The call usually comes after the shock wears off. A tree has punched through the roof in Vancouver. A kitchen fire in Portland has left smoke damage in every room. A nonprofit in Salem has water running through offices and records after a burst line. The property owner is standing in the middle of it, trying to answer three questions at once. Is the building safe, what do I do next, and why does the insurance process already feel like a second disaster?

That feeling is normal. Property claims in Oregon and Washington are paperwork-heavy, deadline-driven, and emotionally draining even before a dispute starts. You're trying to protect the building, document the damage, understand the policy, and respond to an insurer that has its own process, its own vendors, and its own timeline.

That's where claim management solutions matter from the policyholder side. Not as software jargon. As a practical way to organize the work, protect the value of the loss, and keep the claim from getting reduced because the owner is exhausted.

After Disaster Strikes Understanding Your Options

A homeowner in the Pacific Northwest usually doesn't start by asking for a “claim management solution.” They start with a soaked ceiling, a boarded window, or a business that can't reopen. They've already called the carrier. They may have spoken to a field adjuster. They may have been told to inventory contents, save receipts, mitigate damage, meet a contractor, and wait for the estimate.

That pile of tasks is the primary problem.

The damage is visible. The claim process is less visible, and that's where people lose ground. A missed photo. An incomplete scope. A contractor estimate that doesn't match policy categories. A statement given too casually. Those mistakes can narrow a claim long before anyone says the word “denial.”

The stress is real, and delay makes it worse

Many policyholders in Oregon and Washington still run into delay, confusion, and repeated requests for more information. Recent developments, including 2026 regulations in OR/WA mandating transparent adjuster disclosures, haven't solved the issue, as 55% of policyholders still report “denial fatigue” from insurer delays according to this discussion of disclosure rules and policyholder fatigue.

That term fits what owners describe every day. They're tired of repeating the story, tired of waiting for callbacks, and tired of feeling like every answer creates two more demands.

Practical rule: In the first week after a fire, storm, or water loss, your job is not just to clean up. Your job is to preserve evidence and avoid making the claim smaller than it should be.

If the damage involves roof impact or exterior storm loss, it can help to review a plain-language guide to hail damage insurance so you know what insurers often look for when evaluating visible and less obvious damage.

A structured path beats reacting one task at a time

Good claim management from the owner's side means someone is controlling the file instead of reacting to it. That includes triaging immediate damage, organizing photos, matching repair issues to policy language, tracking communications, and pushing the insurer for movement when the file stalls.

For house fires, the first moves matter more than is often realized. A practical checklist like this what to do after a house fire insurance guide can keep you from making preventable mistakes while the scene is still fresh.

The core issue is simple. Insurance companies handle claims every day. Most owners handle one of these once in a lifetime. Without a system, the side with more process usually wins.

Defining Claim Management and Why It Matters

Claim management solutions are the methods, people, and tools used to move a property claim from chaos to settlement. For a policyholder, that means more than filling out forms. It means building, supporting, and defending the value of the claim from the first notice of loss through final payment.

A better way to think about it is this. Claim management is the general contractor for your financial recovery. It coordinates evidence, timelines, valuation, communication, and negotiation so the claim doesn't drift into underpayment.

It's about two goals, not one

A lot of owners assume the point is speed. Speed matters, but it is not the only objective.

A useful claim management approach has two jobs:

- Protect the claim value: Every covered component of building damage, contents loss, code issue, and time element exposure has to be identified and supported.

- Reduce the owner's burden: Someone has to manage records, responses, scheduling, estimates, and the back-and-forth that wears people down.

When those two jobs are handled well together, the owner can focus on stabilizing life or business operations instead of chasing the file all day.

Why claims got harder

Insurance companies have changed how they process claims. The broader market reflects that shift. The global claims management solutions market was valued at US$6.8 billion in 2026 and is projected to reach US$12.4 billion by 2033, driven by digital transformation, rising claim volumes, and demand for automation, according to Persistence Market Research on claims management solutions.

That matters to property owners because modern claims aren't handled only by a person with a clipboard anymore. They're routed through platforms, scoring models, standardized workflows, and audit triggers. The insurer's process is becoming more systematic. The policyholder's side has to become more systematic too.

The old approach of “send a few photos and wait” doesn't hold up well against a carrier running a structured digital claim workflow.

What works and what doesn't

What works is a claim file built like a case file. Photos sorted by room or elevation. Mitigation invoices matched to dates. Contractor scopes reconciled against line items. Contents documented in categories that can be reviewed, not guessed at. Clear written communication after every major conversation.

What doesn't work is treating the claim like a one-time conversation. Owners get into trouble when they rely on verbal assurances, submit partial documentation, or assume the insurer's estimate captures the full scope automatically.

For example, some owners look at a carrier assignment and think that because a large administrator is involved, the process will be neutral. That isn't always how it feels from the policyholder side. If you're trying to understand how a major administrator fits into the process, this overview of Sedgwick claims management gives useful context.

The key point is simple. A claim management solution isn't one thing. It is the full system used to keep your claim organized, documented, and defensible.

Who Handles Your Claim A Comparison of Solutions

People often use the same words for very different roles. “Adjuster” can mean the insurer's employee, a contracted field adjuster, or a public adjuster hired by the policyholder. Then there are third-party administrators and software systems in the background shaping how the file moves.

If you don't know who works for whom, it's easy to assume everyone is pulling in the same direction. They aren't.

The first question is allegiance

Before discussing skill, responsiveness, or software, ask one plain question. Who does this person or system serve?

That answer shapes the whole experience.

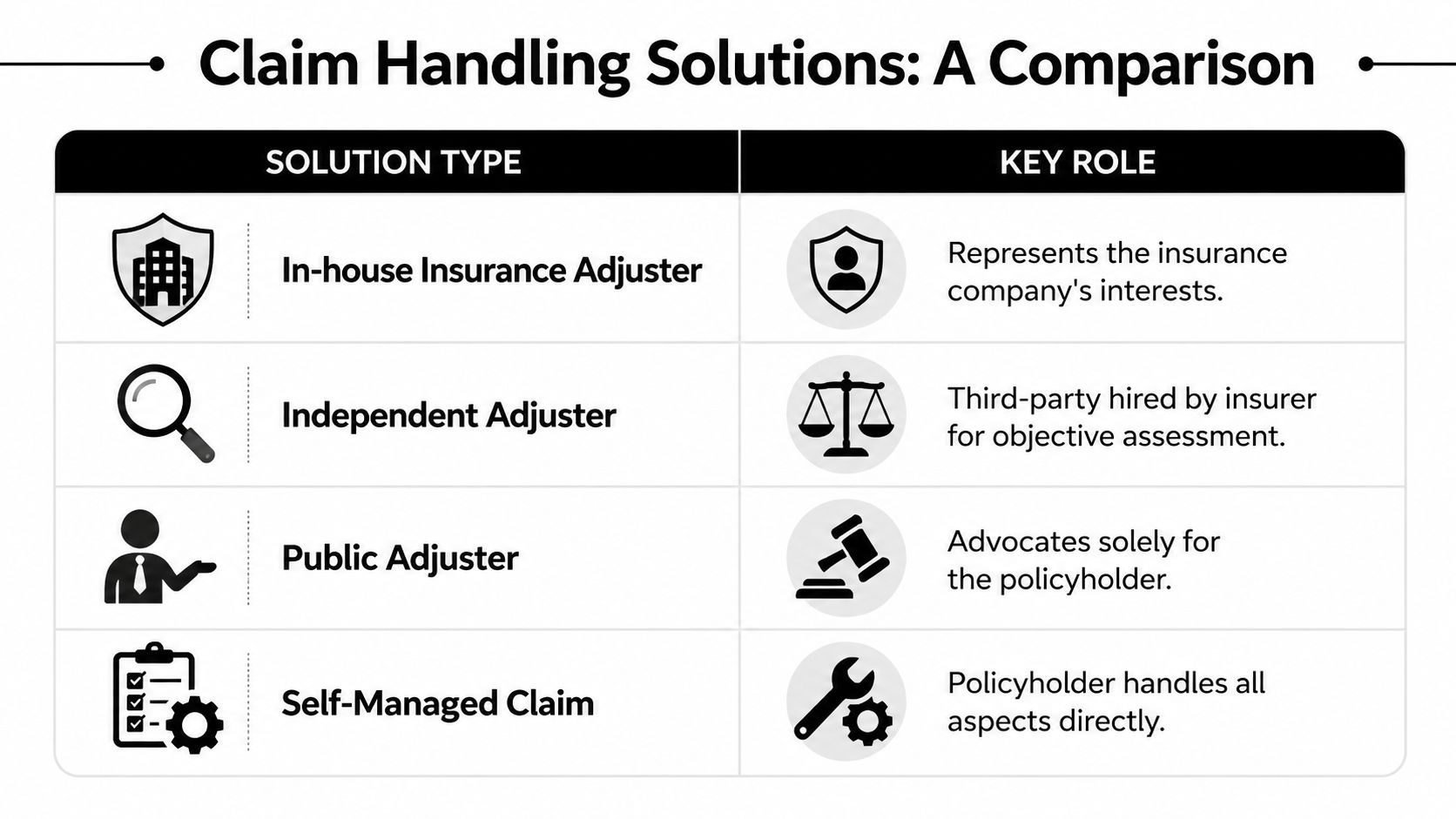

| Solution Type | Who They Work For | Primary Goal | Best For |

|---|---|---|---|

| In-house insurance adjuster | The insurance company | Evaluate and resolve the claim under the carrier's process and cost controls | Routine claims where coverage and scope are straightforward |

| Independent adjuster | Usually hired by the insurance company on a contract basis | Inspect and report findings back to the carrier | Catastrophe events or overflow claim volume |

| Public adjuster | The policyholder | Document, value, and negotiate the claim on the owner's behalf | Large, disputed, technical, or time-consuming property losses |

| Self-managed claim | The policyholder handles it directly | Submit and manage the claim without paid representation | Smaller losses or owners with time, records, and high tolerance for process |

In-house insurance adjusters

An in-house adjuster may be knowledgeable, professional, and courteous. Many are. But their role is still tied to the insurer's obligations, procedures, and internal claim objectives.

That creates a built-in limitation for the policyholder. The adjuster doesn't become your advocate just because they inspect your damage carefully.

Independent adjusters

Independent adjusters are often brought in during busy periods or catastrophe response. They may appear more neutral because they are not direct employees of the carrier. But in practice, they are still part of the insurer's claim handling chain.

Owners should treat them respectfully and professionally, while still remembering that their file is being prepared for the insurer's review, not for the policyholder's recovery strategy.

Public adjusters

A public adjuster works for the policyholder. That changes the file immediately. The focus shifts from “What can be processed?” to “What can be documented, supported, and claimed under the policy?”

That difference matters most when the loss is complex. Fire claims with smoke and contents issues. Water losses with hidden damage. Commercial claims with business interruption questions. Nonprofit losses where records, mission continuity, and building function all have to be protected at once.

If you want a deeper side-by-side look at the difference in roles, this breakdown of a public adjuster vs insurance adjuster is worth reading.

Self-managed claims

Some owners do handle claims themselves. On very small and straightforward losses, that can work. But self-management has a hidden cost. The owner becomes investigator, document manager, estimator coordinator, policy reader, and negotiator while also trying to repair the property and keep life moving.

That is a heavy lift, especially when communication turns adversarial.

A self-managed claim usually fails for the same reason a self-managed construction project fails. The work is broader than it looked at the start, and the owner discovers the complexity after costly decisions have already been made.

The software side of the imbalance

The comparison isn't just about people. It's also about systems. Insurers now use P&C claims systems with predictive analytics that improve decision accuracy by 30-50%, generating fraud and severity risk scores that help automate workflows and reduce insurer costs, according to the CLM buyer's guide on claims systems.

From the policyholder side, that means this. The carrier may be evaluating your claim through a structured digital environment while you're trying to respond with phone notes, scattered photos, and contractor emails. That mismatch is real.

What each option gets right and wrong

Here's the practical trade-off:

In-house insurance adjuster

- Gets right: Access to the carrier's internal process.

- Gets wrong for owners: No independent duty to maximize your recovery.

Independent adjuster

- Gets right: Fast deployment after major weather or surge events.

- Gets wrong for owners: Reports upward to the insurer, not sideways to you.

Public adjuster

- Gets right: Builds the claim from the policyholder's perspective.

- Gets wrong in some cases: May be unnecessary on a small, clean loss.

Self-managed

- Gets right: Full control by the owner.

- Gets wrong: Control without technical support can become expensive fast.

One practical option in Oregon and Washington is NW Claims Management, a licensed public adjusting firm that represents residential, commercial, and nonprofit policyholders rather than insurers. The important point is not the brand name. It's the structure. A public adjuster's role is distinct because the allegiance is different.

Navigating the Property Claim Lifecycle Step by Step

Most owners see a claim as one long conversation with the insurance company. In practice, it's a chain of stages. Each stage creates opportunities to strengthen the claim or weaken it.

First notice and immediate protection

The first step is reporting the loss and preventing further damage. That usually means emergency mitigation, temporary repairs, securing openings, and documenting conditions before cleanup changes the scene.

Owners often make one of two mistakes here. They either wait too long to mitigate because they fear spending money without approval, or they move too fast and throw away evidence. The right path is to protect the property while preserving proof of damage and keeping records of every emergency expense.

Investigation and documentation

At this stage, the claim begins to take shape. Site inspections occur. Photos undergo review. Statements may be collected. Repair contractors, mitigation vendors, engineers, or consultants might be involved.

The strongest files are built with discipline:

- Room-by-room evidence: Photograph damage before demolition and during demolition.

- Written timelines: Record when the loss happened, when mitigation started, and who attended inspections.

- Document control: Save every invoice, moisture report, repair recommendation, and carrier email.

If a damaged component is removed before it is documented well, recovering for it gets harder. The burden doesn't disappear just because the damage was real.

Valuation and estimate building

At this stage, numbers start appearing. Carrier estimates, contractor bids, contents lists, and code-related issues all begin to converge. This is also where many owners first realize the insurer's scope may be narrower than the actual repair path.

Valuation problems rarely look dramatic at first. They show up as omitted line items, incomplete material matching, reduced labor assumptions, or categories of damage that were never fully explored.

Why documentation speed matters

Modern claims technology uses Intelligent Document Processing to achieve up to an 80% reduction in manual data entry for unstructured documents like photos and reports, which can compress claim cycle times from days to hours, according to this overview of claims systems and IDP.

That doesn't mean software wins claims by itself. It means organized documentation now moves faster through claim workflows. When the policyholder side presents coherent, categorized evidence, the file is harder to sideline and easier to evaluate on the merits.

Negotiation and settlement

Negotiation involves more than debating a final figure. It is the process of reconciling scope, pricing, coverage interpretation, depreciation, timing, and supporting evidence. A skilled negotiator does not just state that an offer is too low. Instead, they demonstrate why specific components are incomplete or inconsistent with the loss.

Owners should expect movement to happen in rounds. Initial estimate. Supplemental review. Follow-up inspection. Revisions. Additional requests. Sometimes a long quiet period that requires firm follow-up.

A practical sequence looks like this:

- Establish the full scope before debating price alone.

- Separate coverage issues from pricing issues so discussions don't get blurred.

- Answer requests in writing and keep the file clean.

- Push supplements promptly when hidden damage or additional costs appear.

- Review settlement language carefully before assuming the claim is closed.

The final payment is not the end of your responsibility

Even after agreement, there may be depreciation holdbacks, mortgage involvement, supplemental items, or documentation needed for final release of funds. This is another place where owners drop the ball because they assume “approved” means “finished.”

It doesn't. A claim is finished when the file is paid correctly and all covered categories have been addressed.

When to Hire a Public Adjuster for Your Property Claim

Not every claim needs outside representation. Some do. The hard part is knowing the difference early enough to matter.

A public adjuster is usually worth considering when the claim is large, technical, disputed, or too demanding for the owner to manage well. Fire losses are an obvious example, but they are not the only one. Severe water damage, storm losses with roofing and interior issues, vandalism with business interruption, and claims involving repeated delays can all justify representation.

Four common trigger points

Some owners wait because they think hiring help means the situation has become extreme. Usually the smarter move is earlier, not later.

Consider representation when:

- The damage affects multiple categories of loss: Building, contents, cleanup, temporary protection, and loss of use or interrupted operations all require separate support.

- The insurer's estimate doesn't match the lived reality of the damage: If the offer won't reasonably fund the work, something in scope, pricing, or coverage needs to be challenged.

- You don't have the time to run the file: Owners with jobs, family responsibilities, tenants, or a disrupted business often can't sustain the documentation and follow-up load.

- Communication has gone sideways: Reassigned adjusters, repeated requests, unexplained delays, and vague answers are signs the claim needs tighter handling.

The right time to hire help is often the moment you realize you're spending more energy managing the claim than managing the recovery.

The financial case is hard to ignore

There is a practical reason many owners bring in a public adjuster after struggling alone. Data from a 2023 Insurance Journal study of 25,000 claims shows that policyholders who hire public adjusters recover settlements that are, on average, 747% larger than what they secure on their own. This is often because 70% of homeowners initially attempt to handle claims themselves, leading to frequent underpayments, as summarized in this review discussing public adjuster outcomes.

That doesn't mean every represented claim produces the same gap. It does mean owners consistently underestimate how much value can be lost through incomplete scoping, weak documentation, or fatigue.

A public adjuster is not just for denials

A common mistake is waiting until the claim is formally denied. By then, positions have hardened, records may be incomplete, and valuable time has been lost.

Hiring a public adjuster can make sense long before denial, especially if you want someone to:

- Take over documentation: Organize the evidence in a format that supports the claim.

- Manage inspections and estimates: Keep the scope from getting narrowed by default.

- Handle negotiation: Push back with substance, not frustration.

- Keep communication moving: Follow up consistently so delays don't become the new normal.

If you're wondering whether your situation has crossed that line, this page on when to hire a public adjuster gives practical examples.

The main point is this. Representation is not a sign of conflict. It is a way to balance a process that was never simple to begin with.

How to Select the Right Public Adjuster in Oregon and Washington

Hiring a public adjuster shouldn't feel like taking another gamble while you're already under pressure. A careful screening process helps you avoid that.

The best choice is not the person who talks the most. It's the one who can explain their process clearly, document a loss thoroughly, and work within Oregon or Washington rules without making promises they can't control.

Start with license and local fit

A public adjuster handling claims in Oregon or Washington should be properly licensed for the jurisdiction where the loss occurred. Don't skip that step. It tells you the person is operating inside the state framework and gives you a way to verify standing.

Local knowledge also matters. A firm that regularly handles Pacific Northwest fire, storm, water, and vandalism claims will usually understand the practical issues better than someone working from a generic national script. Building practices, weather patterns, inspection timing, and insurer behavior can look different here than in other regions.

If you need a starting point for Oregon-specific representation, this overview of a public adjuster in Oregon is useful context.

Ask process questions, not just price questions

Many owners jump straight to the fee. The fee matters, but process matters more because that's what drives the outcome.

Ask questions like:

- How do you document the loss? You want a specific answer involving photos, scopes, estimates, inventories, and written support.

- Who communicates with the insurer? Find out whether you'll have one point of contact or a rotating file team.

- How do you handle supplements? Hidden damage and revised scopes are common in property claims.

- What kinds of property claims do you handle most often? Fire, water, storm, and commercial losses don't all require the same workflow.

Look for clarity, not hype

A reliable public adjuster will explain what they can do and what they cannot control. They can manage the claim, support valuation, and negotiate. They cannot guarantee a specific payout.

That distinction matters. Owners under stress are vulnerable to big promises. A disciplined adjuster usually sounds calmer than a sales-heavy one.

Field advice: If the explanation is vague at the hiring stage, the claim handling will likely be vague later too.

Review the agreement carefully

Read the engagement contract. Make sure you understand the fee structure, when it applies, how communication works, and whether there are any conditions for ending the relationship.

Also ask how often you'll receive updates and in what format. Some owners want a call after every inspection. Others prefer written summaries. The right arrangement is the one that keeps you informed without forcing you back into daily claim administration.

The right public adjuster should lower your workload and improve the quality of the claim file. If the relationship sounds confusing before the ink dries, keep looking.

Frequently Asked Questions About Claim Management

Property owners usually reach the same set of questions once the initial panic subsides. They want to know whether they've waited too long, whether hiring help will make the insurer angry, and whether a smaller loss is worth the effort. Those are fair questions.

Is it too late to get help if I already opened the claim

Usually, no. Many owners hire a public adjuster after the claim has already been reported and sometimes after inspections have already happened. The earlier a claim is organized properly, the better, but late help can still be valuable if the file is incomplete, under-scoped, delayed, or headed toward a weak settlement.

What matters most is the current condition of the record. If evidence still exists, documents can be assembled, and disputed items can be supported, there is often still room to improve the outcome.

Will the insurance company treat me differently if I hire a public adjuster

The insurer may communicate more formally once you have representation, but that is not the same as retaliation. In many cases, the process becomes more structured because the carrier now has a designated point of contact who knows how to document requests, respond in writing, and keep the file moving.

That can reduce confusion. The emotional temperature often drops when the conversation shifts from frustration to documented issues.

How do public adjusters usually get paid

Public adjusters commonly work on a contingency basis. That means the fee is tied to the claim recovery rather than billed like hourly consulting.

The practical question isn't only how the fee is calculated. It's whether the agreement is transparent and easy to understand. You should know when the fee applies, what services are included, and who handles communication and documentation throughout the claim.

Are public adjusters only useful on very large losses

No. They are most obviously useful on large and technical claims, but they can also help on moderate losses that have become difficult to manage. A claim doesn't need to be catastrophic to become complicated.

A smaller loss can still justify professional help if the carrier's scope is incomplete, the policy language is unclear, or the owner can't keep up with the demands of the file.

Can I still use my own contractor if I hire a public adjuster

Yes. A public adjuster is not the repair contractor. Their role is to manage, document, value, and negotiate the insurance claim. Contractors repair the property. The two can work alongside each other, and in many cases they should.

That separation is healthy. It allows the repair scope and the insurance presentation to be coordinated without treating them as the same job.

What should I gather before I ask for help

Bring whatever you have. Useful items often include the policy, claim number, photos, videos, emergency mitigation bills, contractor estimates, inventory notes, insurer letters, and a rough timeline of what happened. If you don't have all of that, don't let the missing pieces stop you from asking questions.

A good claim review starts with the current file, not with perfection.

What does a strong claim management process feel like from the owner side

It feels calmer. You know what documents matter. You know what stage the claim is in. You know who is following up and why. The file stops living in your head and starts living in an organized process.

That is the actual value of claim management solutions from the policyholder perspective. They turn a messy, emotional dispute into a documented recovery strategy.

If your property claim in Oregon or Washington feels stalled, under-scoped, or harder than it should be, NW Claims Management offers policyholder-side public adjusting for residential, commercial, and nonprofit losses. A focused claim review can help you understand what's missing, what's recoverable, and what next step makes sense before more time is lost.