You rent an apartment, you’ve paid your premium on time, and then a fire, theft, or major water loss wipes out the things you use every day. The insurer asks for an inventory. You list your TV, laptop, shoes, cookware, bedding, and furniture. Then the first payment arrives, and it’s nowhere near what it will cost to rebuild your life.

That shock usually comes from one detail people miss when they buy a policy. They assume “my stuff is covered” means the insurer will pay what it costs to replace it today. Often, that’s not how the policy works.

From a public adjuster’s perspective in Portland, this is one of the most common and expensive misunderstandings in renters claims. Replacement cost renters insurance can make the difference between a manageable recovery and a financial mess. But even good coverage has a catch. You still need to know how insurers value property, how the claim process unfolds, and where the cash-flow pressure hits.

Why Your Standard Renters Policy Might Fail You

A lot of renters find out what their policy really does on the worst day possible. A kitchen fire gets out of control, the sprinkler line breaks upstairs, or someone clears out the apartment while you are at work. You report the loss, list everything you owned, and assume the carrier will pay what those items cost to replace. Then the estimate comes back based on actual cash value.

That distinction is where a standard renters policy can fall short. The policy may cover the loss, but it can still value your property as used, worn, and partly expired. For electronics, furniture, clothing, and household basics, that usually means a settlement well below what it takes to buy replacements today.

A five-year-old laptop is a good example. The insurer may agree it was covered and still pay only a depreciated amount because it was no longer new. If you have to replace that laptop this week, the gap comes out of your pocket.

Where renters get blindsided

The first problem is assuming “covered” means “enough money to replace it.”

The second problem is trusting the carrier’s first valuation without checking the math. In contents claims, depreciation is one of the simplest ways for an insurer to cut the initial payment while staying inside the policy language. I see that all the time. If the inventory is vague, the item descriptions are weak, or the age assigned by the carrier is off, the settlement drops fast. That is why renters should know how to spot insurance adjuster tactics that reduce contents payouts.

There is also a cash-flow issue people miss. Even when the loss is clearly covered, an ACV policy leaves you funding the difference between a used-value check and the actual cost of replacing your property. After a large loss, that can mean buying a mattress, work clothes, cookware, and electronics with money you do not have available.

Practical rule: If your contents are settled on ACV, the insurer can pay the claim correctly under the policy and still leave you short on the items you need right away.

The Financial Impact of ACV on Large Claims

Small losses can hide this problem. A depreciated payment on one lamp or one coffee table is annoying. A depreciated payment on nearly everything you own becomes a budget crisis.

Major renters claims are rarely about a single item. They involve beds, linens, kitchen goods, shoes, coats, chargers, desks, TVs, and the ordinary things that make an apartment livable. Once depreciation is applied across the full inventory, the shortfall can be substantial. That is the practical weakness in a standard policy. It often protects the insurer’s balance sheet better than your recovery.

What Is Replacement Cost Renters Insurance?

Replacement cost renters insurance pays what it costs to buy new items of similar kind and quality at today’s prices, without subtracting depreciation. That’s the clean definition. In practice, it means your claim is built around the cost of replacing what you had, not the garage-sale value of used property.

Think of a stolen laptop, a damaged couch, or a destroyed set of kitchen items. Under replacement cost coverage, the carrier looks for the current price of comparable new items. Under actual cash value, the carrier starts with replacement cost and then takes money off for age, wear, and expected useful life.

The trade-off is simple

You pay more for better claim economics. According to Policygenius on replacement cost renters coverage, RCV policies typically cost about 10% more than ACV policies.

That premium difference is usually modest compared with what depreciation can strip out of a claim. The issue isn’t whether the endorsement costs more. It does. The key question is whether you want to fund depreciation yourself after a loss.

How insurers actually pay these claims

Most renters assume a replacement cost claim means one full check right away. That usually isn’t how it happens.

Insurers commonly use a two-step payout. They first issue an ACV payment after they review the loss documentation. Then they release the withheld depreciation after you replace the item and submit receipts. The structure matters because it changes how much cash you need on hand while you’re trying to recover.

Here’s the practical difference:

| Coverage type | How the insurer values property | What you usually receive first | What you may need to do next |

|---|---|---|---|

| ACV | Current used value after depreciation | Depreciated amount, less deductible | Accept lower payout or dispute valuation |

| RCV | Cost of a new comparable item | Often ACV first, less deductible | Replace item, submit receipts, recover depreciation |

The policy can say “replacement cost” and still require proof that you actually replaced the property before the carrier pays the holdback.

What works and what doesn’t

What works is reading the contents settlement language before you have a claim. Verify whether personal property is ACV or RCV, and ask how recoverable depreciation is handled.

What doesn’t work is assuming your agent selected the better option automatically. Many renters only find out they had ACV when they’re already displaced, stressed, and trying to buy basic necessities again.

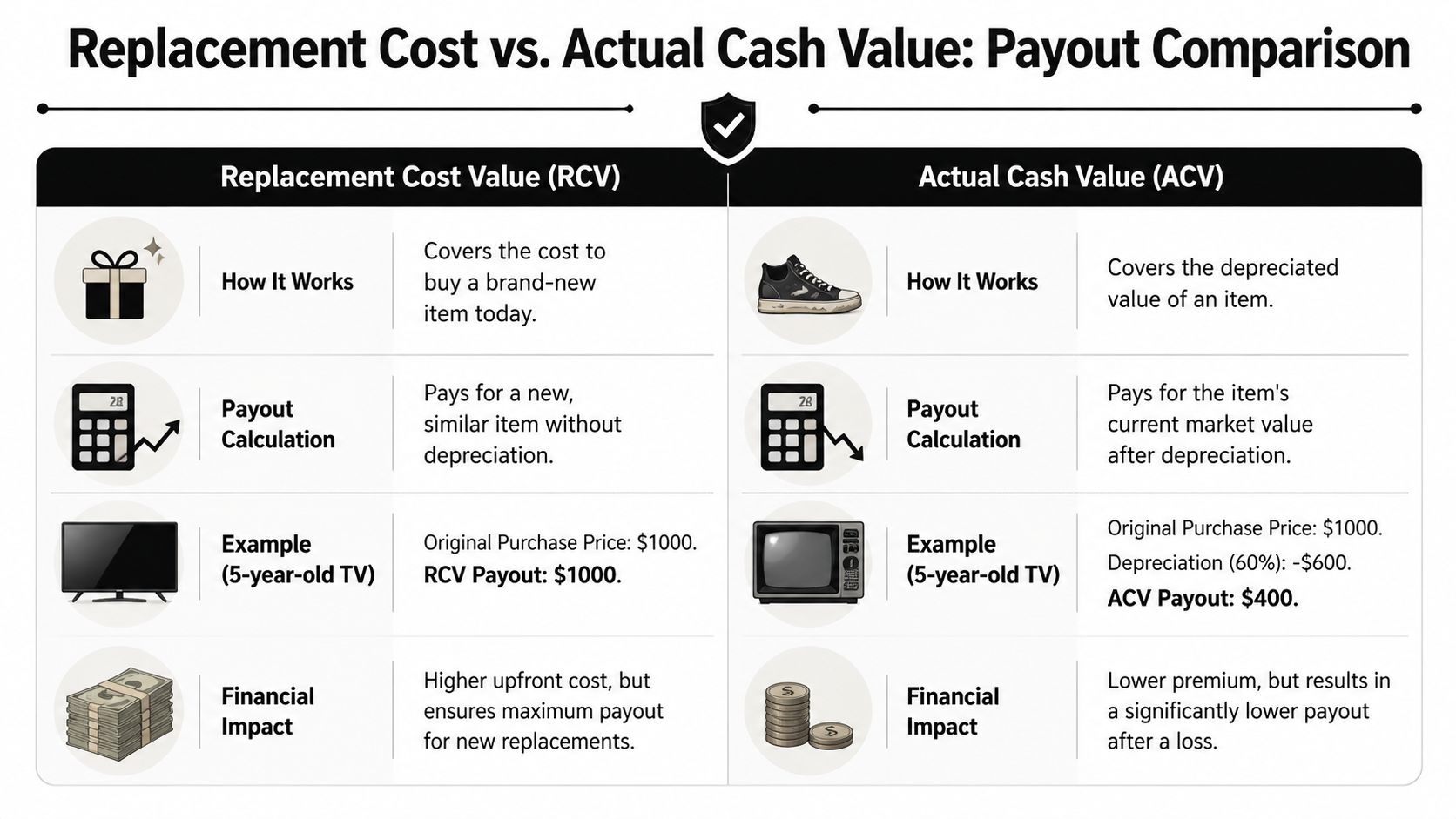

RCV vs ACV A Detailed Payout Comparison

A fire destroys a renter’s apartment on a Friday night. By Saturday morning, they need clothes, chargers, toiletries, shoes, a laptop for work, and a place to sleep. The policy says replacement cost, so they expect enough money to start over. Then the first payment arrives based on depreciated value.

That gap is where many renters get squeezed.

ACV and RCV do not just change a spreadsheet. They change how much cash you need during the first days and weeks of a claim, and they change how much room the carrier has to argue over quality, age, and condition. From the adjuster side, I see the same pattern often. A full contents loss is rarely about one expensive item. It is about 150 ordinary items, each discounted in a way that feels small until you total them.

A side-by-side example

| Item | Original purchase | Age | Likely ACV outcome | Likely RCV outcome |

|---|---|---|---|---|

| Television | $1,000 | 5 years | About $400 after depreciation | $1,000 for a new comparable TV |

| Laptop | $800 | 5 years | Potentially $400 to $600 | $1,200 if that’s the current replacement cost |

| Sofa | Varies | Used | Reduced for wear, age, and condition | New comparable sofa at today’s price |

| Kitchen appliances and smallwares | Varies | Mixed | Reduced item by item | New comparable replacements |

Those examples show the core issue clearly. Under ACV, the carrier pays what your used property was worth right before the loss. Under RCV, the policy is aimed at what it costs to buy a new comparable item today, subject to the policy terms and your follow-through on replacement.

The trade-off is practical, not theoretical. ACV can mean a lower premium, but it shifts more of the recovery cost onto you after a loss. RCV usually gives better protection, yet many policies still pay in stages, with depreciation held back until you replace the property. If cash is tight, that holdback can delay your recovery even when the policy language is better.

Where carriers press their advantage

Insurers do not usually fight over the fact that you owned socks, pots, or towels. They fight over quality and price point. If your inventory says “toaster,” they may price a basic model. If you lost a higher-end stainless model with multiple settings and a longer warranty, that difference matters across dozens of items.

The same thing happens with clothing, cookware, office equipment, and furniture. Generic descriptions produce generic pricing. Generic pricing lowers the settlement.

That is why inventory quality directly affects payout quality.

Build the comparison the way an adjuster would

A credible contents claim should show what the item was, what a comparable replacement costs now, and why that replacement is reasonably matched to what you lost. Use this process:

- Document by room. Keep the list organized so the carrier cannot collapse multiple items into one vague category.

- Use specific descriptions. Brand, model, size, material, and notable features all matter.

- Support pricing with current retail sources. Use actual listings for comparable items, not rough guesses.

- Separate premium items from basic items. A carrier will often default downward unless the file shows otherwise.

- Track your policy cap before you argue price. If your total loss exceeds your contents limit, valuation fights may matter less than the size of your overall limit. Review how insurance policy limits work before assuming every item will be paid in full.

A thin inventory gives the insurer room to substitute lower-grade items, apply heavier depreciation, and close the file cheaply.

The payout difference across a real apartment

A renter rarely loses one TV and one laptop. They lose bedding, coats, shoes, dishes, cleaning tools, food storage containers, headphones, lamps, chargers, desk equipment, and the drawer full of things nobody remembers until they are gone. ACV reduces many of those items sharply because they are used property. RCV can make you whole on paper, but only if the item descriptions are strong and you meet the replacement requirements in the policy.

That is the practical comparison. ACV lowers the value of what you lost. RCV improves the outcome, but it still demands documentation, receipts, and enough cash flow to get through the holdback period.

Calculating Your Ideal Coverage Amount

Most renters pick a personal property limit quickly and move on. That’s understandable, but it’s where underinsurance starts. The right coverage amount comes from your inventory, not from a guess.

The fastest workable method is a room-by-room count paired with current replacement pricing. Don’t focus only on headline items like a TV or laptop. The expensive surprise in many claims is volume. Clothing, shoes, coats, linens, cookware, utensils, small appliances, office gear, cleaning supplies, and personal care devices add up fast when you price them all new.

![]()

How to build a realistic contents value

Start with broad categories, then drill down.

- Bedroom contents include mattresses, frames, dressers, nightstands, lamps, bedding, clothing, shoes, luggage, and jewelry storage.

- Living area contents include sofas, chairs, tables, rugs, bookshelves, TVs, speakers, streaming devices, artwork, and decor.

- Kitchen contents usually surprise people most. Plates, glasses, cookware, knives, pantry containers, coffee equipment, small appliances, and food-storage systems can represent a major chunk of value.

- Work and hobby property matters too. Monitors, printers, cameras, musical instruments, bicycles, gaming gear, and tools may need closer review.

The silent exposure most renters miss

Inflation changes replacement math even when your lifestyle hasn’t changed. Obie’s replacement cost discussion notes that a home insured for $300,000 five years ago may now require over $400,000 to rebuild. The same principle applies to personal property. Renters think they’re fully covered because they haven’t changed apartments, but the cost to replace what they own may have climbed far beyond the limit they selected earlier.

That’s why coverage reviews shouldn’t be one-and-done. Recalculate after major purchases, after a move, after furnishing a room, or when replacement prices have plainly shifted.

Read the policy language that matters

A good renters policy still has limits. Replacement cost coverage on contents does not eliminate your overall personal property cap. If your total inventory exceeds the policy limit, the RCV endorsement won’t magically create extra money above that limit.

Look closely at:

| Policy feature | What to check | Why it matters |

|---|---|---|

| Personal property limit | Total contents cap | RCV still stops at the policy limit unless you have added protection |

| Special limits | Jewelry, electronics, collectibles, other categories | Certain categories may have tighter caps than you expect |

| Settlement terms | Whether depreciation is recoverable | Determines how and when you receive the full replacement amount |

If you’re trying to sort out valuation after a major loss, a professional property damage assessment can identify where your coverage is adequate and where it isn’t.

Field note: The best inventory is the one you can hand over fast, with enough detail that the carrier can’t downgrade your belongings into bargain-bin equivalents.

Essential Endorsements and Common Exclusions

A solid replacement cost endorsement improves the way your contents are valued. It doesn’t erase exclusions, sub-limits, or category-specific problems. Consequently, many renters learn that “good coverage” and “complete coverage” are not the same thing.

Standard renters policies commonly exclude some causes of loss entirely, and they often limit recovery for specific classes of property unless you add endorsements. If you own jewelry, art, collectibles, specialty electronics, or other high-value items, standard policy language may not be enough. Scheduling those items or adding the right rider can matter just as much as choosing RCV.

A claim that goes right

A renter loses a large portion of their apartment contents after a covered fire. Their policy includes replacement cost coverage, and before the loss they kept a photo inventory, copies of receipts, and serial numbers for electronics. That documentation speeds up the first review because the carrier can match item descriptions to current market equivalents.

The renter also had an extended replacement cost endorsement on contents. That turns out to matter because replacement pricing after the loss is higher than expected. Without that endorsement, the policy limit would have created a shortfall.

The endorsement worth asking about

Kin’s explanation of extended replacement cost coverage notes that this endorsement can provide a buffer of 20% to 50% above your policy limit. In a renter example, if you have a $30,000 limit and replacement needs rise to $35,000, the endorsement can cover that $5,000 gap that would otherwise come out of your pocket.

That kind of buffer matters after widespread loss events, when replacement prices can jump and supply gets tight.

Common mistakes after a loss

- Assuming all causes of loss are covered. Renters often discover too late that some events require separate protection.

- Ignoring category limits. A policy can have generous overall contents coverage and still restrict payout on certain types of property.

- Buying RCV but skipping limit reviews. Better valuation doesn’t help if the total policy cap is too low.

The renters who recover best usually did two things before the loss. They bought replacement cost coverage, and they matched it with endorsements that addressed the weak spots in the base form.

Navigating The RCV Claim Process

The claim starts before the paperwork. It starts the moment you realize the apartment isn’t livable, property is missing, or water or smoke has affected what you own. The first priority is safety. After that, your job is to preserve evidence and control the record the insurer will use.

The first moves that matter

Notify the landlord, notify the carrier, and document everything before cleanup changes the scene. Take wide photos, close photos, and video. Save emails, text messages, and emergency-response paperwork. If theft is involved, keep the police report with your claim file.

The sequence is similar to other property claims. If you want a plain-language look at how insurers expect losses to be documented, this guide on how to file a roof insurance claim is useful because the core habits are the same: document early, preserve evidence, and don’t assume the carrier will fill in the blanks for you.

What the insurer is looking for

Carriers want a list they can process. That means item description, age if known, original cost if known, quantity, and current replacement equivalent. If your list is vague, the insurer usually fills in the missing details in a way that helps the insurer.

Use this claim checklist:

- Photographic proof. Capture rooms as they were found, not after sorting and disposal.

- Receipts and statements. Pull order histories from Amazon, Best Buy, Apple, Target, Costco, and similar retailers.

- Model information. For electronics and appliances, serial and model numbers reduce arguments over quality level.

- Replacement research. If the carrier substitutes a lower-grade item, answer with current listings for like kind and quality.

- Communication log. Record who said what, and when.

If you need a broader roadmap, this summary of the home insurance claim process tracks the stages most policyholders face once the file is opened.

The adjuster on the file may be polite and still use valuation choices that cut your claim. Courtesy and fair pricing are not the same thing.

When to push back

Push back when descriptions are wrong, quality is downgraded, quantities are reduced, or payment stalls at the ACV stage without a clear path to recover depreciation. Replacement cost coverage only works if the withheld amounts are released when you comply with the policy requirements.

Many renters get tired halfway through. That’s exactly when money gets left behind.

Maximizing Your Claim and When to Call a Public Adjuster

The biggest catch in replacement cost renters insurance isn’t the endorsement itself. It’s the cash-flow burden that arrives after the loss. A lot of policies require you to buy the replacement item first, then submit proof before the insurer releases the withheld depreciation.

That means the policy may promise full replacement value and still force you to front the money. For a renter displaced by fire or major water damage, that can be brutal. You may be paying for temporary housing, replacing daily necessities, missing work, and trying to rebuild a home all at once.

Experian’s discussion of replacement cost versus actual cash value notes that replacement cost policies can require policyholders to pay out of pocket before getting full reimbursement, creating a cash-flow crisis. It also notes that public adjusters can negotiate for advance payments from the insurer to help bridge that gap.

Where carriers commonly reduce the payout

Insurers don’t need to deny a claim outright to save money. More often, they trim it in smaller ways:

- They challenge like kind and quality. Your midrange or premium item becomes a basic substitute in the estimate.

- They depreciate aggressively. Older furniture and electronics take heavy reductions in the first payment.

- They demand more proof than renters expected. Missing receipts, weak photos, or incomplete inventories slow release of withheld depreciation.

- They let delay do the work. A renter under financial pressure may accept less just to move on.

When handling it yourself stops making sense

A simple theft claim with clear receipts and a short item list may be manageable on your own. A major fire, major water loss, smoke damage claim, or apartment-wide contents loss is different. The valuation work gets technical quickly. So does the negotiation.

A public adjuster changes the dynamic because the file stops being built only by the insurer. The policyholder has someone documenting the contents properly, pricing replacements against real market comparables, challenging weak substitutions, and pushing for the payments the policy allows.

This is especially important in replacement cost claims because the work doesn’t end with the first check. Someone has to track recoverable depreciation, organize receipts, and push the carrier to release what’s still owed.

What practical claim help looks like

A strong claim strategy usually includes:

- A full inventory built to current market replacement standards.

- Documentation that supports quality level, not just item existence.

- A review of policy wording for depreciation holdbacks and payment timing.

- Requests for interim or advance payments when the facts support them.

- Pressure on the carrier when the file stalls or valuation slips.

Straight answer: If the loss is large enough that a bad valuation changes your ability to recover, professional representation is usually worth considering.

The right time to call a public adjuster is early, before weak descriptions and underpriced line items harden into the insurer’s official claim record. If you’re weighing the value of representation, this overview of the benefits of hiring a public adjuster gives a clear sense of what that advocacy changes.

Replacement cost coverage is better than ACV. But the endorsement alone doesn’t protect you from underinsurance, poor documentation, delayed depreciation recovery, or cash-flow pressure. The renters who recover best are the ones who prepare before the loss and manage the claim actively after it.

If you’re dealing with a renters insurance claim in Oregon or Washington and need a serious review of your policy, valuation, or payout, NW Claims Management can help. Their team represents policyholders, not insurers, and works through documentation, valuation disputes, settlement negotiations, and cash-flow issues that often derail replacement cost claims.