The call usually comes after a long night. A tree limb came through the roof in College Park. Wind pushed rain into the attic in Winter Park. A pipe burst while you were out of town, and now the flooring is lifting, the drywall is swollen, and the insurance company wants “documentation” before anyone will say what’s covered.

At that moment, homeowners often search for a public adjuster Orlando residents can trust. Not because they want to fight. Because they need someone who can slow the process down, read the policy correctly, document the loss thoroughly, and deal with the insurer from a position of knowledge instead of panic.

Navigating the Aftermath of Property Damage in Orlando

An Orlando property claim rarely feels simple once you’re living inside it. The roof leak doesn’t stay a roof leak. It turns into wet insulation, stained ceilings, damaged cabinetry, indoor air concerns, and arguments over whether the insurer will pay for repair or full replacement.

A lot of homeowners assume the adjuster sent by the carrier is “their” adjuster. That’s the first misunderstanding that causes trouble. The insurance company’s adjuster evaluates the claim for the insurer. A public adjuster works for the policyholder.

That difference matters most when the damage spreads beyond what’s visible from the driveway.

Who is actually protecting your side

After a storm or sudden water loss, people are juggling mitigation crews, contractor calls, temporary housing questions, and mechanical systems that may no longer be safe to run. If your HVAC took a hit from water intrusion or debris, practical resources on residential HVAC swap-outs can help you understand replacement issues while the claim is still being valued.

A good public adjuster steps into that chaos and does three things fast. They organize the loss, connect the damage to the policy, and present the claim in a form the insurer can’t easily minimize.

Practical rule: The first estimate is often just the starting position, not the final value of the claim.

Why Orlando claims need local judgment

Orlando losses often involve wind-driven rain, roof systems, hidden moisture, and interior damage that develops over days instead of hours. That’s why a generic checklist from a national article often falls short. Local claims work requires attention to roof age, prior repairs, matching issues, mitigation timing, and whether moisture migrated into wall cavities or flooring assemblies.

If you want a broader overview of how the process usually unfolds from first notice through settlement, this guide to the property damage claim process is a useful primer before you start signing anything.

The good news is that the process becomes more manageable once one person takes control of the file and starts building it correctly.

Deciding When to Hire a Public Adjuster

Not every claim needs a public adjuster. Some do. The trick is knowing the difference before you lose advantage.

The strongest reason to hire one is simple. Large claims become technical fast. What looks like “a roof issue” can involve decking, underlayment, insulation, drywall, flooring, electrical components, and code-related repair scope. Once the insurer writes a narrow estimate, the burden usually shifts to you to prove what was missed.

Clear signs you shouldn’t handle it alone

A public adjuster makes the most sense when any of these are true:

- The damage is widespread: Fire, major storm damage, roof failure, water intrusion, or a commercial loss usually creates too many moving parts for a homeowner to document alone.

- The insurer already underpaid or denied part of the claim: Once the carrier takes a position, reversing it takes evidence, not frustration.

- You don’t have time to manage the file: Claims work is administrative and technical. It requires repeated follow-up, estimate review, policy interpretation, and organized submission.

- The damage is partly hidden: Moisture, mold, structural movement, and layered repair issues are where under-scoping starts.

Here’s why that decision can have real financial consequences. A Florida legislative study by OPPAGA found that policyholders who hired public adjusters for 2005 hurricane claims received average payouts of $17,187, compared to $2,029 for those without representation, a 747% increase. For non-catastrophic claims, the increase was 574% (Florida legislative study results).

That doesn’t mean every claim will follow the same pattern. It does mean representation can materially change outcomes when the loss is substantial or disputed.

When a public adjuster may not be necessary

There are also claims where hiring one may not make financial sense.

| Situation | Likely approach |

|---|---|

| Minor, obvious damage with no coverage dispute | You may be able to handle it directly with the insurer |

| Small claim with repair costs close to the deductible | The fee may outweigh the benefit |

| Straightforward personal property issue with complete receipts and no disagreement | Self-management can be reasonable |

The key is complexity, not emotion. A claim can feel overwhelming and still be straightforward. Another claim can look modest at first and become complicated once hidden damage appears.

If the insurer’s estimate doesn’t reflect what contractors are saying, or the adjuster’s inspection felt rushed, that’s usually the point to get help.

For homeowners weighing that decision, this article on when to hire a public adjuster lays out the timing issues well.

The practical cutoff

If you’re asking whether the insurer missed something important, they probably did not explain the estimate clearly enough. If you’re asking whether the payment feels low, compare scope before comparing dollars. Missing line items matter more than the bottom-line number.

That’s where a public adjuster earns their fee. Not by “arguing harder,” but by proving more.

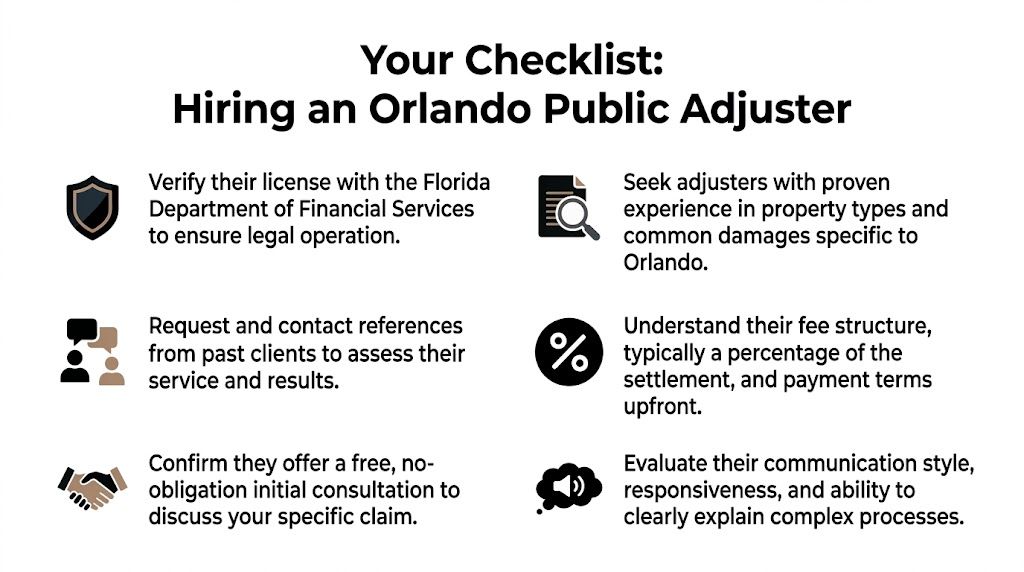

Finding and Vetting the Right Orlando Adjuster

After a storm or major water loss in Orlando, homeowners often get approached fast. A contractor has a recommendation. A door knocker says they can “handle everything.” Someone with a clean website promises a big recovery before they have seen the attic, the roof, or the policy. That is when bad hiring decisions happen.

Florida has a large pool of licensed adjusters, which gives you choices and also raises the odds of picking the wrong one if you do not screen carefully. The Florida Department of Financial Services license search is the first place to check whether the person is properly licensed and whether that license is active.

A polished pitch does not tell you much. The right adjuster for an Orlando claim needs to inspect thoroughly, document hidden damage, write an estimate that can stand up to carrier review, and keep pressing when the insurer limits scope or delays a supplement.

Start with license, local experience, and actual file handling

Verify the license first. Then get more specific.

Ask what kinds of claims they handle in Central Florida every month. Orlando files often involve wind-driven rain, tile roof damage, older underlayment issues, AC-related water damage, and moisture that spreads behind baseboards and cabinets long after the first inspection. Condo claims add another layer because unit-owner coverage, association responsibilities, and water origin disputes can overlap.

Also ask who will work the claim after you sign. Some firms sell the job through a senior person, then hand the file to someone with less experience. That handoff is not always a problem, but you should know it before you commit.

A good screening question is simple: “Who is inspecting my property, who is writing the estimate, and who is speaking to the carrier?” If the answer is vague, expect confusion later.

Homeowners who are still sorting out roles should review the difference between a public adjuster and an insurance adjuster before comparing firms.

Questions that tell you how they actually work

Fee questions matter, but they should not be the first or only filter. Ask questions that show whether the adjuster can build a claim properly under Florida conditions.

What types of Orlando-area losses do you handle most often?

Listen for specific answers. Roof and interior storm claims, slab leak water losses, fire losses, commercial losses, and condo unit claims all require different documentation.What happens during your first inspection?

Strong answers mention room-by-room photos, exterior review, moisture readings when appropriate, measurement methods, and a policy review tied to the damage observed.How do you handle hidden or progressive damage?

In Florida, many disputes turn on what was not visible during the first carrier inspection. The adjuster should be able to explain how they document that issue and submit supplements.How often will I hear from you, and from whom?

You want a clear update schedule and a clear contact person.What do you do when the carrier under-scopes the loss?

The best answers mention side-by-side estimate comparison, code-related issues where supported, contractor input when needed, and written support for omitted line items.Have you worked claims that required Florida pre-suit steps?

Not every file gets there, but Orlando policyholders benefit from hiring someone who understands the pressure points in Florida disputes and can prepare the file cleanly from the start.

Red flags that deserve caution

Some warning signs are obvious. Others are easy to miss until the claim stalls.

- They quote a claim value before a real inspection. Serious adjusters do not price a roof, water loss, or fire claim from a few phone pictures.

- They push for a same-day signature. You need time to verify the license, read reviews carefully, and compare two or three firms.

- They focus on lawsuits before claim preparation. Strong claim files usually get built through inspection, documentation, and scope support first.

- They cannot explain coverage or scope in plain English. If they confuse you during the interview, communication usually gets worse once the carrier pushes back.

- They avoid Orlando-specific questions. Local experience matters because weather patterns, roof types, and common insurer responses in Florida shape how a file should be documented.

A practical shortlist method

Keep the shortlist small. Two or three firms is enough.

Then compare them side by side.

| What to compare | What you want to hear |

|---|---|

| Inspection process | Clear steps, full documentation, no rushed promises |

| Orlando claim experience | Specific local loss types and examples, not generic “we do it all” language |

| File ownership | Names, roles, and who communicates with the insurer |

| Dispute approach | Methodical support for supplements and omitted damage |

| Communication | Defined update cadence and responsive contact methods |

The best hire is usually the adjuster who stays precise under pressure. In Orlando, that matters because insurers often move fast after storm events, and Florida claim deadlines, documentation demands, and pre-suit requirements leave little room for sloppy file work.

Understanding the Contract and Preparing to Work Together

The contract is where good claim help becomes a working relationship, or a future argument.

After a storm or major water loss in Orlando, homeowners are often signing documents while dealing with tarps, hotel stays, or a ceiling that still smells damp. That is exactly when sloppy terms get missed. Read the agreement slowly. Ask questions line by line. A reputable public adjuster will not rush that conversation, especially in Florida, where fee rules and claim handling deadlines can affect what happens after a hurricane or other declared emergency.

What the fee structure means in real life

Public adjusters usually work on contingency. They get paid from the insurance recovery, not by billing hours while the claim develops.

In Florida, fee limits can change based on the type of claim and whether the loss happened during a declared emergency period. The Florida Department of Financial Services lays out those rules in its public adjuster guidance, including the reduced cap that applies to certain hurricane and disaster-related claims during the first year after the event. That matters in Orlando because homeowners often hire help after wind and water losses tied to tropical systems, and the fee language in the contract should match the law.

Before you sign, pin down four points:

- How the percentage is applied: on the whole payment, only on new money recovered, or on supplements too

- What work is included: inspection, estimate writing, contents support, carrier meetings, and supplemental claim handling

- What happens if you cancel: any rescission period, termination terms, and whether the adjuster claims a fee on later payments

- Who will handle the file: the person you met, a staff adjuster, or a rotating office contact

If you want a plain-English explanation before reviewing percentages, this guide on public adjuster cost gives a helpful breakdown.

One practical note from the field. Ask how the contract treats payments already issued or payments the carrier sends directly to you after representation begins. That is where fee disputes often start.

What to gather before the file gets built

A strong claim file starts with records, not opinions. Your adjuster can only argue what can be documented.

Bring the full policy if you have it, including endorsements. In Florida claims, endorsement language often decides the core dispute, especially on roof surfaces, interior water damage, ordinance and law coverage, and deductibles tied to wind or hurricane losses. The declarations page alone is not enough.

You should also gather:

- Photos and video from the first day

- Receipts for emergency mitigation and temporary housing

- Any contractor proposals, drying logs, or inspection notes

- A room-by-room list of damaged items and affected areas

- Prior repair records if the insurer may argue the damage was pre-existing

Keep damaged materials and personal property when it is safe to do so. Do not throw out the soaked baseboards, warped flooring, or ruined contents until your adjuster confirms they have been documented well enough. Insurers often question scope after cleanup starts.

For homeowners who want a better sense of how carriers approach these conversations, How To Deal With Insurance Adjusters is useful background reading.

Set the working rules early

The first week should answer basic operational questions.

Who attends the carrier inspection? How fast do you send new invoices or repair findings to your adjuster? Will updates come by phone, email, or text? If the insurer asks for a recorded statement, proof of loss, or another round of documents, who prepares the response and who reviews it before it goes out?

In Orlando claims, speed matters, but accuracy matters more. A rushed answer can create a coverage problem that follows the file for months. Good adjusters keep the process organized, preserve the paper trail, and tell you when to pause before sending something to the carrier.

Your job is simpler, but it still matters. Preserve evidence, keep receipts, answer factual questions truthfully, and do not authorize permanent repairs before the damage is fully documented unless safety requires immediate work. That trade-off comes up all the time after roof leaks and storm losses. The house may need fast action, but the claim still needs proof.

Common Insurer Tactics and How Your Adjuster Fights Back

A lot of Orlando homeowners reach the same point. The field adjuster was polite, the first check arrived, and it still does not cover the roof, drywall, flooring, and moisture work the house requires.

That gap usually starts with claim handling, not just pricing. A narrow inspection, a missing room, or a document request sent in rounds can cut a claim down before the repair conversation even begins. A public adjuster Orlando homeowners hire steps in to control scope, timing, and proof.

Tactic one, delay and fatigue

Some carriers do not deny early. They slow the file down. Another document request comes in after you already sent photos. Then a second inspection gets discussed but not scheduled. Meanwhile, your kitchen is still torn up and the mitigation invoice is due.

A good adjuster closes that opening by setting a written timeline, answering requests in organized batches, and forcing the file to show what was sent and when. That matters in Florida, where claim disputes often turn on the paper trail as much as the damage itself.

If you want a plain-language overview of carrier behavior, read How To Deal With Insurance Adjusters and this breakdown of insurance company adjuster tricks homeowners run into during claims.

Tactic two, under-scoping visible and hidden damage

This is common after wind and water losses in Orlando. The carrier estimate may include the stained ceiling but leave out wet insulation, detached underlayment, swollen cabinetry, or flooring that cannot be patched to a reasonable match.

Your adjuster pushes back with better proof, not bigger opinions.

- Field documentation: Moisture readings, attic and roof observations, room-by-room photos, and notes tied to exact locations

- Line-item estimate review: Missing labor, detached and reset items, code-related steps, and finish work that often disappears from carrier estimates

- Policy matching: Damage tied to the actual coverage wording, endorsements, exclusions, and duties after loss

That last point matters more in Florida than many owners realize. A claim can be underpaid because the scope is weak, but it can also be underpaid because the damage was documented without connecting it clearly to the policy.

Tactic three, using technical process to gain an advantage

Insurers know many policyholders will not keep pressing once the process gets technical. That is one reason pre-suit work matters. In Florida, the dispute often turns before a lawsuit is ever filed.

According to Florida pre-suit notice claim data, adjuster-prepared estimates on Citizens Property Insurance claims average $98K, leading to demands of $161K. That gap shows what happens when the file is built fully before litigation.

For Orlando claims, this is not abstract procedure. It affects strategy. Florida has rules on pre-suit notice, and hurricane and other declared emergency claims can involve fee restrictions that change how a public adjuster structures the file and the timing of escalation. Generic national advice usually misses that.

Why pre-suit preparation matters in Orlando

Pre-suit notice works only if the claim file is ready. If the estimate is thin, the notice is thin. If the file includes measurements, photos, cause analysis, prior submissions, and a clean line-item comparison, the carrier has a harder time ignoring the dispute.

| Insurer move | Effective counter |

|---|---|

| “We need more time” | Written follow-up with a dated chronology and copies of prior submissions |

| “That damage isn’t related” | Cause and scope support tied to inspection findings and repair logic |

| “Our estimate already covers it” | Side-by-side estimate comparison showing omitted or underpriced work |

A strong claim file gives the insurer fewer places to hide.

The best adjusters in Orlando do not escalate for show. They escalate when the record is organized, supported, and ready to survive scrutiny.

Frequently Asked Questions About Orlando Public Adjusters

What kind of settlement increase is realistic in Orlando

There is no honest fixed percentage.

In Orlando, the result usually turns on four things. How complete the first inspection was, whether the carrier missed hidden moisture or code-related work, how the policy handles replacement cost and exclusions, and how well the claim file is documented before the dispute hardens. Older homes in particular tend to produce larger gaps between the carrier’s first number and the true repair cost, but that is a file-specific issue, not a number any ethical adjuster should promise in advance.

A better question is this: did the insurer price the full scope, or only the damage that was easy to see on day one? In my experience, many underpaid claims start with omitted rooms, missed detach and reset work, incomplete drying, or roofing line items that do not match local repair reality in Central Florida.

How long does a claim take with a public adjuster

Simple losses can move in weeks. Disputed water, roof, and hurricane claims often take much longer.

Orlando files slow down when causation is contested, the carrier asks for repeated documents, or the damage was not fully documented before cleanup. Florida procedure matters here too. If the claim is heading toward a pre-suit dispute, your adjuster has to build the record carefully, because a rushed file usually weakens your position instead of speeding payment.

Speed matters. So does getting the scope right the first time.

Can I switch or cancel if the relationship goes bad

Sometimes, yes. The answer depends on the contract.

Read the cancellation and termination language before signing. Look for how fees are handled if the adjuster has already inspected, prepared estimates, or started negotiations. In Florida, this is not a minor detail. If the claim involves a hurricane or other declared emergency, fee rules can already limit how the agreement is structured, so you want clear terms in writing before work begins.

If a firm gets vague when you ask about cancellation, treat that as a warning.

Is the fee negotiable

Sometimes. Sometimes the answer is no.

Fee flexibility usually depends on loss size, claim stage, and how much reconstruction work the file needs. A fresh claim with clean documentation is different from a disputed Orlando roof or water loss where the adjuster has to rebuild scope, pricing, and chronology from scratch.

Focus on clarity more than headline percentage. Ask what the fee applies to, whether it changes if supplemental payments come in later, and how Florida emergency-claim fee restrictions affect the contract.

Should I hire a public adjuster before or after the insurance inspection

For a substantial loss, earlier is usually better.

Early involvement helps document the condition before temporary repairs, demolition, or drying change the evidence. It also helps prevent avoidable problems with inventories, recorded statements, and incomplete scope. If the carrier has already inspected, you can still bring in a public adjuster. It just means more effort may go toward correcting a weak first record instead of building a strong one from the start.

What should I do today if my property was just damaged

Start with the first 24 hours.

- Protect the property from further damage: Tarp roof openings, board broken windows, shut off water or power if needed, and keep receipts for every emergency expense.

- Document before conditions change: Take wide photos, close-ups, video walkthroughs, and note the date and time.

- Separate cleanup from disposal: If materials must come out, photograph them first and keep samples when practical.

- Report the loss promptly: Give the carrier basic facts, but do not guess about cause, scope, or cost.

- Ask for a full certified policy copy: The declarations page is not enough to evaluate coverage, limits, duties after loss, or endorsements.

Then make a judgment call. If the damage is minor and straightforward, you may be able to handle it yourself. If it involves roofing, water spread, mold, business interruption, code upgrades, or a large gap between the visible damage and the first insurer estimate, get professional help early.

If you’re in Oregon or Washington and need experienced help after fire, storm, flood, vandalism, or a complex commercial loss, NW Claims Management provides licensed public adjusting representation focused on policyholders, not insurers. The team handles claim documentation, policy analysis, negotiation, and settlement strategy on a contingency basis, so you can move from confusion to a structured recovery plan with clear guidance.