So should serious discussion of business interruption.

One practical option in the Pacific Northwest is NW Claims Management, a firm serving Oregon and Washington under public adjuster licenses and handling commercial, residential, and nonprofit property claims. If you want to understand the type of support a licensed firm provides before making contact, their main site gives a straightforward starting point.

Don't wait for the insurer's version of the loss to become the default version. Once the file is shaped around an incomplete scope, correcting it gets harder, slower, and more expensive.

If your business property in Oregon or Washington has suffered serious damage, the next smart step is simple. Get the claim evaluated by someone who works for you.

If you need a second set of eyes on a commercial loss, contact NW Claims Management for a free, no-obligation claim evaluation. It's a practical way to find out where your claim stands, what may be missing, and whether professional representation makes financial sense before you commit to anything.