A Wenatchee wildfire rarely begins as a paperwork problem. It starts with something more ordinary. Dry heat. A sharp smell in the air. A text from a neighbor asking if you can see the smoke column from your side of town.

Then the questions come fast. Should you leave now or wait? What should you pack? Did your policy cover smoke damage, debris removal, temporary housing, business interruption, tree loss, erosion work, or only the obvious burn damage? Most property owners don’t struggle because they failed to care. They struggle because wildfire recovery turns into a technical insurance fight at the exact moment they’re exhausted.

That’s where this guide matters. If you’re dealing with wildfire wenatchee wa concerns, you need more than brush-clearing reminders. You need a practical plan for preparing the property, leaving safely when orders are issued, documenting the loss correctly, and putting yourself in a strong position before the insurer starts narrowing the claim.

The Reality of Wildfire Risk in the Wenatchee Valley

A lot of Wenatchee residents know the feeling. You look toward the hills on a summer afternoon and try to decide whether that haze is distance, heat shimmer, or something serious. By the time you refresh local alerts, your mind has already jumped ahead to your roof, your garage, your trees, your pets, your photos, your records, and whether you could get out quickly if the road closes.

That reaction isn’t overblown. It’s grounded in local history.

What local history tells you

The 1994 Tyee Creek fire in the Wenatchee National Forest burned for 33 days, destroyed 35 homes and cabins, and required over 2,775 firefighters to respond, according to HistoryLink’s account of the Tyee Creek fire. That single event is enough to show the scale a regional fire can reach.

The same historical record notes that related fires in the region also consumed additional acreage and drew in even more personnel, including military support. For property owners, that means one thing. A major wildfire doesn’t stay neatly contained in the way people hope it will.

Practical rule: Treat smoke in the Wenatchee Valley as a financial warning sign, not just a visual one.

Wildfire damage is broader than most owners expect

When people think about wildfire loss, they usually picture a total burn. Insurance claims rarely stay that simple.

A property can survive standing and still suffer serious loss from:

- Wind-driven embers that ignite vulnerable edges of the structure

- Smoke infiltration into insulation, HVAC systems, attic spaces, and contents

- Heat exposure that warps frames, damages seals, and shortens roof life

- Ash and soot contamination across surfaces, electronics, and inventory

- Post-fire runoff and erosion that create a second wave of property damage

That last category gets missed constantly. Owners focus on the fire front, then discover slope instability, drainage failure, or contaminated soil after the flames are gone.

The real problem after a wildfire

Sound decisions are often made when there is ample time. Wildfire strips time away.

You may be dealing with evacuation, family logistics, temporary lodging, contractor calls, and an insurer requesting immediate statements before you’ve even seen the full damage. If you don’t organize the claim early, the insurance file starts taking shape without your version of the loss.

That’s why the process matters as much as the damage itself. The strongest wildfire claims in Wenatchee usually come from owners who prepare before fire season, document methodically after reentry, and resist the urge to settle based on the first number put in front of them.

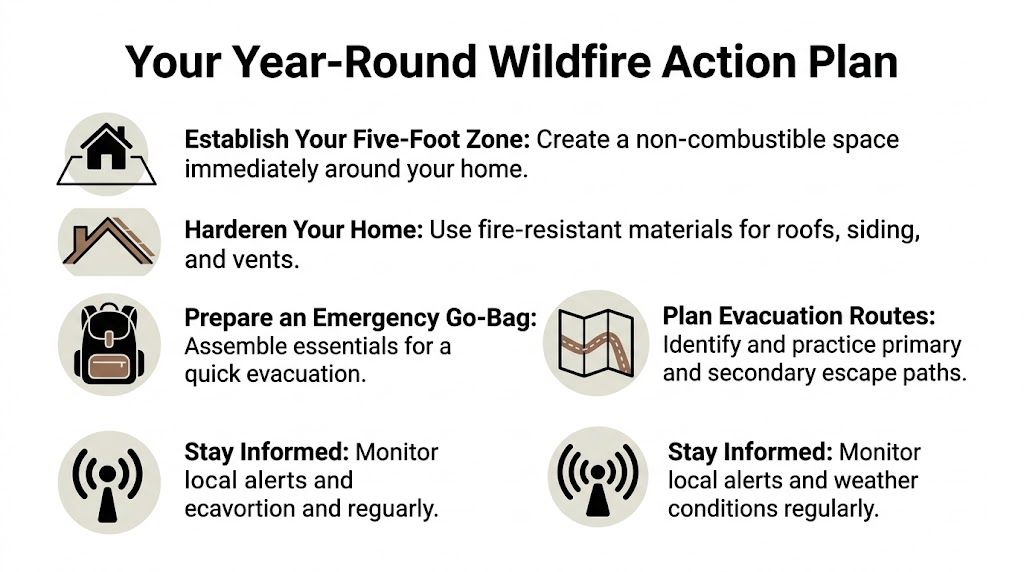

Your Year-Round Wildfire Action Plan

Preparation works best when it’s boring, repeatable, and documented. If your wildfire plan depends on doing everything perfectly during a red-flag day, it’s not a plan. It’s hope.

Start with the structure, not the yard decorations

The area immediately around the house matters most. Many owners put energy into the far edge of the property while leaving the most vulnerable zone cluttered.

Focus first on a five-foot non-combustible zone around the structure. In practice, that means reducing ignition opportunities right next to walls, decks, doors, vents, and foundations.

A solid baseline checklist looks like this:

- Remove ignition-friendly items: Move bark mulch, wood stacks, dry patio cushions, spare lumber, cardboard, and gas cans away from the house.

- Choose hard surfaces where possible: Gravel, stone, pavers, and well-maintained concrete are more predictable near the home than combustible outdoor materials.

- Watch corners and dead spaces: Fences, deck stairs, and the side yard where leaves collect often become ember traps.

Harden the house against ember entry

In Wenatchee-area wildfire losses, the property doesn’t always need direct flame contact to suffer major damage. Embers exploit weak points.

Pay attention to the places owners tend to ignore:

| Vulnerable area | What to check | What works better |

|---|---|---|

| Roof | Missing shingles, debris in valleys, needle buildup | Clean rooflines and maintain fire-resistant roofing materials |

| Vents | Large openings or damaged screens | Ember-resistant vent protection |

| Windows | Aging seals or cracked trim | Tight seals and maintained exterior trim |

| Decks | Dry debris between boards and underneath | Regular cleaning and enclosed or managed under-deck areas |

| Gutters | Leaf and needle accumulation | Frequent cleaning during fire season |

If you own a rental, shop, or mixed-use building, apply the same discipline to service yards, loading areas, dumpster enclosures, and roof access points. Commercial losses often start where maintenance standards slipped.

Prepare the people inside the property

Your house can be physically ready and your household still be unprepared.

Every property should have:

- A go-bag for each person: Include clothing, chargers, medications, glasses, pet supplies, and basic hygiene items.

- A document pouch: IDs, insurance declarations, policy contact numbers, medical information, banking access details, and property records.

- A communication plan: Decide who updates extended family, where everyone meets, and who handles pets or livestock if you’re separated.

The owners who recover fastest after a fire usually aren’t the calmest people. They’re the people who prepared while calm.

Build an insurance-ready home inventory

This is the step people skip because it feels tedious. It becomes the step they wish they had done once they’re standing in ash or smoke damage trying to remember what was in every room.

Walk the property with your phone and record video slowly. Open closets. Film drawers. Narrate brand names, materials, and approximate purchase timing when you know it. Save receipts if you have them, but don’t stop there. Video evidence is often far better than memory.

Include:

- Furniture and rugs

- Electronics and appliances

- Tools, sporting gear, and hobby equipment

- Jewelry and collectibles

- Business equipment if you work from home

- Seasonal storage in garage, attic, and outbuildings

Back up the files to cloud storage and an external drive stored away from the home.

A second smart move is learning how your policy caps different categories of payment before a loss happens. This guide on insurance policy limits explained is useful because many owners don’t realize the policy can have separate limits, conditions, and valuation rules for structure, contents, and living expenses.

Don’t ignore smoke preparation

Even if the house never catches, smoke can force expensive cleaning, filter replacement, and indoor air management. Good filtration matters before and after a fire event, especially if ash and odor enter the home. If you’re reviewing indoor air options, this overview on finding the best HEPA filters for your home is a practical companion to wildfire prep.

What doesn’t work

A few habits consistently fail property owners:

- Last-minute photo dumps: Blurry pictures taken during panic don’t replace a real inventory.

- Overgrown “natural” landscaping near the house: Attractive doesn’t mean defensible.

- Assuming insurance records are enough: Your insurer doesn’t maintain a room-by-room list of your belongings.

- Saving everything only on one device: Phones get lost, damaged, or left behind.

If you’re serious about wildfire wenatchee wa preparation, the goal isn’t only to reduce burn risk. It’s to create a claim file before you ever need one.

Responding When Evacuation Orders Are Issued

When an evacuation order comes in, people lose time arguing with themselves. They want one more hour. One more load. One more sweep through the garage.

That’s how departures turn frantic.

What Ready means

At Level 1, you should act like leaving is likely, not hypothetical.

Do these first:

- Fuel vehicles early: Don’t wait until everyone else does.

- Load key documents and medications: Put them in the car, not in a pile by the door.

- Charge devices and battery packs: Phones become your map, camera, and contact line.

- Text your core contacts: Let them know your status and intended destination.

If you have children, older relatives, pets, or livestock, assign responsibilities now. Don’t assume the family will sort it out in real time.

What Set means

At Level 2, shift from planning to execution. You should be able to leave in minutes.

Before leaving, if it’s safe and local guidance allows, take practical property steps:

- Close windows and doors

- Move outdoor combustibles away from the structure

- Shut off propane if appropriate for your setup

- Leave exterior access clear for firefighters

- Do not lock gates if local responders advise it

This isn’t the moment for roof climbing, hose deployment experiments, or trying to save every item in the house. Focus on life safety and clean departure.

If an order rises while you’re still deciding what matters, take documents, medications, phones, chargers, pets, and leave. Property can be documented later. People can’t.

What Go means

At Level 3, leave immediately.

Don’t circle back for “one last thing.” Don’t stay because the smoke shifted for ten minutes. Fire behavior changes fast, and traffic gets worse with every delay.

A safe exit usually follows a few simple rules:

- Use your primary route if it’s open.

- Switch early to your backup route if conditions change.

- Keep headlights on and windows up in smoke.

- Drive with intention, not speed. Panic driving causes its own emergencies.

- Expect roadblocks, checkpoints, and rerouting.

What to bring if you have sixty seconds left

When people freeze, a short list helps. Prioritize this order:

| Priority | Take first |

|---|---|

| Life and health | People, pets, medications, mobility aids |

| Identity and access | Wallet, IDs, keys, phone, chargers |

| Financial recovery | Insurance papers, photos inventory, policy contacts |

| Essential continuity | Laptop, hard drive, checkbook, basic clothing |

What to expect after you leave

Evacuation centers, hotels, family homes, or temporary rentals all create paperwork. Save everything tied to displacement. Lodging receipts, meal records if your policy may address them, pet boarding invoices, replacement clothing for emergency need, and mileage logs can all matter later depending on the policy language.

Keep a simple timeline in your phone notes:

- Order issued

- Departure time

- Where you stayed

- Who you spoke with

- What you paid for

- Any official notice allowing reentry

That timeline becomes more useful than expected. It anchors your memory when the insurer starts asking for dates and sequences weeks later.

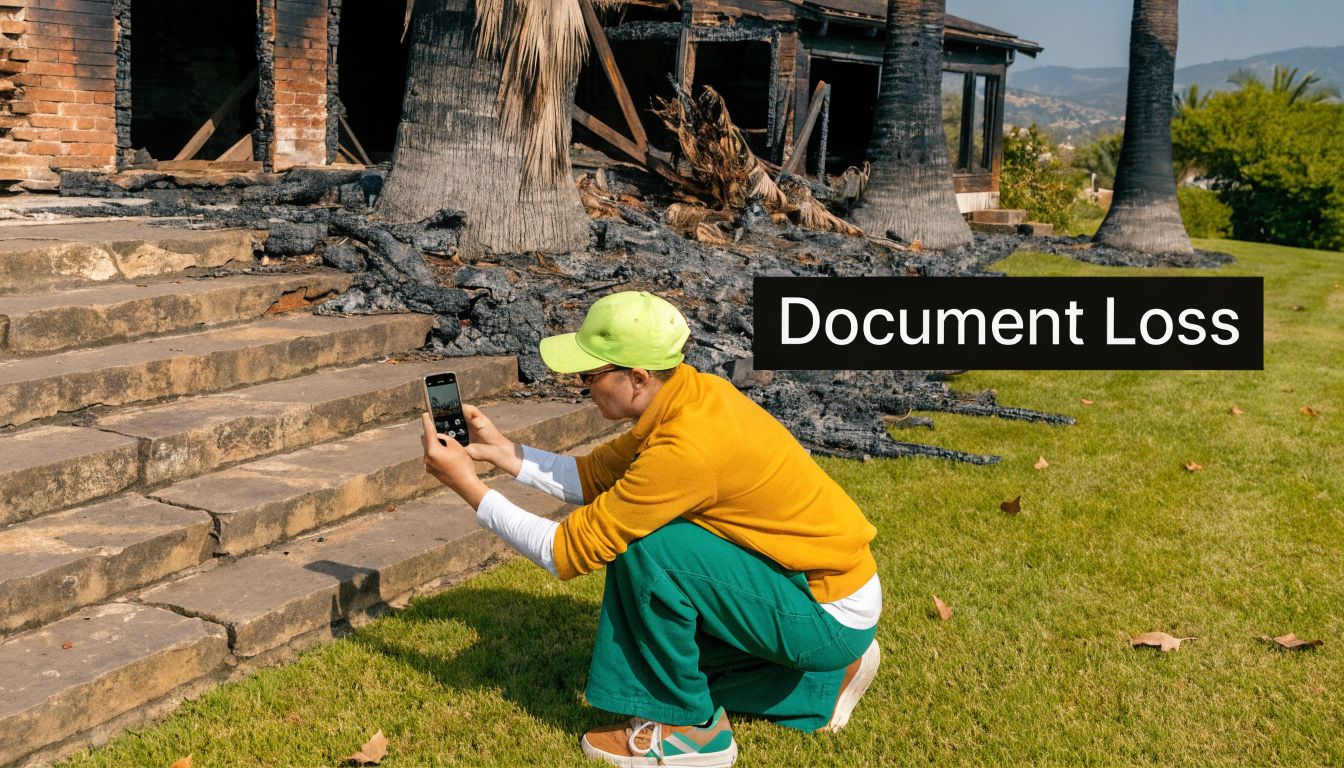

After the Fire Passes Documenting Your Property Loss

The first return to the property is where many wildfire claims either strengthen or weaken. People are overwhelmed, tired, and desperate to start cleaning. That instinct is understandable. It’s also risky.

The first job isn’t cleanup. It’s evidence.

Follow one rule first

Document everything before you move or discard anything.

That includes burned items, partially damaged items, smoke-coated contents, warped fixtures, insulation debris, damaged fencing, spoiled inventory, and landscaping changes. Once the item is removed, your ability to make a claim diminishes.

Start outside and work inward

Don’t begin with close-ups. Begin with context.

Take wide exterior photos from every angle:

- Front elevation

- Rear elevation

- Both sides

- Rooflines visible from grade

- Driveway and access points

- Fences, decks, retaining walls, detached structures

- Trees that fell, scorched, or threaten structures

- Slope changes, exposed soil, runoff channels, damaged drainage

Then record slow video while narrating what you see. Date your files and keep originals.

After that, move room by room.

What to capture inside

Many wildfire losses aren’t visually dramatic. You need to record the less obvious forms of damage just as carefully as heavy charring.

Use this room method:

- Stand in the doorway and take a full-room shot.

- Move clockwise and photograph each wall.

- Photograph ceiling, floor, windows, doors, and vents.

- Open cabinets and drawers.

- Capture close-ups of soot, residue, melted components, cracked finishes, and water intrusion from suppression efforts.

- Narrate odor conditions if smoke is strong.

Document things owners often miss:

- Smoke odor in soft goods

- Ash in HVAC registers

- Heat-warped vinyl or window trim

- Clouded double-pane glass

- Garage contents with residue

- Attic insulation contamination

- Food spoilage from power loss

- Business records or electronics affected by soot

Build the contents list while memory is fresh

You don’t need the perfect spreadsheet on day one, but you do need a working inventory before memory degrades.

Create categories first:

| Category | Examples to list |

|---|---|

| Furniture | Beds, sofas, tables, office chairs |

| Electronics | TVs, laptops, monitors, routers, printers |

| Kitchen | Small appliances, cookware, dish sets |

| Clothing | Daily wear, outerwear, footwear |

| Tools and equipment | Power tools, ladders, shop gear |

| Sentimental items | Albums, heirlooms, collections |

For each item, record the best information you have: description, brand, model, approximate age, condition before loss, and whether it was destroyed, smoke-damaged, or questionable pending inspection.

Land damage needs its own file

Wildfire claims often focus too tightly on the building. The land around it may need professional rehabilitation, drainage work, erosion control, or slope stabilization.

For properties that require post-fire treatment, documenting pre-treatment hydrology and soil conditions is critical. Expert-led Burned Area Rehabilitation can cost $500 to $2,000 per acre, and 60% to 75% insurer recovery often depends on strong documentation showing why the work was necessary, according to the Bureau of Indian Affairs guidance on post-wildfire recovery.

That’s where many owners lose recoverable value. They start emergency grading or erosion control without preserving enough evidence of the original condition.

Bring in trained eyes early

A homeowner can document a lot. A qualified assessor can often document the claim more credibly, especially when the damage includes smoke migration, structural heat impact, debris contamination, outbuilding loss, and land instability.

If you need a framework for a more formal inspection process, this page on property damage assessment outlines what a thorough evaluation should include.

What not to do on reentry

The most common mistakes are preventable:

- Don’t throw out contents immediately. Even badly damaged items may need to be inspected or listed.

- Don’t authorize major demolition too early. Emergency mitigation is one thing. Uncontrolled tear-out is another.

- Don’t rely on memory alone. Write and film everything.

- Don’t clean surfaces before photographing them. Soot patterns and residue levels matter.

- Don’t assume “minor smoke” equals minor claim. Smoke can affect habitability, contents, and systems well beyond what the eye catches.

A wildfire file gets built from the bottom up. Photos, videos, notes, inspection findings, receipts, and timelines become the structure of the claim. If that structure is weak, negotiation gets harder later.

Navigating the Complexities of a Wildfire Insurance Claim

Once the immediate shock fades, the insurance process starts pushing back. That’s when many policyholders realize the claim isn’t just about proving there was a fire. It’s about proving the full scope of what the fire did.

That distinction matters.

The insurer’s first framing of the loss isn’t final

When you report the claim, the carrier opens a file and assigns an adjuster. From that point on, the insurer begins organizing the loss into categories, timelines, and payment decisions. If your documentation is incomplete, the file can get shaped around a narrower version of the damage.

Wildfire claims often become contested over questions like:

- Was the damage caused by direct flame, smoke, heat, ember intrusion, or later contamination?

- Is the structure repairable, or are portions functionally unsalvageable?

- Which contents are cleanable versus replaceable?

- Are outdoor items, landscaping features, fencing, and detached structures covered?

- What temporary living costs fit within policy terms?

- Did the fire create secondary damage that now requires separate treatment?

Ember damage creates real disputes

In Wenatchee, historical fire patterns show why this matters. The Sleepy Hollow Fire demonstrates that wind-driven embers can cause major structural losses, and ember-related damage is exactly the kind of loss insurers may try to minimize if it isn’t documented carefully, as discussed in the CPAW recommendations for Wenatchee wildfire planning.

An ember loss can look small at first. A vent opening, deck edge, roof transition, or exterior seam may show limited visible burn, while smoke, heat, and hidden spread affect much more than the initial ignition point suggests.

Small visible burn patterns can produce large insurance disputes. Don’t let the carrier define the loss by the smallest-looking part of it.

Read the policy like a claims document, not a brochure

Owners often know the broad headings but not the practical triggers. Start by identifying the sections that control the major buckets of payment:

- Dwelling coverage for the structure itself

- Personal property coverage for contents

- Additional living expense coverage if you can’t safely live in the home

- Other structures coverage for garages, fences, shops, and detached buildings

- Debris removal and cleanup language

- Code upgrade or ordinance provisions, if present

The claim process becomes smoother when you compare every loss item against an actual coverage section instead of making assumptions.

This overview of the property damage claim process is a useful reference if you need a plain-English sequence for how claim reporting, inspection, valuation, and negotiation usually unfold.

Watch for common insurer tactics

Most wildfire policyholders aren’t prepared for how quickly pressure appears. It may be subtle, but it’s there.

Typical pressure points include:

| Tactic | What it looks like | Why it matters |

|---|---|---|

| Fast early estimate | A quick number before full inspection | Sets a low anchor |

| Narrow damage scope | Focus only on obvious burn areas | Misses smoke, heat, and hidden damage |

| Cleanup-first pressure | Push to dispose of items quickly | Reduces evidence |

| Premature finality | Language suggesting closure | Limits later recovery if accepted carelessly |

Know when outside specialists matter

Wildfire claims can overlap with contractor opinions, hygienist findings, engineer input, tree damage evaluations, and debris questions. If you’re sorting through whether removal of damaged or hazardous trees may be addressed under a policy, this practical guide on tree removal insurance coverage helps frame the issue.

That kind of supporting information matters because the carrier may separate “covered damage” from “site work” in a way that benefits the carrier unless you challenge it with evidence.

Don’t confuse payment speed with claim quality

A quick check feels like relief. Sometimes it’s only a partial payment tied to a narrow estimate. Sometimes it subtly steers the claim toward an outcome that won’t cover the full repair, replacement, and recovery burden.

The better approach is slower at the front end and stronger at the back end:

- Report promptly.

- Preserve and organize evidence.

- Read the policy.

- Track every communication.

- Challenge gaps in scope.

- Don’t sign away rights casually.

For wildfire wenatchee wa claims, informed policyholders usually do better than passive ones. Not because they argue more, but because they force the file to reflect the actual loss.

When You Need a Public Adjuster on Your Side

At some point, a wildfire claim stops being a documentation problem and becomes a representation problem. That’s the point where many owners realize they need someone who deals with policy language, valuation disputes, and insurer pushback every day.

Know who works for whom

Three adjuster roles get confused all the time:

- Company adjuster works for the insurance carrier.

- Independent adjuster may be contracted by the carrier, but still serves the carrier’s side of the claim.

- Public adjuster works for the policyholder.

Only one of those roles is hired to advance your interpretation of the loss.

The red flags are usually obvious in hindsight

You should think seriously about public adjuster involvement when the claim has one or more of these features:

- High overall value

- Complex smoke, ash, or ember issues

- Commercial or mixed-use property damage

- Multiple structures or land rehabilitation issues

- A carrier estimate that doesn’t match the actual repair reality

- Delayed responses, repeated re-inspections, or partial denials

- You’re too overwhelmed to manage the file well

For some owners, representation is less about fighting and more about bandwidth. They can’t be project manager, evidence custodian, policy interpreter, contractor coordinator, and negotiator at the same time.

Public entities face a different kind of pressure

This isn’t just a homeowner issue. In the Wenatchee area, municipalities, schools, and nonprofits can run into policy disputes over restoration costs and administrative overload when public assets are damaged, as noted by the Wildfire Risk to Communities overview cited for this underserved claims angle.

That matters because public and nonprofit leaders often need to preserve service continuity while the claim is unfolding. They can’t let the insurance process consume the entire organization.

When getting help is the practical choice

If you’re wondering whether it’s time, this page on when to hire a public adjuster gives a clear decision framework.

One available option for Oregon and Washington property owners is NW Claims Management, a licensed public adjusting firm that handles residential, commercial, and nonprofit property claims and negotiates on behalf of policyholders rather than insurers.

The right time to ask for help is usually earlier than people think. Once evidence is lost and the claim narrative hardens, fixing the file gets harder.

Frequently Asked Questions About Wenatchee Wildfire Claims

Should I give a recorded statement right away

Not casually. If the insurer asks for a recorded statement, slow down and understand why they want it, what topics will be covered, and what your policy requires. Facts stated too early, while you’re still displaced or haven’t fully inspected the loss, can box you in later.

Should I accept the first check

Usually, not without understanding what the payment represents. A first check may be partial and appropriate, or it may reflect a narrow estimate that leaves out real damage. Read the accompanying paperwork carefully and ask whether the payment is advance, actual cash value, undisputed amount, or something the carrier considers more final.

What if smoke damage seems worse than the visible burn

Treat smoke as its own claim issue. Odor, soot spread, HVAC contamination, insulation impact, and cleaning feasibility all need documentation. Don’t let the file focus only on the most visibly charred area.

What if I think I’m underinsured

You still need to pursue every covered category fully and document the loss in detail. Underinsurance doesn’t mean you stop building the claim. It means you need a clearer strategy around scope, prioritization, and any policy conditions that may affect payment.

How do I spot insurer pressure tactics

Watch for rushed deadlines, repeated requests for the same material, narrow inspections, and language that steers you toward closure before the damage is fully understood. This breakdown of common insurance adjuster tricks can help you identify pressure points before they undermine your claim.

If wildfire damage has turned your home, business, or organization into an insurance dispute, NW Claims Management can help you evaluate the loss, organize documentation, and pursue a fair settlement with policyholder-focused representation.