When your property is harmed, the term 'damage' seems simple enough. But in the world of insurance claims, its specific legal meaning is the bedrock of your entire case.

At its core, the damage legal definition points to the actual physical harm or loss that reduces a property's value or stops it from working as it should. It’s the tangible, visible hurt—the cracked foundation, the waterlogged floors, or the smoke-stained walls after a fire.

What Does Damage Legally Mean in an Insurance Claim

While you might use the word casually, your insurance policy views damage as a precise legal concept. Think of it as the physical evidence of your loss. Your home is functioning perfectly one minute, and the next a pipe bursts. The resulting warped floorboards and ruined drywall are the damage.

This idea is the starting point for every property claim. The legal world generally defines property damage as an 'injury to real or personal property through another's negligence, willful destruction or by some act of nature,' a principle well-documented by sources like the Cornell Law School Legal Information Institute. This definition is critical because it covers both your house itself and everything you own inside it.

Getting a firm grip on this term is the first step, as it shapes how you identify and report every single aspect of your loss to the insurance company.

Damage vs. Damages: A Critical Distinction

Here’s where many policyholders get tripped up. The words "damage" and "damages" sound almost identical, but in a claim, they represent two completely different things. Nailing this difference is absolutely essential for a successful recovery.

To put it simply:

- Damage is the physical harm your property has sustained.

- Damages is the money the insurance company owes you to fix that harm.

Let's quickly compare the two side-by-side.

Damage vs Damages Key Differences

| Term | Meaning | Example |

|---|---|---|

| Damage | The physical harm or injury to property. | The hole in your roof and the water stains on the ceiling after a storm. |

| Damages | The monetary compensation paid to repair the harm. | The $25,000 settlement you receive to fix the roof and ceiling. |

Understanding this table is key to communicating effectively with your adjuster.

Think of it like this: A kitchen fire causes damage. The insurance company pays you damages (the money) so you can hire contractors to rebuild it.

Why does this matter so much? Your entire goal is to thoroughly document all the damage so you can prove you are owed the appropriate damages to make you whole again. This small shift in vocabulary gives you the power to speak the insurer's language and confidently advocate for the fair settlement you deserve.

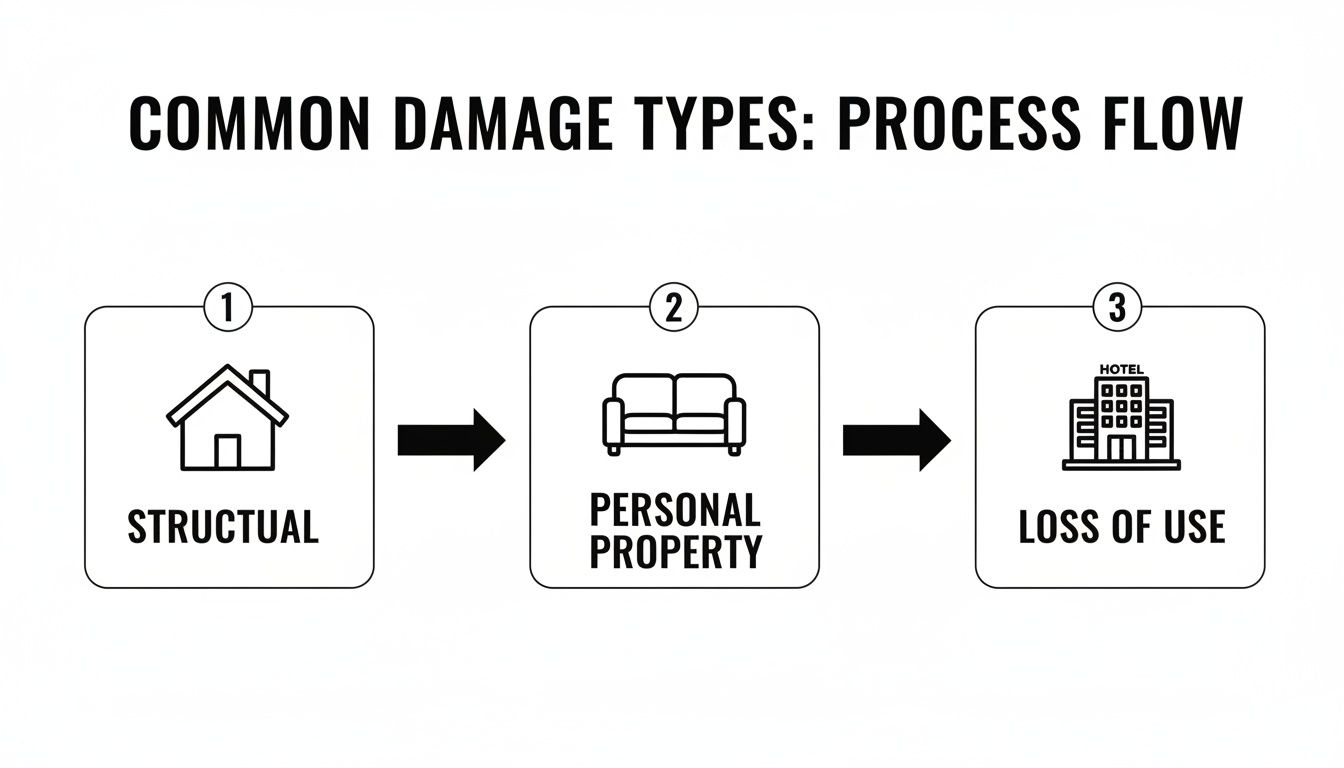

Common Types of Damage Covered by Your Policy

Think of your insurance policy less like a single, all-encompassing safety net and more like a specialized toolkit. Each tool is designed for a very specific type of harm, and knowing which tool to use is the key to a successful claim.

Getting this right from the start is crucial. When you can correctly categorize the losses you've suffered, you're not just organizing paperwork—you're building the foundation for a smoother claims process and making sure no covered damage gets overlooked.

Structural and Personal Property Damage

The most obvious type of loss is structural damage. This is any physical harm to the fixed parts of your building: the foundation, walls, framing, and roof. I've seen it a thousand times in the Pacific Northwest—a winter windstorm sends a massive Douglas fir crashing through a client's roof, splintering trusses and exposing the entire home to the elements. That's a classic, clear-cut case of structural damage.

But the damage doesn't stop with the building itself. You also have personal property damage, which covers all your movable belongings. It’s the furniture, the electronics, the clothes in your closet, the books on your shelves. If that same storm surge causes a power spike that fries your TV and computer, or the roof leak ruins your grandmother's antique rug, that's a personal property loss.

Insurance policies draw a hard line between these categories, and your coverage amounts will differ for each. While standard liability coverage often falls in the $25,000 to $50,000 range, the limits for your own property are spelled out in your specific policy declarations.

Additional Living Expenses and Business Losses

What happens when the damage is so bad you can't even stay in your home? This is where your Loss of Use coverage kicks in, often called Additional Living Expenses (ALE). This is an incredibly important part of your policy. It covers the additional costs you incur by having to live somewhere else—things like a hotel stay, laundry services, and the extra expense of eating out while your kitchen is being rebuilt. The goal is to help you maintain your normal standard of living.

For local business owners here in Oregon and Washington, the situation gets another layer of complexity. Business property damage covers the physical harm to your commercial building, equipment, and inventory. A fire in a restaurant's kitchen that destroys the cook line and spoils thousands of dollars in food is a perfect example.

But what about the money you aren't making? That's where Business Interruption coverage becomes a lifeline. It’s designed to replace the income your business loses while it’s shut down for repairs, helping you cover ongoing expenses like payroll and rent even when no money is coming in.

Each of these categories demands a different kind of proof and documentation. Understanding how your policy's limits and deductibles apply to each type is non-negotiable. To get a better handle on these financial thresholds, you can learn more about how insurance policy limits are explained in our guide. Correctly identifying every type of damage you’ve suffered is the first step toward securing the full settlement you’re owed.

How to Document Damage and Build a Stronger Claim

What you do in the moments and days right after a loss can make or break your insurance claim. Think of yourself as an investigator building a case. Every photo, every receipt, and every note you take is a piece of evidence that proves the full extent of your damage.

Your first job is to capture everything before any cleanup or repairs begin. This creates a baseline—a snapshot in time that shows the insurance company exactly what happened. Start with the big picture and then zoom in on the details.

Build Your Evidence File

First, take wide-angle photos and videos of all affected rooms and the exterior of your property. Get shots from different corners of the room to provide a full 360-degree view of the scene.

Then, get up close. Don't just snap a picture of a collapsed ceiling. Document the waterlogged insulation, the ruined light fixture, and the dust-covered furniture below. This level of detail makes it nearly impossible for an insurer to downplay the initial scope of the loss.

As you document, remember to:

- Shoot video walkthroughs. A slow, narrated video is incredibly effective. Walk through the damaged areas, explain what you’re seeing, and describe what no longer works.

- Don't throw anything away. Resist the urge to clean up and toss damaged items. A pile of ruined belongings is powerful, tangible proof. Wait until your adjuster has seen everything or gives you the green light.

- Keep a communication log. Every time you talk to your insurance company, write it down. Note the date, time, the representative's name, and a summary of your conversation.

Your goal is to document every category of loss you've sustained, from the structure itself to the contents inside and the costs of being displaced.

Itemize and Track Every Single Loss

Your most valuable tool in this process will be a detailed inventory list. Go room by room and list every single item that was damaged or destroyed. For each one, note its description, brand, approximate age, and what you paid for it, if you can remember. This applies to everything from your sofa and television down to individual shoes and books.

Crucial Tip: Immediately start a folder for all receipts related to the loss. This includes any money you spend on temporary repairs (like boarding up a window), as well as all your additional living expenses if you've had to leave your home. Hotel bills, restaurant meals, and laundry services are often covered under your policy.

Solid record-keeping is the foundation of a successful claim, and many of the same principles apply to professional legal document management.

This is where having an expert on your side truly pays off. We are trained to spot the "hidden" damage that homeowners almost always miss—things like faint smoke damage inside a wall cavity or subtle electrical issues caused by a minor water leak. A thorough property damage assessment conducted by a professional ensures every bit of your loss is found, valued correctly, and included in your claim. We make sure no money is left on the table.

Navigating Oregon and Washington State-Specific Laws

Insurance laws are not a one-size-fits-all deal. What works for a claim in California or Texas might be completely irrelevant here in the Pacific Northwest. For property owners in Oregon and Washington, understanding our local legal quirks isn't just a good idea—it’s absolutely critical for getting a fair settlement.

These state-specific rules are the playbook that determines your rights and your insurance company's obligations.

One of the most important concepts that differs from state to state is something called comparative fault. This legal rule decides how to split the bill when more than one person is responsible for an accident. Luckily for us, both Oregon and Washington use a modified version that is very favorable to policyholders.

Understanding Comparative Fault in the PNW

Let’s use a real-world example. Imagine a pipe bursts in your condo, flooding your unit and leaking into your neighbor's place below. After a bit of digging, it turns out the pipe was old, which is on you. However, the investigation also shows the building’s overall water pressure was dangerously high, which is the HOA's fault.

A court might look at this and say you were 20% at fault, while the HOA was 80% at fault.

Thanks to the comparative fault rules here, you can still recover money as long as you aren't considered more responsible than the other party. In this case, you could recover 80% of your losses from the HOA’s insurance. This is a huge deal because it stops an insurer from denying your entire claim just because you had a small hand in the incident.

This principle is a cornerstone of how liability and property damage are handled here, and it’s a world away from the rules in some other states. For a sense of how much these laws can vary, you can even see how other jurisdictions have completely different liability models.

Why Local Laws and Court Rulings Matter

Beyond just fault, the definitions and rules of the game are constantly being shaped by local court rulings and state laws. These precedents can control everything from how quickly an insurer has to respond to you to what "matching" means when only half your siding is damaged. For a wider view on this, there are great resources for mastering state laws beyond federal regulations that highlight the importance of local knowledge.

This is exactly where having a local public adjuster on your side becomes a game-changer. An expert who works exclusively in Oregon and Washington lives and breathes the specific legal landscape that will govern your claim. They put that expertise to work for you.

A local pro can:

- Challenge unfair denials by citing specific state laws and past rulings.

- Negotiate from a place of strength, using relevant local case law as leverage.

- Hold the insurer accountable to all state-mandated deadlines and procedures.

When an insurance company throws a lowball settlement offer your way, they’re often betting you don't know your rights under local law. Having a professional who understands the specific damage legal definition and how it’s applied in our courts instantly levels the playing field.

At the end of the day, filing a claim is so much more than just sending a list of what broke. For a closer look at the nuts and bolts, you can read our guide on how to file a property damage claim. It's about building a solid case, and an expert uses their deep knowledge of state law to make sure you get every penny you're owed.

Why Your Definition of Damage Can Increase Your Settlement

Ever wonder why some insurance settlements feel fair while others fall frustratingly short? The answer often comes down to a single word: damage. How that word is defined is a battleground in almost every claim.

Insurance companies often lean on a very narrow, restrictive definition of "damage" to limit their payout. It’s a strategy designed to protect their bottom line, but it can leave you shouldering the cost for an incomplete repair.

Let's say a kitchen fire scorches a few of your custom cabinets. The insurance adjuster might offer to replace only the three cabinets that were directly burned. On paper, they’ve “repaired the damage.” But now you’re left with a jarring mismatch between the new cabinets and the rest of your original kitchen, tanking your property’s aesthetic and overall value.

This is a textbook move. They’ve addressed the most obvious harm but have completely sidestepped their contractual duty to return your property to its "pre-loss condition." True restoration means making you whole again—not just patching up the scorched, soaked, or broken pieces.

Expanding the Definition to Ensure Wholeness

Our job as public adjusters is to push back against this limited view. We argue that “damage” goes far beyond the directly affected materials. It includes the loss of uniformity, the disruption of function, and the damage to your property’s overall appearance. The "pre-loss condition" you're owed is a kitchen with matching cabinets, not a Frankenstein's monster of old and new.

This broader perspective forces the insurance carrier to address what we call "line of sight" issues.

Here are a couple of real-world examples:

- Matching Materials: Imagine a water leak ruins half the hardwood in your open-concept living room. Simply replacing the damaged planks would create an obvious and ugly patch. By arguing for a complete repair, we can often secure the funds needed to sand and refinish the entire floor, restoring its uniform appearance.

- Consistent Finishes: A storm rips siding off one exterior wall. The new siding will never perfectly match the existing, sun-faded material on the rest of that elevation. A successful claim would cover replacing the siding on the entire wall to ensure a consistent, visually appealing finish.

By successfully challenging the insurance company’s narrow interpretation, we hold them accountable to the full promise of your policy. This is absolutely essential to maximize your insurance claim payout and ensure you aren’t left paying for repair shortfalls yourself. It’s not about getting a windfall; it's about recovering what you’ve truly lost.

How a Public Adjuster Secures Your Financial Recovery

Trying to take on an insurance company by yourself after a major loss can feel overwhelming, like you're fighting a battle you can't possibly win. A public adjuster is your personal champion in this fight—an expert who steps in to manage your claim and secure the full financial recovery you're entitled to by law.

Think of it this way: your insurance provider has a whole team of professionals working to protect its own bottom line. A public adjuster is the expert you put on your side to level the playing field. From there, we systematically tackle every part of the process, from deciphering dense policy language to documenting every last detail of your loss.

Your Advocate in Action

A skilled public adjuster does far more than just fill out forms; we build a rock-solid case for your recovery. It all starts with our own independent and incredibly thorough evaluation of the loss, which often turns up "hidden" damage that the insurance company's adjuster might have missed or minimized.

Here's what that process looks like:

- Policy Analysis: We start by digging into your insurance policy, line by line, to identify every bit of coverage you have available for the structure, your personal belongings, and any additional living expenses.

- Detailed Documentation: We then create a comprehensive inventory of every single damaged item. This isn't just a list; it's backed by photos, videos, and professional estimates for what it will actually cost to repair or replace everything.

- Expert Negotiation: Armed with hard evidence and a deep understanding of the damage legal definition and state laws, we negotiate forcefully with your insurer to counter lowball offers.

This isn't just about getting a payment. It's about getting the maximum settlement your policy allows for.

An investment in a public adjuster is an investment in peace of mind. While you focus on the important work of rebuilding your life or business, your advocate handles the entire claims process, ensuring no money is left on the table.

Our one and only goal is to manage the fight for you, turning a confusing and stressful ordeal into a structured path toward a successful recovery. When you bring in a professional, you gain an ally dedicated to protecting your rights at every turn. If you're looking to dive deeper, you can explore the benefits of hiring a public adjuster to see exactly how we make a difference.

Frequently Asked Questions About Property Damage Claims

When your home or business is damaged, it feels like your world is turned upside down. Suddenly, you're faced with a process filled with confusing terms and rules. We get it. After decades of helping property owners in Oregon and Washington, we've heard just about every question in the book.

Here are a few of the most common ones we tackle, along with answers drawn from real-world experience on the ground.

What Is the Most Important First Step After Damage Occurs?

Before you touch a single thing, grab your phone. Document everything immediately.

Take more photos and videos than you think you need. Get wide shots of the rooms, then close-ups of the specific damage. Record a video where you walk through and narrate what you're seeing. This creates a time-stamped, undeniable record of what the scene looked like before any cleanup or repairs began. An adjuster can argue about costs, but they can't argue with a picture.

Can an Insurer Deny a Claim for an Old Roof or Pipes?

This is a classic insurance company tactic. They might see an older component and immediately try to blame the loss on "wear and tear," but that's not the whole story. An insurance policy is designed to cover sudden and accidental events.

The real question is about the cause of the loss, not the age of the part that failed. Imagine an old pipe in your wall suddenly bursts, flooding your kitchen. While your policy likely won't pay to replace the old pipe itself, it should cover the thousands of dollars in water damage to your cabinets, flooring, and drywall. The sudden burst is the covered event.

Don't let an adjuster shut down the conversation just because something wasn't brand new.

Do I Have to Accept the Contractor My Insurance Company Recommends?

Absolutely not. You are not obligated to use your insurance company’s “preferred” contractor. In fact, you have the right to choose your own licensed, bonded, and insured contractor to fix your property.

Think about it: the insurer's recommended vendor has a primary relationship with the insurance company, and their incentive is often to keep the repair costs down. Choosing your own trusted contractor ensures the focus is on quality and restoring your property to your standards, not just the insurer's budget.

Knowing the true damage legal definition and the rights your policy affords you is how you protect yourself. It's the key to challenging a lowball offer or an unfair denial and getting the resources you need to truly recover.

You don't have to face the insurance company by yourself. The public adjusters at NW Claims Management work only for policyholders in Oregon and Washington. We use our deep expertise to document your claim, negotiate on your behalf, and secure the maximum settlement you are rightfully owed. Get your free claim evaluation today and let us take the fight to them.