The first hours after a house fire, burst pipe, or wind loss are always the same. You’re standing in the driveway, your phone won’t stop buzzing, a contractor is handing you a card, the insurance carrier says an adjuster will call, and everyone seems to want a decision before you’ve even had a full night’s sleep.

That’s when people in Oregon and Washington make one of the most expensive mistakes in this business. They assume every adjuster is there to help them in the same way.

They aren’t.

A private claims adjuster, also called a public adjuster, works for you. Other adjusters work for the insurance company. If you understand that early, you protect yourself. If you miss it, you can spend months fighting uphill on scope, pricing, code issues, contents, and timeline while thinking you already had an advocate.

After the Disaster Before the Rebuild

If your home was just damaged, you probably aren’t thinking in insurance language. You’re thinking about where you’ll sleep, whether the smoke smell will ever come out, and how long your family can live in limbo.

That’s normal. The claim starts before claimants feel ready for it.

A serious property claim moves fast. The carrier wants notice of loss, mitigation vendors want approval, contractors want scope decisions, and the adjuster assigned by the insurer starts building a file right away. If you don’t know how that file gets built, you can fall behind before the actual negotiation even begins. A useful starting point is understanding the home insurance claim process, because the sequence matters almost as much as the damage itself.

Why this feels so uneven

Most homeowners handle very few major claims in a lifetime. The industry handles them every day. The claims adjusting field includes over 125,000 professionals, with insurance companies employing about 70% in-house, and those professionals collectively adjust an estimated $450 to $500 billion in claims value each year according to the American Association of Insurance Claims Professionals survey.

That number matters for one reason. Your loss may feel personal, but it enters a system built around process, documentation, and negotiation.

Practical rule: The first version of your claim file often shapes every conversation that follows.

What a private claims adjuster actually does at this stage

A private claims adjuster steps into the middle of that chaos and organizes it. Not later. Right then.

That means identifying what was damaged, documenting what can disappear with cleanup, reading the policy for coverage triggers, coordinating estimates, and making sure the insurer is evaluating the full loss instead of the most visible portion of it. After a fire, for example, the challenge often isn’t just the burned framing. It’s smoke migration, damaged finishes, electronics contamination, debris handling, code upgrades, temporary repairs, and personal property detail that nobody has fully listed yet.

This is why people hire representation. Not because they want a fight, but because they need someone who knows where claims get undercounted.

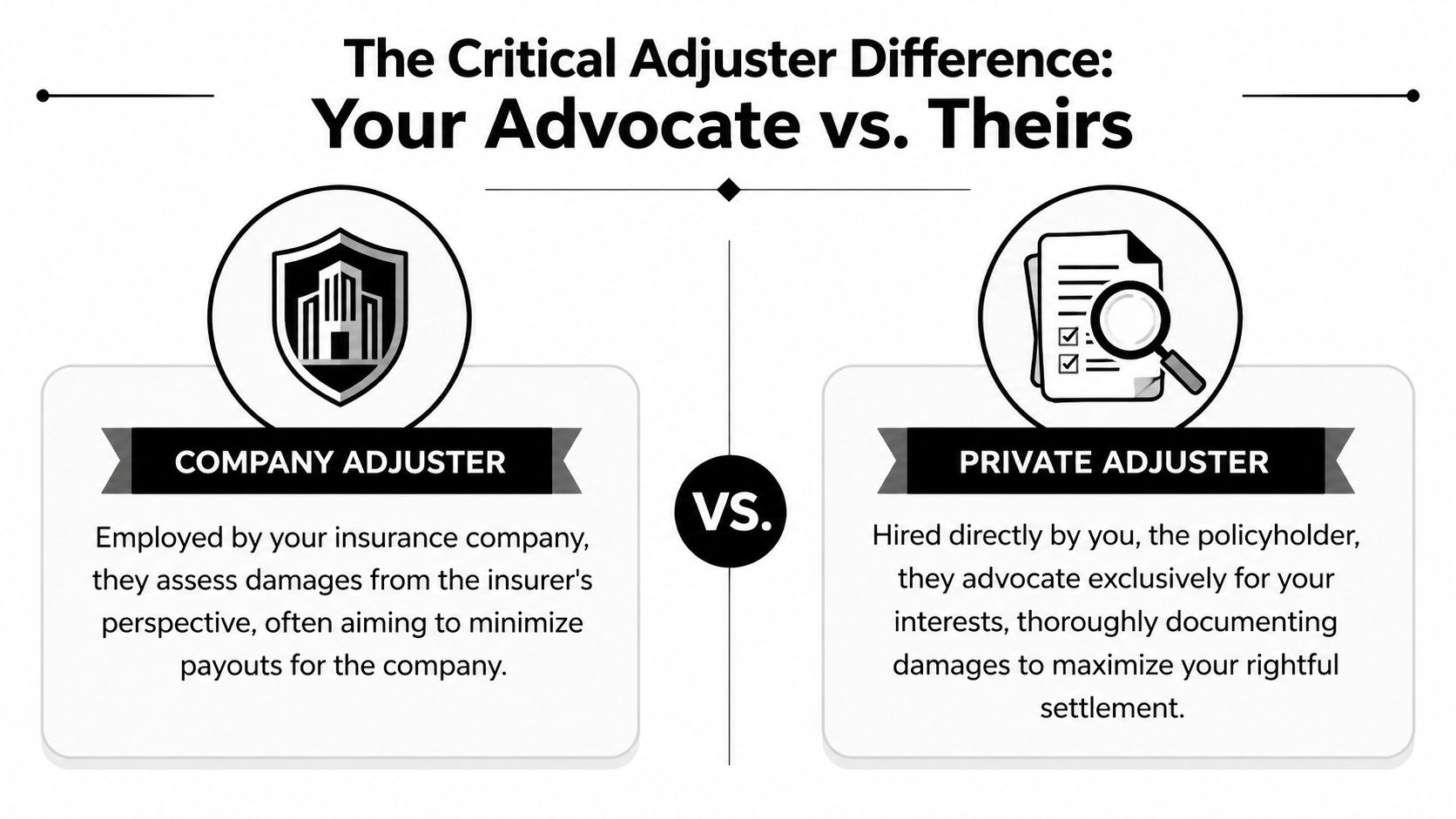

Your Advocate vs Theirs The Critical Adjuster Difference

This is the part I wish every policyholder understood before the first inspection.

There are usually three kinds of adjusters involved in property claims. Only one works for you.

The three roles in plain English

| Adjuster type | Who hires them | Who they represent | What that means for you |

|---|---|---|---|

| Company adjuster | Insurance carrier | Insurance carrier | They investigate and evaluate the loss for the insurer |

| Independent adjuster | Insurance carrier or third-party firm | Insurance carrier | They are not independent from the claim outcome from your side |

| Private or public adjuster | Policyholder | Policyholder | They document and negotiate for your recovery |

The word independent confuses people constantly. In everyday language, it sounds neutral. In claims, it usually means the person is an outside contractor hired by the insurance company.

A major source of confusion for policyholders in Oregon and Washington is the difference between independent and public/private adjusters. Independent adjusters work for insurers and handle a significant portion of the $450 to $500 billion in annual claims, while public adjusters are licensed by the state to represent the policyholder exclusively, as explained in this overview of public adjusters versus insurance adjusters and supported by Claim Concepts.

Why the mix-up costs people money

I’ve seen homeowners say, “The independent adjuster is coming out, so at least I’m getting an outside opinion.” That’s the mistake.

An independent adjuster may be perfectly professional. Many are. But professional doesn’t mean aligned with you. Their assignment still comes from the insurer. Their role is to inspect, estimate, and move the claim for the carrier.

A private claims adjuster is closer to your side’s claim manager. The situation is comparable to a business dispute. The insurer has its own file, its own estimating approach, and its own interpretation of what is covered. You need someone building your file with equal discipline.

The most important question to ask any adjuster is simple. “Who do you work for on this claim?”

Where technology adds another layer

Carriers and vendors increasingly rely on remote tools, fast photo review, and workflow systems to move claims. Some of that is efficient. Some of it misses context that only appears in a full site inspection and careful policy review. If you want a sense of how insurers are streamlining intake and review behind the scenes, this piece on automated claims processing gives useful background.

That doesn’t make automation bad. It means policyholders should be careful about assuming speed equals accuracy.

The test I tell neighbors to use

Ask these questions before you talk details:

- Who signed your work order: If the insurance company did, that adjuster is on their side.

- Who pays you: If your fee comes from the insurer, your duty runs to the insurer.

- Can you negotiate only for me: A licensed public adjuster can answer yes.

If the answers are fuzzy, stop and verify before the claim gets too far down the road.

The Tangible Benefits of Hiring Your Own Adjuster

A private claims adjuster earns their keep in the less visible aspects of the claim.

The obvious assumption is that this is about “getting more money.” The better way to say it is this. It’s about getting the claim measured correctly, presented correctly, and negotiated from the policyholder’s side instead of waiting for the insurer to define the loss for you.

Where results come from

Industry benchmarks show that policyholders who hire a private claims adjuster often see final settlements increase by 200-700%, based on benchmarks cited here. That outcome doesn’t happen because someone argues louder. It happens because the claim gets built with more detail, better support, and stronger policy application.

A good adjuster doesn’t walk through a damaged house and stop at “replace drywall.” They look at what caused the loss, how far conditions spread, what hidden materials need opening, whether smoke or moisture migrated, whether code requirements apply, and how the policy wording affects valuation.

What the work actually looks like

This is the difference between a rough complaint and a documented claim:

- Damage documentation: Photos, room-by-room inventory, cause analysis, mitigation records, contractor input, and written scope tied to what was affected.

- Policy interpretation: Reading coverage sections, exclusions, endorsements, and valuation language closely enough to know where the carrier’s reading is too narrow.

- Estimating: Using tools like Xactimate and comparing line items against what the loss really requires, not just what fits a quick inspection.

- Negotiation: Responding to under-scoped estimates, omitted items, depreciation disputes, and soft denials with organized evidence.

One option policyholders in Oregon and Washington consider is the benefits of hiring a public adjuster, especially when the loss includes fire, water migration, structural issues, or business interruption.

A weak claim file invites a low evaluation. A well-built file forces a better conversation.

What doesn’t work

Some homeowners try to manage a major loss by piecing together contractor bids and forwarding emails to the carrier. That can help on a small, straightforward claim. It usually falls apart on complex losses.

Here’s what commonly goes wrong:

- Contractors price repairs, not coverage: They may be excellent builders and still not document the claim in policy language.

- Owners focus on visible damage: Hidden moisture, smoke contamination, and code-triggered work get missed.

- The file becomes reactive: Instead of presenting the full claim, the owner keeps answering the insurer’s narrower version of events.

That’s why representation matters most when the claim is complex, disputed, or too big to improvise.

Understanding Adjuster Fees and Contracts

The fee question is often asked with some hesitation, which makes sense. You’ve just had a loss. Cash flow is tight. Temporary housing, cleanup, missed work, and uncertainty are already taking a toll.

So let’s make this plain. A private claims adjuster usually works on a contingency fee. The common idea is simple. If the claim recovery improves, the adjuster gets paid from the settlement according to the written agreement.

Why contingency matters

The median annual wage for claims adjusters, examiners, and investigators was $76,790 in May 2024, and compensation structures vary widely. Public adjusters typically work on a contingency fee based on the settlement outcome, which aligns their financial interest with maximizing the policyholder’s recovery, according to the Bureau of Labor Statistics occupational overview.

That alignment is one reason many policyholders prefer this model. You’re not paying hourly while wondering whether the claim is moving. The adjuster has a direct stake in the result.

What to look for in the contract

Before signing, slow down and read every page. If you want a second set of eyes on contract language in general, a practical contract review checklist can help you spot provisions that deserve a closer look.

Focus on these points:

- Fee basis: Is the percentage applied to the total recovery, or only to new money recovered after the current offer?

- Scope of work: Does the agreement cover inspection, estimating, contents, negotiation, supplements, and re-opened issues if they arise?

- Termination language: If you end the relationship, what happens next?

- Communication terms: Who speaks to the insurer, and how often should you expect updates?

A detailed explanation of public adjuster cost is worth reviewing before you sign any agreement.

What a clean agreement feels like

A good contract should read like a working plan, not a trap. You should understand who does what, when fees are earned, and what authority you’re giving the adjuster.

Client advice: If you can’t explain the fee arrangement back in your own words, don’t sign yet.

The wrong way to hire a private claims adjuster is under pressure at the curb, on the first day, after a fast sales pitch. The right way is to verify the license, read the contract, ask uncomfortable questions, and make sure the relationship is clear before anyone starts negotiating on your behalf.

A Practical Checklist for Hiring a Private Adjuster

The market gets noisy after a major storm or fire. Trucks show up fast. So do salespeople. Some are legitimate. Some are not people you want anywhere near your claim.

Use a checklist. It keeps you from making a rushed decision when you’re tired and overloaded.

Start with licensing and location

The first filter is simple. Verify that the person is licensed as a public adjuster in the state where your loss occurred.

If you’re in Oregon or Washington, don’t rely on a business card or a social media profile. Check directly with the state regulator. That matters because a private claims adjuster should be licensed to represent policyholders. An independent adjuster’s license is not the same thing, and that distinction is exactly where many homeowners get tripped up.

Also ask where they work. Local knowledge matters. Oregon and Washington claims often involve regional construction pricing, weather-related damage patterns, local permitting issues, and practical rebuild realities that out-of-state storm chasers may not understand well.

Questions worth asking on the first call

Use direct questions. You don’t need polished insurance language.

- “Do you represent only policyholders?” If the answer wanders, keep looking.

- “Have you handled losses like mine in this area?” Fire, water, wind, and commercial losses each bring different problems.

- “Will you inspect the property yourself?” You want to know who is performing the work.

- “How do you build the claim?” Listen for specifics such as scope documentation, estimating software, contents, and policy review.

- “How are your fees calculated?” If the explanation is slippery, that’s a warning sign.

Review the paperwork before emotion takes over

Some policyholders wait until they feel desperate, then sign whatever is put in front of them. That’s exactly when mistakes happen.

Read the agreement line by line. Make sure the fee structure, scope, cancellation terms, and communication expectations are written clearly. If an adjuster resists giving you time to review the contract, move on.

You should also ask what happens if the carrier has already issued a payment, denied part of the claim, or assigned multiple field adjusters. Experienced representation can still help in those situations, but the contract should reflect what work is being taken on.

Look for signs of a disciplined practice

A reliable private claims adjuster usually has a process. Not a slogan. A process.

That may include site inspection, policy review, photographic documentation, estimate preparation in Xactimate, contents handling, and structured communication with the insurer. If you’re trying to decide when to hire a public adjuster, the answer is often earlier than people think, especially when damage is extensive or the carrier’s first scope feels incomplete.

If someone promises a huge result before they’ve read the policy and inspected the loss, they’re selling confidence, not doing adjusting.

A quick red-flag list

| Red flag | Why it matters |

|---|---|

| They call themselves independent but say they help everybody | That wording often hides who they actually represent |

| They push for an immediate signature | Pressure is the enemy of good hiring decisions |

| They can’t explain their fee cleanly | Confusion now usually becomes conflict later |

| They avoid local references | You need evidence of real claim work, not general sales talk |

| They speak only in settlement hype | Serious adjusters talk about documentation, scope, and policy terms |

The best hiring decision usually feels calm, not flashy.

Real World Scenarios When a Private Adjuster is Essential

Some claims can be handled without much friction. Others become technical fast. These are the situations where a private claims adjuster stops being a convenience and becomes a practical necessity.

The commercial fire with two losses at once

A business suffers a fire in the back of the building. The obvious damage is the charred area, cleanup, and repairs. The less obvious damage is the interruption to operations, inventory disruption, delayed reopening, and the documentation needed to present the loss in a way the insurer can evaluate fully.

In that kind of file, property damage and income loss are tied together. If the claim isn’t organized from the start, one side gets attention and the other gets neglected.

The water loss that looked smaller on day one

A homeowner sees stained drywall after a plumbing failure. The insurer’s early estimate addresses surface repairs. Later, demolition reveals trapped moisture, insulation damage, cabinet impact, flooring spread, and conditions that weren’t visible during the first walk-through.

That’s a common turning point. The issue isn’t whether water caused damage. The issue is how far the documented scope follows the actual path of the loss. Without somebody pushing the file forward with revised support, the original estimate can anchor the whole claim.

The overwhelmed family who just can’t manage one more thing

This is more common than people admit. A retired couple, a family with small children, or a business owner already stretched thin may understand the claim process in theory and still be unable to manage it well in practice.

They’re juggling temporary housing, work obligations, cleanup decisions, receipts, contractor calls, and insurer emails. A private claims adjuster becomes the point person who keeps the file moving, organizes the evidence, and takes the negotiation burden off the owner’s shoulders.

Sometimes the value isn’t just technical. It’s having one experienced person carry the claim when you no longer can.

Frequently Asked Questions About Private Adjusters

Is it too late to hire a private claims adjuster if I already started the claim

Usually, no. Many people bring in help after the insurer has already inspected, issued an estimate, or paid part of the claim. The key question is whether important parts of the loss are still under review, underpaid, or poorly documented.

Does hiring a public adjuster make me look hostile to my insurance company

No. It’s a standard form of representation. You’re not breaking the relationship. You’re making sure your side of the claim is prepared and presented professionally.

Are private and public adjusters the same thing

In everyday use, yes. People often say private claims adjuster when they mean a licensed public adjuster who represents the policyholder. What matters most is confirming that the adjuster works only for you on that claim.

When might hiring one not make sense

If the loss is small, straightforward, and fully accepted by the insurer, the fee may not be worth it. The more technical, high-value, disputed, or time-consuming the claim becomes, the more useful representation usually is.

What should I do before signing with any adjuster

Verify the license, read the contract, ask who they represent, and make sure they can explain how they will document and negotiate your specific type of loss. If you still feel confused after the conversation, keep interviewing.

If you’re dealing with a fire, water, storm, vandalism, or commercial property loss in Oregon or Washington, NW Claims Management is a licensed public adjusting firm that represents policyholders, not insurers. They handle claim documentation, policy review, damage assessment, and negotiation on a contingency basis, and they offer a free claim evaluation if you need help understanding your options.