If you're searching for "JC Penney insurance," you’re probably thinking about protecting a big-ticket item you just bought, not a traditional policy for your home or car. And you'd be right. In almost every case, what we're talking about is a product protection plan, sometimes called an extended warranty.

These plans are sold at checkout and are designed to cover specific problems—like an accidental coffee spill on your new sofa or a mechanical breakdown in your washing machine—long after the standard manufacturer's warranty has expired.

What Is JC Penney Insurance Really?

First things first, let's get one common mix-up out of the way. The "insurance" JC Penney offers for furniture, appliances, or fine jewelry isn't insurance in the same sense as your homeowner's policy. It's actually a service contract, usually managed by a completely separate, third-party company.

Think of it as an optional safety net for your purchase. Its main job is to provide coverage once the manufacturer's warranty runs out. A typical manufacturer’s warranty only covers defects in materials and workmanship for a short period, usually 90 days to one year. A protection plan is meant to step in after that.

A manufacturer's warranty protects against things that go wrong with the product, like a faulty internal component. A retail protection plan, on the other hand, often covers things that happen to the product, such as accidental damage from handling.

Understanding The Key Differences

It's really important to know the difference between what the manufacturer promises and what the store's protection plan actually offers. The manufacturer's warranty is your first line of defense, but it has its limits. The protection plan is designed to fill in the gaps or take over when the original warranty ends.

To make it crystal clear, here’s a quick comparison of what a standard manufacturer's warranty covers versus a typical retailer protection plan.

Retail Protection Plan vs Manufacturer Warranty

| Coverage Aspect | Manufacturer's Warranty | Retailer Protection Plan |

|---|---|---|

| Primary Focus | Defects in materials or workmanship | Accidental damage, stains, mechanical issues |

| Duration | Short-term (e.g., 1 year) | Long-term (e.g., 3-5 years) |

| Accident Coverage | Usually not covered | Often the main feature (e.g., spills) |

| Cost | Included with the product purchase | An additional, optional cost |

Seeing them side-by-side helps illustrate the distinct roles they play.

For example, imagine your new refrigerator suddenly stops cooling six months after you buy it. If the cause is a faulty compressor, that's a classic manufacturer's warranty claim. But if your child accidentally dents the door, the manufacturer won't cover it. That’s where a JC Penney protection plan could save the day, assuming it includes coverage for accidental damage. Understanding this distinction is the key to knowing exactly what you're paying for at the register.

The Forgotten History of JC Penney's Insurance Empire

When you hear “JC Penney insurance” today, your mind probably jumps straight to those protection plans they offer for furniture or appliances. But there's a much bigger, almost forgotten story here. For a long time, JC Penney wasn't just selling sofas; it was a genuine powerhouse in the traditional insurance industry.

This all started back in the 1960s. It was an era when many big retailers were looking for new ways to grow, and JC Penney saw a golden opportunity in financial services. They didn't just dip their toes in the water; they dove in headfirst, creating an insurance subsidiary that would completely reshape the company.

From Retail Giant to Insurance Titan

And it worked. By tapping into its massive customer list and the trust people already had in the JC Penney name, the company built an insurance empire almost entirely through direct marketing. This wasn't just some small side hustle—it became a huge source of steady income, often cushioning the company from the volatile world of retail.

The legacy of JC Penney's insurance division is a powerful reminder that a brand's expertise can sometimes stretch into surprising new areas. It also underscores a key lesson: whether you're a massive corporation or just a homeowner, managing financial risk always requires specialized knowledge.

This diversification was incredibly successful. The insurance division grew into a behemoth, and by 1997, it was managing over 13 million policies and accounts. But as the new millennium approached, the retail world was changing fast, and JC Penney decided it was time to get back to its roots. In a landmark deal, the company sold its direct-marketing insurance business to the Dutch insurer Aegon in 2001 for $1.3 billion. You can read more about this strategic decision and its financial reasoning.

This history is exactly why the name “JC Penney insurance” still has a ring of familiarity for so many people. Even though the company no longer underwrites life or health insurance, its past success forged a lasting link between the brand and financial protection. It’s a fascinating chapter that shows how a retail icon once became an insurance giant, leaving a legacy that still shapes how we see the brand today.

Decoding the Fine Print of Your Protection Plan

When you check out with a new piece of furniture or a pricey appliance, that offer for a protection plan can sound pretty tempting. But let’s be clear: what you're buying isn't an all-encompassing insurance policy. It’s a very specific service contract, and the devil is always in the details.

Think of your plan's terms and conditions as its rulebook. It lays out exactly what a "covered event" is and what it isn't. If something happens that’s not on that list, you’re out of luck. Taking the time to read that fine print now can save you a world of frustration later.

What's Typically Covered

Most JC Penney protection plans are designed to handle life’s little mishaps and the mechanical failures that happen right after the manufacturer's warranty gives out. They're there to keep your purchase looking and working like new.

Here’s a look at what you can usually expect to be covered:

- Accidental Stains: For furniture, this is a big one. Think spills from coffee, wine, or even messes from kids and pets.

- Accidental Damage: This generally includes things like rips, tears, burns, or punctures on fabric and leather surfaces.

- Structural and Mechanical Breakdowns: A recliner mechanism that stops working or a cracked sofa frame often falls under this. For appliances, it’s about motors, compressors, and other essential parts that fail after the initial warranty expires.

- Jewelry Damage: Plans for jewelry are more specialized, often covering things like bent prongs on a ring, a cracked band, or a broken necklace clasp.

What's Almost Always Excluded

Now for the most important part: the exclusions. This is the section that trips most people up because it's where the company draws a hard line on what it absolutely will not pay for.

The exclusions section is arguably the most critical part of your protection plan. It tells you the exact boundaries of your coverage, preventing costly assumptions about what you're entitled to.

You can bet you'll find these situations on the "not covered" list:

- Normal Wear and Tear: This is a classic. The slow fade from sunlight on your sofa, minor scuffs from daily life, or cushions that naturally soften over time are considered your responsibility.

- Damage from Pets: While a one-time accident might get a pass, damage from a cat who uses your new chair as a scratching post or a dog who habitually chews on the legs is a standard exclusion.

- Improper Use or Abuse: Using a home appliance for a commercial business? Standing on a dining chair to change a lightbulb? If the item wasn't used as intended, any resulting damage won't be covered.

- Catastrophic Events: These plans are not meant to cover massive damage from a fire, flood, or other major disaster. That's what your homeowners or renters insurance is for. In fact, understanding your primary insurance policy limits explained is essential for navigating these large-scale events.

By reading both what's included and—more importantly—what's excluded, you put yourself in the driver's seat. You’ll know exactly what you’re paying for with your JC Penney plan and can decide if it’s truly the right fit for you before you ever have to make a call for help.

How to File a Claim and Navigate the Process

It happens. That brand-new sofa gets a red wine stain, or the refrigerator you just bought suddenly goes quiet. It’s easy to feel a jolt of panic, but this is exactly why you bought a protection plan. Filing a claim doesn't have to be a headache; if you know the steps, it's actually quite manageable.

The most important thing? Act fast. Don’t let a week go by. Many plans have strict timelines for reporting an incident. The moment you spot the damage or the malfunction, your first job is to document everything. Get your phone out and take clear photos or a short video from different angles. This visual proof is your strongest asset when dealing with the claims administrator.

Locating Your Documents and Making the Call

Next, you'll need to gather your paperwork. Find the original sales receipt and the protection plan contract itself. These documents are gold because they hold your contract number and, critically, the contact information for the plan administrator. It's important to realize you probably won't be calling JC Penney directly, but rather a third-party company that manages the JC Penney insurance program.

Before you pick up the phone or go to their website, have this information ready to go:

- Your name and current contact details

- The original purchase receipt showing the date you bought the item

- Your protection plan or contract number

- A straightforward description of what’s wrong—is it damaged or not working?

- Your photos and videos

Once your claim is submitted, the administrator starts their review. They’ll look at your evidence and compare it against the fine print in your plan. They might follow up with questions or, in some cases, send a technician to your home for a firsthand look. For a broader overview of this initial stage, our guide on how to file a property damage claim provides some excellent foundational context.

Understanding the Outcome

After the review, a few things can happen. The administrator might approve a repair, authorize a complete replacement, or offer a store credit or cash payment based on the item’s current value. But what if your claim is delayed or denied? This is often due to missing information or because the specific issue is listed as an exclusion in your contract.

If you get a denial, don’s just accept it. Your next step should be to politely ask for a written explanation that points to the exact clause in your contract they're using to deny the claim. A denial can sometimes be the result of a simple misunderstanding.

The claims world is always evolving, and it can be interesting to see how technology like automated claims processing is changing how things are handled behind the scenes. By staying organized, being persistent, and knowing your rights, you put yourself in the best position to get the resolution you paid for.

Retail Plans vs. Homeowners Insurance

It’s easy to get confused about the difference between a retail protection plan and your homeowners insurance. Let’s clear that up. Think of a JC Penney protection plan as a specialist—it’s there for one specific job. Your homeowners insurance, on the other hand, is the full-scale emergency response team for a major disaster.

The JC Penney insurance you bought for your new washer is designed to handle a very specific problem, like a sudden mechanical failure. Your homeowners policy, however, protects all your personal belongings (including that washer) from catastrophic events like a fire, a widespread pipe burst, or a break-in.

Which Policy Is Primary?

Knowing who to call first is everything. If your new appliance just stops working on its own, you’ll turn to the retail plan. But what happens if a kitchen fire damages that same appliance along with half your house?

In that scenario, your homeowners insurance is always the primary policy. It's built to handle large-scale, complex losses. You would file one comprehensive claim with your home insurance carrier, which would cover the value of the damaged appliance and everything else. Trying to file a separate, smaller claim with the retail plan administrator would just muddy the waters and complicate your recovery.

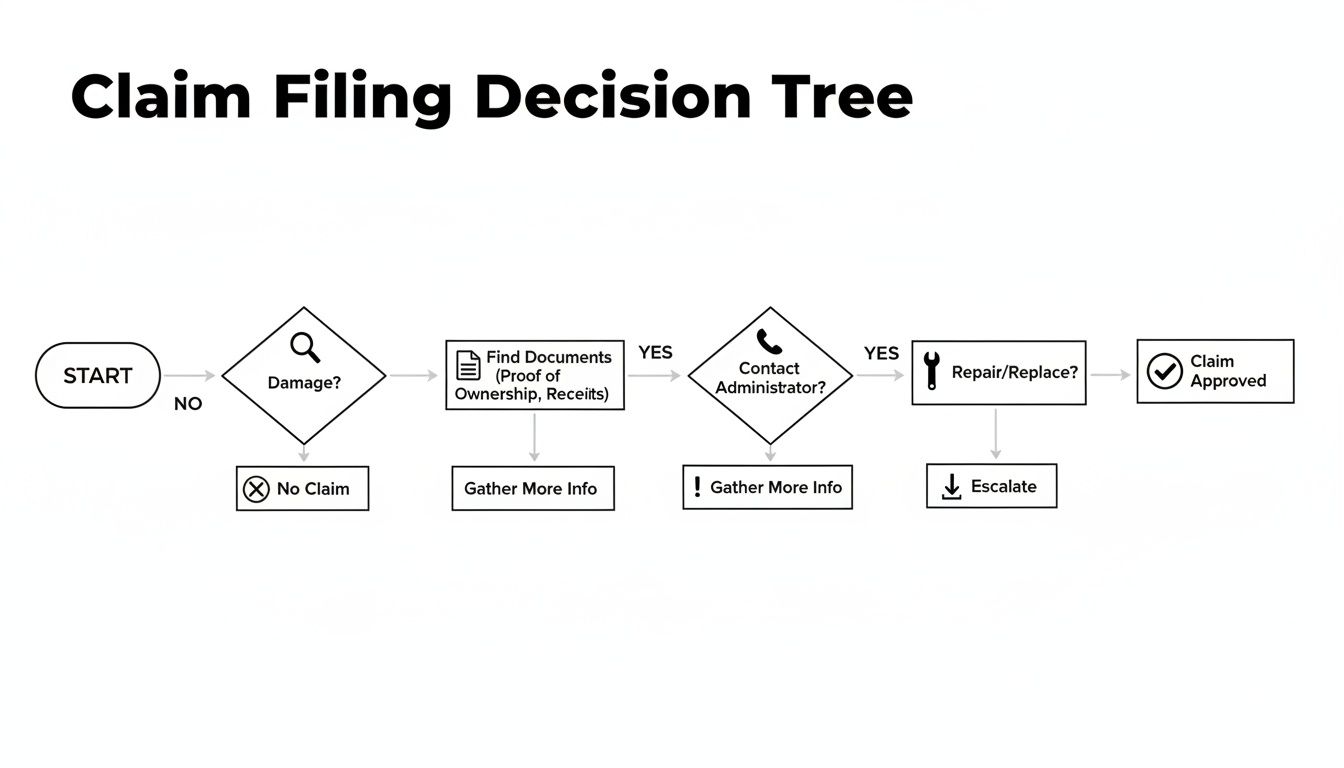

This flowchart maps out the typical claim process for a retail protection plan. It’s a straightforward path from identifying the damage to getting a resolution for that single item.

As you can see, the path to a repair or replacement under a retail plan is very linear. It’s a world away from the complexities of a major property disaster claim.

The Buffer Against Financial Storms

This idea of using different financial tools for different risks is a time-tested strategy. In fact, JC Penney’s own insurance division proved this back in 1991. While the company's retail income was tanking in a turbulent economy, its insurance pre-tax income jumped by an impressive 44%. It shows how a specialized insurance operation can act as a financial buffer, a lesson every homeowner should take to heart.

In a major property loss, your homeowners policy is your financial lifeline. It is the comprehensive tool designed to restore your home and possessions, while a retail plan is reserved for isolated, everyday mishaps.

To really get a handle on what a robust policy looks like, it helps to review a Florida homeowners insurance comparison and see what comprehensive coverage entails. When disaster does strike, your first move should always be a professional property damage assessment. This is the first step to making your primary insurance policy work for you and ensuring every single loss is accounted for.

When You Need a Public Adjuster for Your Property Claim

Filing a claim on a JC Penney protection plan for a single faulty appliance is one thing. You can usually handle that yourself. But facing a catastrophic loss from a fire, a hurricane, or a major flood? That's a whole different ballgame.

Suddenly, you’re not just trying to replace one item. You’re facing a mountain of paperwork and a complicated negotiation with your homeowners insurance company. And let's be clear: their adjuster works for them, not for you. Their job is to protect their company's financial interests, which often means paying out as little as possible.

This is precisely when you need a professional in your corner. A public adjuster is a licensed claims expert who works only for you, the policyholder. They are your advocate, and their one and only goal is to make sure you get the full, fair settlement you're entitled to under your policy.

The Role of Your Advocate

Think about it this way: a public adjuster is like your personal project manager for the entire insurance claim. They dive deep into the fine print of your policy, meticulously document every single loss—from the structural damage to your roof down to the last fork in your kitchen drawer—and handle all the back-and-forth with the insurance company.

Their expertise becomes your shield against the common tactics insurers use to delay, deny, or drastically underpay claims.

A public adjuster is essential in these situations:

- Large or Catastrophic Claims: After a house fire or widespread water damage, the sheer amount of work needed to document everything correctly is staggering.

- Complex Policy Language: Insurance policies are notoriously confusing. A public adjuster knows how to interpret obscure clauses and endorsements to find coverage you might have missed.

- Lowball Settlement Offers: If the first offer from your insurer feels insultingly low, a public adjuster will build a detailed, evidence-backed case to demand what you’re actually owed.

- Unfair Claim Denials: When a claim is denied, it can feel like a dead end. A public adjuster will analyze the denial and fight to get that decision overturned.

The entire point of insurance is to be a financial safety net when disaster strikes. A public adjuster's job is to make sure that safety net actually holds up when you need it most.

Using insurance as a tool for financial survival isn't a new concept. In fact, James Cash Penney himself famously borrowed against his life insurance policies to pull his company through the Great Depression. You can read about how visionary business leaders have used insurance as a lifeline.

Today, public adjusters apply that same fundamental principle, fighting to make sure homeowners and businesses get every dollar they deserve from their policies to rebuild. For a more detailed breakdown of the process, it's worth learning more about when to hire a public adjuster to protect your financial recovery.

Common Questions About Retail Protection Plans

When you’re buying a new couch or appliance, you’ll almost always get asked if you want the protection plan. It’s that moment at the checkout counter where you have to make a quick decision. Is it worth it? What does it really cover? Let's walk through the questions I hear most often so you can feel confident in your choice.

A big one is pet damage. People want to know if the plan will cover their cat deciding the new armchair is a perfect scratching post, or their dog getting a little too friendly with a table leg. I can tell you from experience, the answer is almost universally no. These retail plans are notorious for having specific exclusions for pet damage, so it's best to assume your furry family members' antics are on you.

What to Do in a Major Disaster

Another scenario that causes a lot of confusion is what happens after a major event, like a house fire or significant water damage. You have homeowners insurance, but your new fridge also has a protection plan. Which do you call first?

The answer is simple: your homeowners insurance is always your primary claim. It's the policy built for disasters and is designed to cover your personal property as a whole. Trying to file a separate, tiny claim for a single appliance with the store’s plan administrator while you’re dealing with a major loss just adds unnecessary chaos. Focus on the big picture with your home insurer first. Getting that part right is crucial, which is why understanding the ins and outs of negotiating with your insurance company is so important.

The principle of having proactive financial tools and expert guidance is key to resilience. NW Claims Management embodies this by providing exclusive client advocacy, leveraging 20+ years of expertise to dissect policies, document damages, and negotiate optimal settlements. You can discover more about the value of expert advocacy from trusted sources.

Are Protection Plans Worth It?

This is the million-dollar question, isn't it? Are these plans just a money grab? The honest answer is, it really depends. It comes down to the price of the item and your own tolerance for risk.

For something expensive that gets a lot of daily use—think of the main family sofa or your primary refrigerator—a plan that covers accidental spills and mechanical failures can bring genuine peace of mind. On the other hand, for a cheaper item that you could afford to repair or replace yourself without much financial pain, the extra cost of a plan probably isn't a smart buy. Always take a minute to read the fine print before you say yes.

If you're facing a major property loss and need an expert to manage your claim and secure a fair settlement, NW Claims Management is here to help. Get your free claim evaluation at https://nwclaimsmanagement.com.