You open your mail, or your inbox, and see the notice from your insurance company. They want to inspect your property.

Most owners treat that as routine paperwork. That’s a mistake.

A loss control inspection can affect your premium, your renewal, and the way your insurer handles a future claim. If the inspector documents problems and you ignore them, those same notes can come back later when you need coverage most. I’ve seen property owners cooperate politely, then get blindsided months or years later when the carrier points to an old report and says the damage was tied to poor maintenance, an existing hazard, or an uncorrected condition.

Treat this like a financial event, not a courtesy visit.

Your Insurance Company Wants to Inspect Your Property

That notice usually lands at the worst time. You’re busy. The building is occupied. There’s deferred maintenance you’ve been meaning to handle. You assume the insurer just wants a quick look and that being cooperative is enough.

It isn’t.

A loss control inspection creates a record. That record can shape how the insurer views your property from this point forward. It may include photos, notes about maintenance, observations about fire protection, and comments about hazards that have nothing to do with the loss you might suffer later. Once those findings are in the file, they rarely disappear.

Why you shouldn’t treat it as harmless

A landmark review by MSB, now Verisk, found that 75% of insurance loss control inspections failed to produce actionable information to mitigate risks for carriers in approximately 2 million field inspection projects, according to Canalix’s summary of the MSB review. That’s the part policyholders need to pay attention to. An inspection can fail to create useful risk reduction for the carrier and still create useful ammunition against you.

That’s why I tell owners to stop thinking of inspections as neutral.

Practical rule: If an insurer wants to document your property, you should be documenting it too.

The right mindset before the inspector arrives

You don’t need to be combative. You do need to be prepared, organized, and careful with what gets said and what gets left undocumented. If you casually admit you’ve “been having some roof issues” or “haven’t gotten around to testing that system,” expect that to live in the file.

Also, don’t assume the insurer’s representative is there to protect your interests. They’re there to evaluate risk for the company. That distinction matters. If you’ve never read up on the ways insurers frame property conditions and claim narratives, this breakdown of insurance adjuster tricks is worth your time before the inspection date.

Go into the appointment with one clear goal. Present the property accurately, correct obvious issues you can fix now, and create your own paper trail before someone else creates one for you.

What Are Loss Control Inspections and Why Insurers Do Them

A loss control inspection is the insurer’s pre-claim checkup on your property. It's comparable to a lender ordering an appraisal before approving a loan. The carrier wants to know what it’s insuring, what could go wrong, and whether the premium matches the risk.

That’s the insurer’s side of it. Your side is simpler. They are gathering facts that can affect coverage decisions later.

The three reasons insurers order them

First, they use inspections for underwriting accuracy. If the property is in worse condition than the application suggested, the insurer may change the premium, add requirements, or decide the account no longer fits its guidelines.

Second, they use them for risk mitigation. The industry has a strong business reason to do that. According to the Insurance Information Institute, companies that implement thorough loss control programs experience 30% fewer insurance claims, as cited by Archipelago’s overview of insurance loss control. That explains why insurers invest time and money into inspections. They believe fewer claims justify the process.

Third, they use them for pre-loss documentation. This is the part property owners underestimate. A photo taken today can become part of the insurer’s story tomorrow.

Who actually performs the inspection

The person showing up may be:

- An insurer employee who handles field inspections for the carrier

- A third-party inspection vendor hired to collect information and photos

- A specialist consultant focused on fire protection, building systems, or commercial risk

- A remote reviewer conducting phone-based or image-based evaluation

That last category matters more than many owners realize. You may never have a full conversation with the person evaluating your risk.

The inspector may look independent, but the report is built for the insurer’s file, not yours.

What the insurer is trying to confirm

They’re usually checking whether the property matches the policy file and whether they see conditions that increase the chance of a claim. For homeowners, that often means roof condition, trip hazards, exterior upkeep, fire safety, and signs of water intrusion. For commercial properties, it can include electrical systems, housekeeping, fire suppression, access control, storage practices, and occupancy concerns.

If you own a damaged building or you're already dealing with disputed scope and pricing issues, it helps to understand how property condition gets translated into claim value. This primer on property damage assessment gives a good baseline for how insurers and policyholders often view the same facts very differently.

Loss control inspections aren’t random. They’re a business tool. Once you understand that, your job is to prepare like the result will matter, because it will.

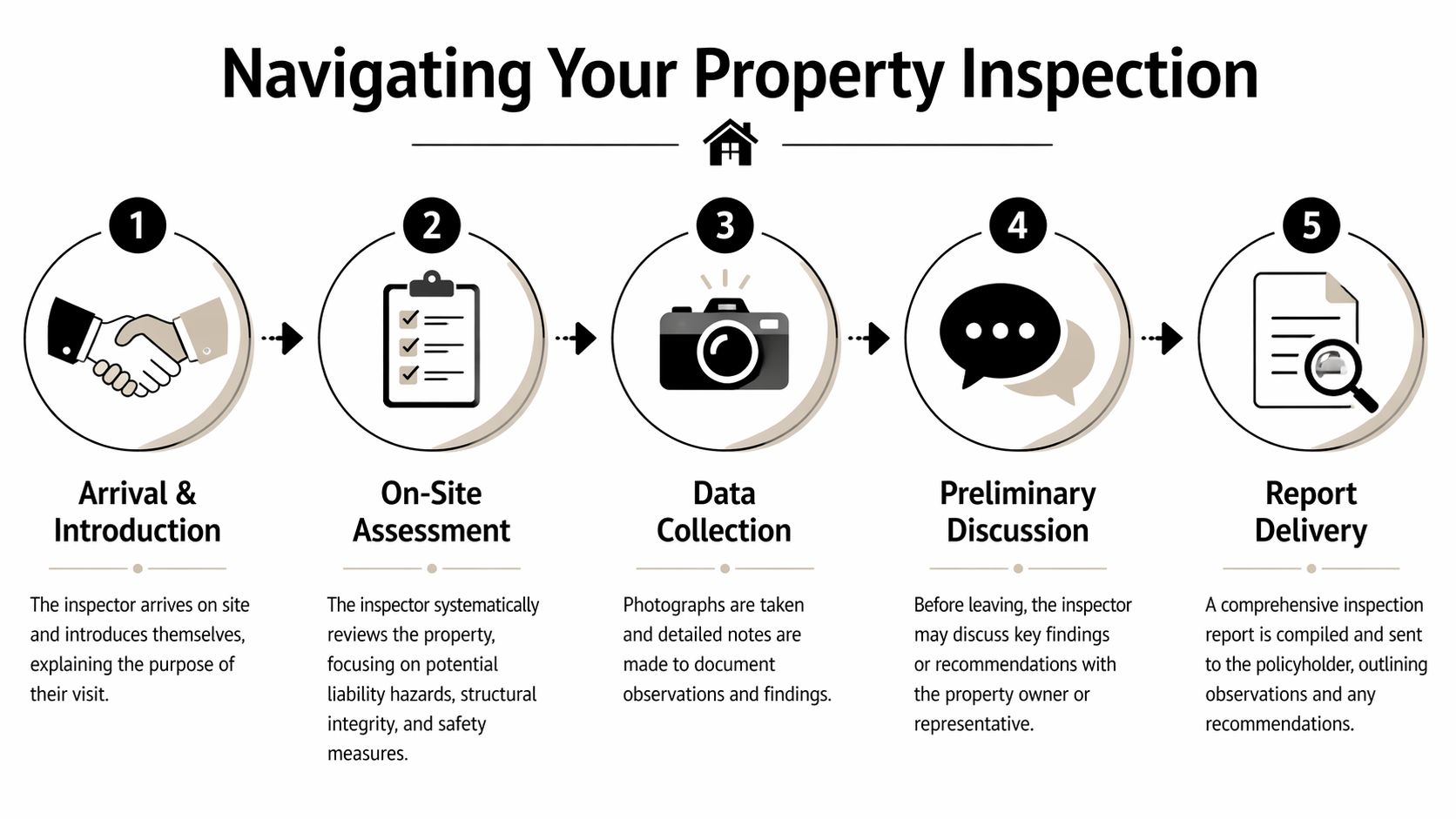

What to Expect During the Property Inspection Process

Most inspections are uneventful on the surface. The inspector arrives, asks a few questions, walks the property, takes photos, and leaves. The full impact becomes apparent later, when those observations get written into a report.

Here’s the basic flow you should expect.

What the inspector usually looks at

They’ll start with broad visibility items. Exterior condition, access paths, stairs, railings, sidewalks, roofs, vegetation, drainage patterns, and signs of neglect often get immediate attention. Inside, they may look at electrical panels, water heaters, plumbing leaks, smoke detectors, storage practices, housekeeping, fire extinguishers, and any obvious liability hazards.

If you own a commercial property, expect more focus on life-safety systems and operational risks. If you own a home, expect more attention to conditions that suggest future water, fire, or liability claims.

Some inspectors are methodical and fair. Others move quickly and photograph anything that looks questionable from a bad angle.

How the process unfolds on the day

A typical inspection looks like this:

- Arrival and identity check. Confirm who they are, who sent them, and what type of inspection they’re performing.

- Walkthrough of the property. They observe, photograph, and ask targeted questions.

- Notes on visible conditions. This includes anything they view as deferred maintenance, unsafe access, or poor housekeeping.

- Possible verbal comments before leaving. Sometimes they’ll mention concerns. Sometimes they won’t say much at all.

- Report sent after the visit. The written version matters more than the conversation.

If there’s a component you suspect may be problematic, get ahead of it. For example, if drainage is causing repeated moisture issues, a tool like modern drain camera inspection can help identify hidden line problems before an insurer’s report turns “standing water concern” into a long-term underwriting issue.

Remote and drone inspections are changing the game

Not every inspection involves someone knocking on your door. Post-2024 wildfire seasons in the Pacific Northwest have led to a 40% surge in drone-enabled inspections, according to Davies Group’s loss control services page. That matters because remote inspections often flag conditions like brush proximity without giving the owner much chance to explain context, recent cleanup, or planned remediation.

That changes the balance. The insurer gets a visual record. You may not even know what image triggered the concern.

If the inspection is remote, ask what was reviewed, what was photographed, and whether you can respond before the findings affect the policy.

The real risk for policyholders

The report can trigger repair demands, underwriting changes, or a renewal problem. A note about roof wear, vegetation, wiring, or fire protection may seem minor until the carrier asks for proof of correction. If you miss the deadline or disagree with the finding and do nothing, you’ve handed the insurer a future argument.

That’s why it helps to understand the difference between someone evaluating the insurer’s risk and someone protecting your side of the record. This comparison of a public adjuster vs insurance adjuster lays out that divide clearly.

Don’t wait for the report to take this seriously. The inspection starts the moment the property is viewed.

A Practical Checklist to Prepare Your Property

Preparation isn’t about making the place look perfect. It’s about removing easy negatives and backing up the condition of the property with records. You want the inspector to see a maintained property, not an owner who’s guessing.

Start with the obvious items you can correct quickly. Then gather your paperwork.

Physical preparation that actually matters

Walk the property like someone looking for reasons to flag it. Look at entrances, stairs, handrails, exterior lighting, roof edges you can safely observe from the ground, visible leaks, signs of rot, stored combustibles, blocked exits, and overgrown vegetation near the structure.

Inside, test smoke detectors, replace dead batteries, make sure extinguishers are visible, clear access to electrical panels, and remove tripping hazards. If the building has maintenance issues you can’t fully resolve before the inspection, at least document that you’ve scheduled service or obtained an estimate.

A clean file starts with a clean property, but it also requires clean documentation.

If you need a structured way to review routine upkeep before the inspection, a practical home maintenance checklist template can help you catch items that are easy to miss when you’re rushing.

The documents you should have ready

Don’t rely on memory. Put records in one folder, digital or paper, so you can produce them fast if needed.

| Area | Action Item | Status (To Do / Done) |

|---|---|---|

| Roof | Gather invoices, repair records, replacement paperwork, and photos | To Do / Done |

| Electrical | Collect upgrade receipts, panel work records, and electrician reports | To Do / Done |

| Plumbing | Save leak repair invoices, mitigation notes, and service records | To Do / Done |

| Fire Safety | Compile alarm testing logs, extinguisher service tags, and sprinkler records if applicable | To Do / Done |

| Exterior | Remove debris, trim vegetation, and document recent cleanup work | To Do / Done |

| Walkways and Stairs | Repair uneven surfaces, secure railings, and photograph corrections | To Do / Done |

| Water Intrusion | Keep mold remediation, drying, or waterproofing records together | To Do / Done |

| Renovations | Prepare permits, contractor invoices, and completion photos | To Do / Done |

| Occupancy and Use | Make sure the current use of the property matches what was disclosed to the insurer | To Do / Done |

| Inspection File | Create your own date-stamped photos and notes before the inspector arrives | To Do / Done |

How to create your own record

Take clear date-stamped photos before the inspection. Photograph all sides of the structure, major systems, key interiors, and any area you know could be misunderstood. If there’s an active issue, document it accurately and pair it with proof of repair efforts.

If your property has prior storm, fire, or water damage, keep that material separate and labeled. Mixing old damage, repaired damage, and current condition in one pile creates confusion later.

And if you’re already worried about how a future insurer payout could be reduced, learn the tactics that often shrink recoveries and what owners can do to maximize insurance claim payout. The best time to protect a claim file is before a loss, not after a denial letter arrives.

How Inspection Results Impact Your Premiums and Claims

An inspection report affects more than underwriting. It can shape the insurer’s attitude toward your property for years.

There are usually three broad outcomes. The insurer sees no major problem and moves on. The insurer wants corrections and gives you a deadline. Or the insurer decides the risk is outside its comfort zone and changes pricing, terms, or renewal status.

How a report affects your money now

A favorable report can help preserve current pricing and keep renewal simple. An unfavorable one can create a list of demands. Carriers may ask for proof that you repaired a railing, replaced a roof section, serviced alarms, trimmed vegetation, or corrected storage practices. If you don’t respond clearly and on time, the underwriting problem gets worse.

That’s why vague promises are dangerous. “We’re working on it” is weak. Paid invoices, contractor schedules, service records, and before-and-after photos are strong.

How an old report hurts a future claim

Policyholders can find themselves caught in a bind. Years after an inspection, you suffer a fire or water loss. The insurer opens the file and sees prior notes about maintenance, fire protection, or deferred repairs. Suddenly the claim isn’t just about the event. It’s also about whether you failed to maintain the property.

According to Visualping’s discussion of commercial insurance loss control monitoring, insurers may cite maintenance deficiencies noted in a loss control report, such as untested sprinkler systems, to deny or reduce fire claims, and those systems account for 40% to 50% of preventable fire escalations per NFPA data. That’s a powerful example of how a pre-loss report can become a post-loss defense.

The same inspection report that looked routine at renewal can become central evidence when the carrier looks for a reason to pay less.

Why you should respond to findings in writing

If the report contains mistakes, challenge them promptly. If it contains valid concerns, correct them and keep proof. If the insurer knew about a condition, kept collecting premium, and still tries to weaponize that condition later, that record may cut both ways.

Policyholders weaken their position when they leave inspection findings unanswered. They strengthen their position when they build a paper trail showing correction, disagreement with support, or insurer awareness of the issue.

Silence helps the carrier. Documentation helps you.

How a Public Adjuster Can Defend Your Interests

When an insurer uses an old inspection report against you, you need more than frustration. You need a counter-record, a policy-based argument, and someone who knows how to pull apart vague or exaggerated findings.

That’s where a public adjuster becomes valuable. Not because the inspection disappears. It won’t. But because the report can be challenged, reframed, and tested against the actual policy language, repair history, and loss facts.

What an advocate actually does

A strong public adjuster reviews the loss control report line by line, compares it to the damage claimed, and looks for weak assumptions. Was the insurer calling something long-term deterioration when the actual loss came from a sudden event? Did the report note a condition but the carrier renewed anyway? Did photos get interpreted without context?

A good challenge often involves more than argument. It may require contractor records, maintenance logs, expert evaluation, prior correspondence, and a clear timeline.

Challenging findings can change the payout

This isn’t a symbolic fight. A 2025 Lloyd’s study found that policyholders who successfully challenged negative inspection findings recovered 18% more in claim settlements, according to Mackoul Risk Solutions’ discussion of carrier inspections. That supports what experienced claim advocates already know. When you push back with evidence, the numbers can move.

Don’t accept an inspection finding as final just because it’s in the insurer’s file.

If you’re facing a reduced payment, a denial tied to maintenance, or a carrier narrative built around an old inspection, it helps to understand the full benefits of hiring a public adjuster. The right representation can keep a questionable report from becoming the final word on your claim.

The biggest mistake owners make is waiting too long. Once the insurer has shaped the story, every day of delay makes it harder to unwind.

If your insurer has inspected your property, cited maintenance issues, delayed a claim, or tried to use an old report against you, NW Claims Management can help you evaluate the damage, review the carrier’s position, and fight for a fair settlement. They represent policyholders across Oregon and Washington, not insurance companies, and they offer free claim evaluations when you need clear answers fast.