When it comes to your property, thinking about insurance risk can't be a passive activity anymore. It's not enough to just buy a policy and file it away. To truly protect your investment, you have to get in the driver's seat. That means actively looking for threats specific to your property, taking real steps to reduce those risks, and knowing your policy inside and out before you ever need it. Having a solid action plan is your best defense against a financial disaster.

The New Reality of Property Risk in the Pacific Northwest

Let's be honest: owning property in Oregon and Washington has changed. The days of predictable stability are behind us. We're now facing more frequent and powerful natural disasters, from devastating wildfires that sweep through entire towns to atmospheric rivers that cause unprecedented flooding. These aren't just news stories; they are the new reality impacting your bottom line.

Because of this, just having an insurance policy isn't the ironclad guarantee it once was. Insurance carriers are feeling the pressure, too. They're responding by hiking premiums, making it harder to qualify for coverage, and in some areas, simply refusing to renew policies. The rules of the game have changed, and if you don't adapt, you’re leaving yourself dangerously exposed.

The Soaring Cost of Complacency

The financial fallout from this new normal is staggering. In just the first half of 2025, climate-related disasters caused $162 billion in global economic losses. The insured portion of that hit $100 billion—that's a 40% jump from the $71 billion we saw in the same period of 2024.

And where did most of that happen? Right here. The United States accounted for over 90% of those insured losses. For anyone owning property in Oregon and Washington, those numbers should be a wake-up call.

This guide is your action plan. It's designed to help you move past the anxiety and into a state of preparedness, with concrete steps to protect what's yours. We're focused on what you can control now to prevent a catastrophe later.

A passive approach to property insurance today is a direct path to financial exposure. Your policy is a starting point, not the entire strategy. Taking control of your risk profile is the single most important action you can take to protect your investment.

Shifting from Reactive to Proactive

So, what does managing insurance risk actually look like? It means building a strong defense long before you ever have to think about filing a claim. It breaks down into a few key areas:

- Pinpointing Your Threats: Get specific. Are you dealing with wildfire exposure in Bend or flood potential in the Puyallup River Valley? Know your enemy.

- Taking Action: This is about making physical improvements. It could mean creating defensible space around your home, upgrading old plumbing, or retrofitting for earthquakes.

- Mastering Your Policy: Your insurance needs aren't static. Review your policy every single year to make sure your coverage keeps up with today's rebuilding costs and ever-changing local building codes.

Think about it this way: a serious house fire is more than just a personal tragedy; it's the start of an incredibly complex and often frustrating financial puzzle. Knowing what to do after a house fire with your insurance ahead of time can be the difference between a smooth recovery and a nightmare.

By following the strategies we're about to lay out, you’ll be far better prepared to handle whatever comes your way and fight for the settlement you deserve.

Conducting Your Property Risk Assessment

If you want to get a handle on insurance risk, you first have to know what you're up against. That's where a thorough property risk assessment comes in. It’s the essential first step—basically, walking your property with a critical eye to spot vulnerabilities before they become expensive claims.

Think of it as preventative medicine for your biggest investment.

This process goes beyond just looking for obvious problems. It’s about seeing how small, overlooked details can snowball into major disasters. For instance, that slow drip under a bathroom sink might seem insignificant. But over months, it can lead to rotted subfloors, widespread mold, and a complicated water damage claim that your insurer could argue was just a preventable maintenance issue.

The goal is to stop reacting to problems and start getting ahead of them. Let's get specific about what you should be looking for.

Checklist for Residential Properties

For homeowners, risks are often tied to the age of the house and its immediate environment. A great starting point is understanding what a home inspection entails, as that gives you a professional baseline. From there, you can conduct your own regular check-ups by focusing on these key areas:

- Water Intrusion Points: Scrutinize your roof for any missing or damaged shingles. Make sure your gutters are clear and actually channeling water away from the foundation. Don't forget to inspect the seals around every window and door for gaps.

- Aging Systems: Know the age of your water heater, HVAC unit, and major appliances. A water heater that's past its 10-year lifespan isn't just old—it's a ticking time bomb for a potential flood.

- Electrical Hazards: Keep an eye out for outdated wiring (like knob-and-tube), overloaded outlets, or lights that flicker. These are classic signs of a serious fire risk.

- Wildfire Defensible Space: This is non-negotiable for homes in Oregon and Washington's wildland-urban interface. You must clear a perimeter of at least 30 feet around your home of flammable vegetation, pine needles, and dead leaves.

I once handled a claim where a homeowner lost everything because embers from a nearby wildfire ignited a pile of dry firewood stacked right up against their house. It was a simple, tragic oversight. That's a perfect, real-world example of how a small risk assessment action could have saved an entire home.

Checklist for Commercial Properties

If you own or manage a commercial property, the scope of risk gets much bigger. You're not just protecting a building; you're responsible for the safety of employees, customers, and the general public. In these situations, a detailed property damage assessment becomes even more crucial.

Your assessment needs to cover a few more bases:

- Public Liability Hazards: Walk the areas where the public has access. Are there cracked sidewalks that create trip hazards? Is the lighting in your parking lot adequate and functional? Are all the handrails secure?

- Fire Suppression Systems: Don't just assume they work. Regularly test and certify your sprinkler systems, fire alarms, and extinguishers. Make sure all the documentation is up-to-date and easy to find.

- HVAC and Mechanical Systems: A failed HVAC system is more than just an inconvenience. It can lead to business interruption, mold growth from condensation, and even burst pipes in the winter. Meticulous maintenance logs are your best friend here.

- Security and Vandalism: Take a hard look at your property's vulnerability to theft and vandalism. Are your fences secure? Is all the exterior lighting working? Do you have monitored security cameras in place?

Turning Your Assessment Into Action

Finishing these checklists is just the beginning. The real work—and the real value—comes from turning your findings into a prioritized action plan. Not every risk is created equal, so you’ll need to categorize them by severity and the cost to fix. A loose handrail is a quick, cheap fix that can prevent a massive liability claim. A 20-year-old roof, on the other hand, is a major capital expense that requires serious planning.

Taking these proactive steps shows your insurer that you're a responsible property owner, which matters more than ever in the current market. Even with fierce competition recently driving global property insurance rates down by 9% in a single quarter, insurers are still rewarding well-managed properties with better terms and pricing. At the same time, they're heavily scrutinizing properties that carry a higher-risk profile.

A documented risk assessment and a clear mitigation plan are your best tools. They not only help you prevent losses but also position you to get the best possible coverage and pricing from your insurance carrier.

Decoding Your Insurance Policy Like a Pro

Your insurance policy isn't just a document you sign and file away. It’s a complex, legally binding contract, and simply assuming you're covered can be a financially catastrophic mistake when disaster strikes. To truly manage your risk, you have to treat your policy as a living agreement that you fully understand and regularly revisit.

Let's be honest, the language can be dense and confusing. But this isn't about memorizing legal jargon. It's about knowing which parts of the policy hold the most financial weight. A single clause tucked away on page 17 could mean the difference between a full recovery and a crippling out-of-pocket expense.

The Clauses You Absolutely Cannot Ignore

When you open your policy, the declarations page gives you the highlights, but the real devil is in the details—specifically, the definitions, exclusions, and conditions sections. Two of the most critical terms you need to find are Replacement Cost Value (RCV) and Actual Cash Value (ACV).

- Replacement Cost Value (RCV): This is the gold standard. RCV pays to replace your damaged property with brand-new materials of similar kind and quality, without any deduction for depreciation. It’s designed to make you whole at today's prices.

- Actual Cash Value (ACV): This is RCV minus depreciation. If a hailstorm destroys your 15-year-old roof, an ACV policy only pays you for the remaining value of a 15-year-old roof. You're left to foot the bill for the substantial difference to install a brand new one.

That one distinction can easily amount to tens or even hundreds of thousands of dollars on a major claim. If your policy is ACV, your first call should be to your agent to discuss upgrading to RCV.

I’ve seen countless homeowners crushed when they discover their "full coverage" policy was actually ACV. They thought they were insured for a new house, but the settlement they received was barely enough to pay off their mortgage, let alone rebuild. Understanding this one detail is paramount.

Another landmine to watch for is the co-insurance penalty. This clause requires you to insure your property for a specific percentage of its total value, usually 80-90%. If you’re underinsured when a loss occurs, your insurance company can penalize you by reducing your claim payment proportionally.

For example, say your property is valued at $500,000 and your policy has an 80% co-insurance clause. You’re required to have at least $400,000 in coverage. If you only carry $300,000 (just 75% of the required amount), your insurer may only pay 75% of your claim, even if the total damage is well below your $300,000 limit. It’s a nasty "gotcha" that catches far too many property owners off guard.

Your Annual Policy Review Checklist

To stay ahead of the game, you need to review your policy at least once a year—and not just when the renewal notice shows up. Set a dedicated meeting with your agent and come prepared with a clear agenda.

Here’s what you should cover:

- Are your coverage limits high enough? Construction costs have skyrocketed. The amount that would have rebuilt your home two years ago might be dangerously inadequate today. Our guide to understanding insurance policy limits offers a deeper dive into this.

- How is your property valued? Confirm in writing that you have RCV coverage. If you have ACV, get a quote for what it would cost to upgrade. The peace of mind is almost always worth the extra premium.

- What's explicitly not covered? Don't be shy. Ask your agent point-blank: "What are the biggest gaps in my coverage?" Standard policies often exclude major risks like floods, earthquakes, and certain types of water damage (like sewer backup).

- Do you have Ordinance or Law coverage? If your property is damaged, local building codes may have changed since it was constructed. This add-on coverage pays the extra cost to bring your property up to current code during repairs—an expense a standard policy won't touch.

By actively reviewing these items, you shift from being a passive policyholder to a proactive risk manager. You stop hoping for the best and start ensuring your most valuable asset has the protection it actually needs.

Building Your Claim-Ready Toolkit

The absolute best time to prepare for an insurance claim is right now, long before you ever need one. When disaster hits, the last thing you'll be able to do is calmly recall every item in your home and prove what it was worth. A well-organized toolkit is your secret weapon against the chaos.

This is more than just a simple list. It’s about building an undeniable record of your property and everything in it. From my experience, this level of preparation is the single most effective way to speed up the claims process, push back against lowball offers, and make sure you get paid fairly for your loss.

Create a Bulletproof Property Inventory

A handwritten list of your belongings is a start, but it won't hold much water with an insurance company. To truly maximize your settlement, you need a powerful visual and digital record that leaves zero room for doubt.

Grab your smartphone and start documenting your home, one room at a time. Take a slow, panoramic video of each space. Don't forget to open every closet, cabinet, and drawer. As you record, narrate what you're seeing. Mention anything special—"This is my grandfather's watch," or "We bought this sofa from Crate & Barrel in 2023."

After the video tour, switch to taking detailed photos of your high-value items. This is where you get specific:

- Electronics: Snap a clear picture of the serial and model numbers.

- Appliances: Get a photo of the manufacturer's label.

- Furniture: Take shots from different angles, making sure to capture any brand markings.

- Art & Collectibles: Zoom in on signatures, edition numbers, or other unique features.

This visual proof is a game-changer when you're negotiating with an adjuster. It shifts the conversation from "I think I had a nice TV" to "Here is the photo, model number, and receipt for my 65-inch OLED TV."

In all my years of handling claims, I've seen firsthand that those backed by video and photos settle faster and for significantly more money. An adjuster simply can’t argue with a clear video of your living room or a photo of a serial number. This documentation becomes your most powerful negotiation tool.

Digitize and Safeguard Your Proof

What good is your inventory if it gets destroyed in the same fire or flood that damages your home? Keeping paper receipts in a filing cabinet or photos on a single home computer is a huge risk. You need a secure, off-site way to store everything.

Cloud storage is the answer. Services like Google Drive or Dropbox let you upload your videos, photos, and scanned documents so you can access them from anywhere.

Create a main folder called "Property Insurance" and organize it with sub-folders like these:

- Photos & Videos: Label them by room (e.g., "Kitchen," "Master Bedroom").

- Receipts & Appraisals: Scan and upload all receipts for major purchases. If you have appraisals for jewelry, art, or antiques, get those in there, too.

- Policy Documents: Save a complete digital copy of your insurance policy, especially the declarations page.

- Key Contacts: A simple document with phone numbers for your insurance agent, a trusted local contractor, and a public adjuster.

This level of organization is more important than ever. The IAIS Global Insurance Market Report 2025 points out that as insurers face new threats, they're beefing up their own systems to scrutinize payouts. Your meticulous records are your best defense against this heightened scrutiny.

Get Your Emergency Plan in Place

Finally, put your digital toolkit into a practical emergency plan. If you have to evacuate in a hurry, you won't have time to hunt for documents.

First, know exactly where your main utility shut-offs are—water, gas, and electricity. Practice turning them off so you can do it quickly under pressure. In a fire or flood, this simple act can prevent thousands of dollars in secondary damage.

Next, make sure your digital toolkit is easily accessible from your phone. With everything organized in the cloud, your smartphone essentially becomes your emergency "go-bag." It holds your proof of ownership, your policy details, and the contacts you need to start the recovery process immediately. This preparation puts you back in the driver's seat when you feel like you have no control.

Navigating a Claim and When to Call for Backup

The moment disaster strikes your property, the clock starts ticking. In those first chaotic hours, your job is to focus on two things: making sure everyone is safe and taking immediate, reasonable steps to stop the damage from getting worse. Once that's handled, you notify your insurance company. This is your first step in managing the risk that follows the event itself.

After you make that initial call, the claims process officially kicks off. You'll quickly meet the main players, starting with the adjuster assigned by your insurance company. It's critical to remember who they work for. While they are usually professional and pleasant, their primary duty is to protect the financial interests of their employer, the insurance company.

You don't have to navigate this process alone. You have the right to bring in your own expert: a public adjuster.

Understanding the Role of a Public Adjuster

A public adjuster is a state-licensed claims professional who works exclusively for you, the policyholder. We don't work for insurance companies. Our only job is to manage your claim from start to finish—documenting your losses, digging into your complex policy language, and negotiating with the insurer to get you the full and fair settlement you're entitled to.

Think of it this way: if you were sued, you wouldn’t rely on the other party’s lawyer for advice. A major insurance claim is a high-stakes financial negotiation. Going in alone means you're up against a team of experts who handle these situations every single day. A public adjuster levels that playing field.

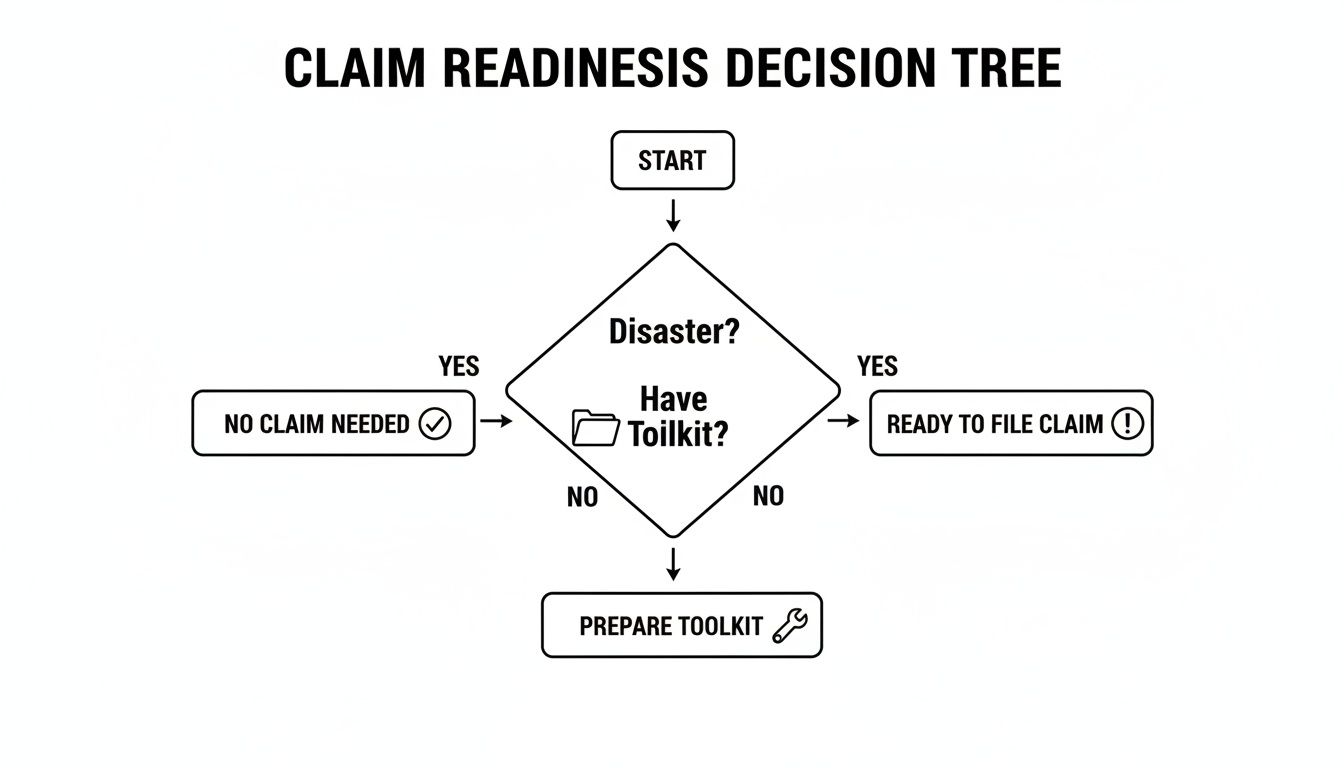

The flowchart below gives you a clear path for assessing your readiness before a claim even happens.

As you can see, a disaster is just the beginning. Having a pre-built toolkit is what separates a smooth, efficient recovery from a long, stressful ordeal.

When Is It Time to Call for Backup?

Not every claim needs a public adjuster. A small, straightforward claim for a broken window is probably something you can handle on your own. But in other situations, bringing in an advocate isn't just a good idea—it can be the difference between a successful recovery and a financial disaster.

You should seriously consider getting professional help in these scenarios:

- You've suffered a major or catastrophic loss. After a significant fire, flood, or storm, the scope of damage is just enormous. It involves complex structural assessments, detailed contents inventories, and business interruption calculations that are simply overwhelming for most property owners.

- The claim is complicated. Water damage claims with hidden mold, smoke damage that has seeped into an entire building, or claims involving multiple structures are notoriously difficult. An insurer's adjuster might undervalue—or completely miss—these "hidden" damages.

- You’ve received a lowball settlement offer. If the first offer from your insurer is shockingly low and won't even come close to covering your real repair costs, that’s a huge red flag. You need a professional negotiator to build a detailed counter-proof of loss and fight back.

- The insurer is delaying or denying your claim. When weeks turn into months with no progress, or you get a denial letter filled with confusing policy jargon, it's time to bring in an expert who can challenge their position and force a resolution.

- You just don't have the time or expertise. Managing a large insurance claim is a full-time job. If you're trying to run your business or get your family’s life back to normal, you simply won't have the hundreds of hours it takes to properly document and negotiate your claim.

I worked with a restaurant owner in Portland whose business suffered a major kitchen fire. The insurer's initial offer barely covered the new equipment, completely ignoring the extensive smoke and soot damage to the dining room and the massive business income loss. We reopened the claim, brought in our own experts to document the full extent of the damage, and ultimately recovered a settlement that was nearly three times the original offer. That's the power of having an advocate.

Hiring help is a strategic decision to protect your financial recovery. For anyone navigating the choppy waters of a property claim, learning more about when to hire a public adjuster can provide much-needed clarity and confidence. It’s all about making sure you have the right team fighting for your best interests when the stakes are highest.

Common Questions About Managing Insurance Risk

As a public adjuster working across Oregon and Washington, I talk to property owners every day who are understandably feeling overwhelmed. Managing insurance risk feels complicated, but it doesn't have to be. Let's break down some of the most common questions I hear to give you the clarity you need to protect your investment.

My Insurance Premium Went Up but My Coverage Didn’t. Why and What Can I Do?

It’s a frustrating—and incredibly common—experience. You open your renewal notice, and the price has jumped, even though you haven't had a claim. What gives?

Often, these increases have little to do with you personally. Insurers are adjusting their rates across the board to keep up with the soaring costs of lumber, materials, and labor. They're also reacting to the increased frequency of major disasters in our region, like wildfires and severe storms. Essentially, their risk is going up, and they're passing that cost along to policyholders.

But you’re not powerless. Here’s what you can do to push back:

- Showcase Your Upgrades: Have you recently installed a new roof, upgraded old plumbing, or put in a monitored alarm system? Don't assume your agent knows. Call them immediately. Proactive improvements like these can make you eligible for some pretty significant discounts.

- Shop Your Policy: Loyalty doesn't always translate to the best price in insurance. Get quotes from at least a couple of other reputable carriers before you renew. Another company might view your property's risk profile differently and offer a much better rate.

- Revisit Your Deductible: If you have a solid emergency fund, think about raising your deductible. By agreeing to cover a larger amount out-of-pocket for a potential claim, you can lower your annual premium. Just be absolutely sure you can comfortably afford that higher deductible if something happens.

What Is the Difference Between an Insurance Agent and a Public Adjuster?

Understanding this difference is one of the most critical things a property owner can learn. Getting it wrong can cost you thousands after a loss.

Your Insurance Agent is the person who sells you the policy. They might be a "captive" agent working for one specific company or an independent agent who represents several. Their primary role is sales.

The Insurance Company Adjuster (also called a staff or independent adjuster) is assigned by your insurer after you've had a loss. Their legal and professional duty is to their employer—the insurance company. Their job is to evaluate the damage and resolve the claim based on the insurer's guidelines and financial interests.

A Public Adjuster is the only adjuster licensed by the state to work exclusively for you, the policyholder. We step in after a loss to manage every single detail of your claim, from documenting the damage to negotiating the final settlement. Our only goal is to make sure you receive the maximum amount you're entitled to under your policy.

Think of it this way: The insurance company's adjuster is their expert, representing their interests. A public adjuster is your expert, representing only yours. In a high-stakes financial negotiation, you want your own advocate in your corner.

Can I Really Negotiate My Claim Settlement with the Insurance Company?

Absolutely. The first settlement offer you get from an insurance company is just that—an offer. It's a starting point for a negotiation, not the final word. You have every right to challenge it if you believe it's too low.

But to negotiate effectively, you need more than just a feeling. You need to build a rock-solid case with your own evidence. This means you have to prove it with documentation like:

- Detailed, line-item repair estimates from your own trusted, independent contractors.

- A comprehensive inventory of every single damaged item, complete with photos, receipts, and research on what it costs to replace them today.

- Reports from third-party experts, like an industrial hygienist to test for smoke or mold, to document the true scope of the damage.

Let's be honest: this is a mountain of work, and insurers know it. They are professionals who handle thousands of claims. Over the years, we've seen countless insurance adjuster tricks they use to justify paying less. This gap in experience is precisely why so many property owners bring in a public adjuster to level the playing field and manage the negotiation for them.

Does Making My Property Safer Actually Lower My Insurance Costs?

Yes, it really does. This is one of the best ways you can take control of your insurance costs. Insurers are in the business of calculating risk, and they will reward you for making your property a safer bet.

For example, simply installing a monitored fire and burglar alarm system can earn you a discount of up to 15-20% on your homeowner's policy. In the wildfire-prone areas of Oregon and Washington, creating "defensible space" by clearing brush and flammable vegetation from around your home doesn't just make it safer—it can also make it more insurable and qualify you for better rates.

Whenever you make a significant safety upgrade, tell your insurance agent in writing. Ask them to review your policy and apply all available discounts. It’s a true win-win: your property is better protected, and you pay less for that peace of mind.

Feeling overwhelmed by a property damage claim? You don't have to go through it alone. The team at NW Claims Management is here to fight for you. We handle every step of the process to ensure you get the full settlement you deserve. Get a free claim evaluation today at https://nwclaimsmanagement.com.